Water Activity Instrumentation Market Outlook

Other |

2026-06-10 13:38:19

PW Consulting’s latest Pag Compressor Oil Market report (base year 2025, forecast period 2026–2032) delivers an operationally focused intelligence package to inform board- and executive-level decisions in 2026. The global market reached approximately USD 939 million in 2025 and is modeled to expand to roughly USD 1,037 million in 2026, proceeding to an estimated USD 1,459 million by 2032 — a compound annual growth rate (CAGR) of 6.51% over the forecast window. Market concentration is moderate: the top three players account for just over 42% of the market, while the top five represent about 58% — a structure that rewards scale but still leaves tactical openings for differentiated specialists.

Pag Compressor Oil Market

Actionable timing: Our 2026-focused scenario analysis translates multi-year forecasts into 12–18 month tactical choices — from CAPEX phasing to procurement locks and product launch sequencing.

Pag Compressor Oil Market

Margin-first playbook: With upstream feedstock volatility and raw-material inflation (notably recent production-cost upticks tied to CPI/PPI movements and elevated polypropylene glycol pricing), the report provides concrete levers to protect margin and working capital.

Pag Compressor Oil Market

M&A and partnership prioritization: The combination of medium concentration and technological differentiation creates specific M&A archetypes; the report maps targets by capability rather than headline geography.

Three structural forces will determine winners next year: product compatibility with low-GWP refrigerants, raw-material cost trajectories, and applied scale in industrial channels. Regulatory momentum (for example, EU F-Gas regulation and the Kigali Amendment) continues to accelerate adoption of low-global-warming-potential refrigerants. This shift is increasing demand for PAG lubricants that are chemically compatible with next-generation refrigerants.

At the same time, producers face input-cost pressure. Polyalkylene glycol production costs have risen following recent CPI and PPI movements, and polypropylene glycol benchmarks moved materially in late 2025, exerting near-term margin stress. Our bottom-up cost models show that, absent targeted pricing or efficiency actions, EBITDA volatility is likely for smaller producers during periods of raw-material inflation.

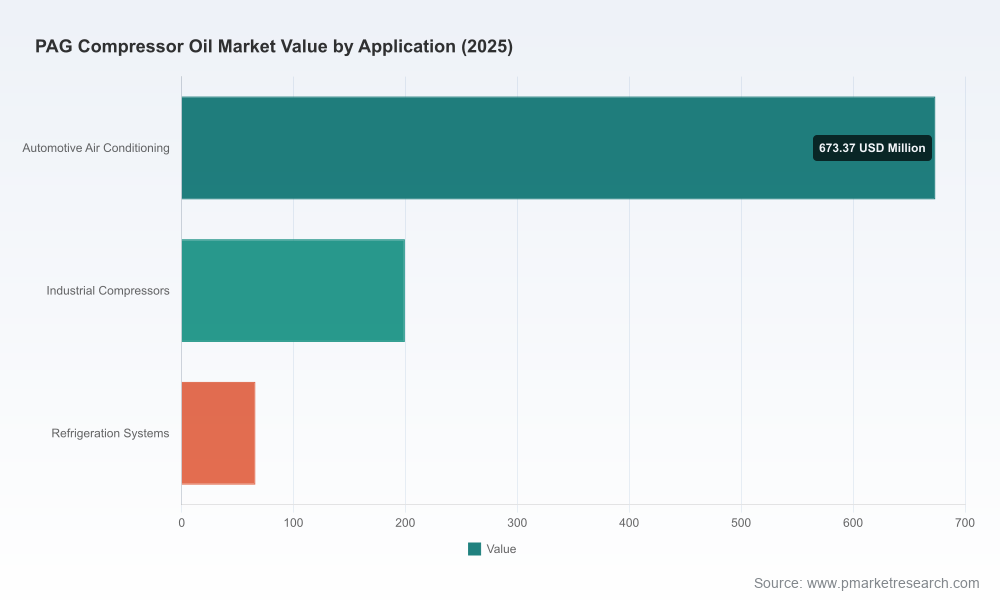

Demand-side, the market benefits from durable industrial compression growth plus a structural upgrade cycle in automotive HVAC and electrified vehicle architectures that require tailored dielectric and thermal properties. These demand threads combine to produce the reported CAGR of 6.51% through 2032.

The market is populated by supermajors, integrated chemical suppliers, specialized lubricant formulators and nimble regional players. Key competitive archetypes and implications:

Integrated majors (e.g., ExxonMobil, Shell, Chevron, TotalEnergies): These firms leverage OEM approvals, global distribution and integrated sourcing for scale advantages. Their strategies in 2026 will focus on locking OEM design wins and extending shelf-to-field supply agreements. Expect continued productization of PAG fluids with OEM certification as a go-to-market moat.

Chemical and feedstock integrators (e.g., BASF, Cargill): Backward integration into base stocks gives these firms superior supply security. For buyers, these suppliers provide a defensible hedge against feedstock shortages — a critical factor for long-term contracts.

Specialized formulators and high-performance niche players (e.g., Klüber, FUCHS, Next Lubricants, Matrix Lubricants): These vendors compete on formulation sophistication and field-specific performance guarantees. Their strategic advantage in 2026 will be rapid qualification cycles with OEMs and custom formulations for electric compressors and R1234yf applications.

Regional and aftermarket players (e.g., AMSOIL, Shrieve Chemical, Oscar Lubricants): These companies win on agility and targeted product launches. Recent launches have targeted EV and hybrid HVAC systems with low-viscosity PAG grades designed for extreme climate operation.

Recent corporate moves underscore both consolidation and product innovation: Chevron’s acquisition of Hess (July 2025) strengthens scale across energy and industrial lubricants; Oscar Lubricants launched new PAG grades for automotive R134a and R1234yf systems in August 2025; and Petronas in 2023 introduced high-durability PAG compressor oils with long service life guarantees. These developments indicate concurrent strategies of scale-building and premium product rollouts.

The report is intentionally execution-oriented. It includes:

Proprietary market sizing and topline forecasts (historical 2020–2025; forward 2026–2032) with scenario bands for high- and low-uptake pathways.

Supply-chain risk heatmap combining feedstock exposure, supplier concentration, transport vulnerability and inventory-days modelling to quantify potential disruptions by severity and duration.

Pricing and margin toolkits that translate feedstock swings into SKU-level margin outcomes and suggest contract clauses (indexation, collar mechanisms, cap-and-floor pricing) suitable to different counterparty types.

Commercial playbooks for OEM qualification, aftermarket channel penetration, and fleet-specification strategies — including templates for field trials and success metrics.

Acquisition and partnership frameworks that map value-creation levers (technology, distribution, backward integration) and typical valuation multiples by archetype.

Regulatory impact matrix and product-readiness scoring for common low-GWP refrigerants, enabling product roadmaps that balance speed-to-market with risk.

Procurement: Move from calendar-driven purchases to conditional contracts tied to feedstock indices; prioritize multi-sourcing from base-stock integrators to raise service levels during volatility.

R&D and product management: Accelerate validation pipelines for R1234yf- and electric-compressor-compatible PAGs; adopt modular formulation platforms to shorten OEM qualification time.

Commercial strategy: Differentiate either by scale (supply security, OEM approvals) or by specialization (application-specific fluids and value-added testing services); attempts to be “everything to everyone” will underperform.

M&A and partnerships: Target bolt-on acquisitions that deliver one or two of: access to certified OEM approvals, backward integration into PAG base-stocks, or presence in aftermarket/service channels.

Risk management: Implement hedging and pricing collars for feedstock exposure and adopt KPI-based supplier SLAs; design contingency inventories for critical regions or product families.

This press release is designed as a strategic preview. To preserve competitive integrity and to deliver the full operational value to subscribers, we have intentionally withheld detailed regional, application and SKU-level splits that underpin the forecast. The full report contains the granular segmentation, OEM qualification matrices, supplier scorecards and downloadable financial models that enable transaction-grade decision-making.

For C-suite leaders preparing 2026 budgets, the immediate priorities are clear: secure multi-year supply arrangements with price-flex clauses, accelerate compatibility testing for low-GWP refrigerants and prioritize either scale-driven or speciality-driven go-to-market strategies. PW Consulting’s report equips you with the scenario tools, playbooks and counterparty analyses necessary to convert the macro growth opportunity (6.51% CAGR to 2032) into defensible margin expansion and reduced operational volatility.

Organizations that require the full dataset, supplier scorecards, downloadable financial models and the tactical playbooks should contact PW Consulting or visit our Pag Compressor Oil Market report page. The full package is structured to support 12–18 month execution plans and includes bespoke briefing sessions for executive teams and investment committees.

For detailed analysis of this topic, please visit the official page:Pag Compressor Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com