Is Wireless Connectivity Becoming the Backbone of Next-Generation Healthcare Systems?

Networking |

2026-06-09 12:14:49

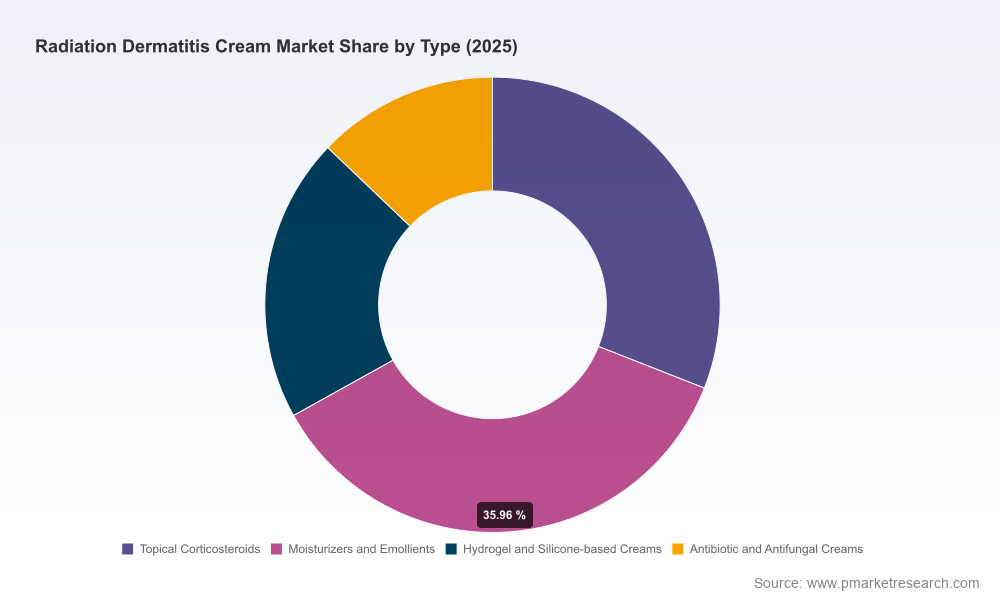

The market for radiation dermatitis creams has moved from a niche supportive-care segment into a strategic battleground for specialty dermatologic and oncology-focused manufacturers. Our latest market model shows the global market expanding from approximately USD 410 million in 2020 to about USD 520 million in 2025, and, under our central-case forecast, approaching roughly USD 745 million by 2032. This trajectory implies a mid-single-digit compound annual growth rate (CAGR) of about 5.25% over the 2026–2032 forecast window — sufficient to attract new entrants, to drive product innovation, and to justify near-term commercial investments by incumbent players.

Radiation Dermatitis Cream Market Research

Timing of clinical and commercial investment. With steady market expansion and moderate concentration (CR3 ≈ 34.8%, CR5 ≈ 51.25%), 2026 is a pivotal year for firms to decide whether to accelerate clinical programs, secure distribution footholds, or pursue opportunistic M&A before competitive differentiation becomes harder and acquisition prices rise.

Radiation Dermatitis Cream Market Research

Reimbursement and guideline alignment. Evolving clinical guidance and payer recognition of supportive oncology therapies create windows for formulary inclusion and enhanced reimbursement pathways — a material consideration for firms that can demonstrate cost-offsets and patient-centered outcomes.

Radiation Dermatitis Cream Market Research

Product mix and manufacturing prioritization. Advances in silicone-based occlusion, hydrogel hydration, and steroid-sparing anti-inflammatory approaches favor targeted R&D spend rather than broad product portfolios.

Three structural forces underpin the market’s steady growth. First, the growing global oncology patient population and expanding use of radiotherapy sustain absolute need for topical management of radiation-induced skin injury. Second, guideline evolution — for example, recent recommendations supporting moisturizers and barrier creams without steroids for mild-to-moderate dermatitis — is reshaping clinical preferences toward steroid-sparing and barrier-oriented formulations. Third, payer recognition in several major markets, including certain Medicare reimbursement pathways for prescription radiation dermatitis products, increases the commercial viability of prescription-strength offerings that are supported by health-economics evidence.

On formulation science, the migration toward silicone-based and hydrogel platforms is material: clinical and manufacturer-supplied data indicate silicone occlusion can reduce trans-epidermal moisture loss by a substantial margin, delivering both symptomatic relief and a platform for adjunctive actives. These performance differentials are becoming primary decision criteria for procurement by oncology centers, hospital pharmacies, and specialty distributors.

The competitive map is heterogeneous: a mix of smaller specialty firms with focused, clinically-differentiated products sits alongside larger pharmaceutical and medtech companies that leverage scale in distribution and payer contracting. Our research highlights four illustrative players whose strategies exemplify prevailing market archetypes:

PrimaMed Clinical Systems (Miaderm): A small-to-mid cap specialty player offering a steroid‑free antioxidant and emollient cream positioned around tolerability and daily-use protocols. Strengths include targeted formulation messaging and relationships with dermatology and radiation oncology clinics; limitations are scale of distribution and depth of payer dossiers.

Stratpharma AG (StrataXRT): A focused device/formulation provider that leverages silicone gel technology for occlusion and protection. Its scientific narrative around moisture preservation and dressing-based prevention resonates with clinicians seeking non‑pharmacologic options. Competitive advantages include a device-class positioning that can simplify regulatory pathways in some jurisdictions.

Integra LifeSciences (Xeladrone): A larger medtech/biomaterials player with a hydrogel-based offering emphasizing hydration and anti‑inflammatory support. Integra’s ability to cross-leverage hospital relationships and supply-chain capabilities gives it a distribution advantage in hospital pharmacy channels.

Viatris (Biafine Emulsion Cream): A legacy clinical brand with broad international recognition and an established commercial footprint. It exemplifies a portfolio-based manufacturer able to combine brand reach with supply reliability, though such players must continually refresh evidence and labeling to defend clinical preference.

Across these profiles, common strategic levers are evident: differentiation through clinical evidence (including real-world outcomes), channel partnerships with oncology centers and hospital pharmacies, and payer engagement to secure reimbursement for prescription-strength products.

Prioritize clinical programs that deliver PROs and health‑economic endpoints. Investment in randomized prevention trials for high-risk radiotherapy populations and real‑world evidence demonstrating reduced care escalation can open reimbursement and formulary pathways.

Design product portfolios around clear clinical use cases. Successful portfolios separate prevention vs. acute treatment propositions, and prioritize silicone-occlusive, hydrogel, or steroid‑sparing chemistries where clinical guidance favors such approaches.

Target distribution and channel strategies to hospital pharmacy and oncology clinic workflows. While retail and online channels expand patient access, hospital purchasing and oncology protocols remain primary determinants of adoption for prescription-grade products.

Secure raw-material and manufacturing resilience. Silicone-based and hydrogel ingredients are central inputs; early supplier agreements and capacity planning reduce price and availability risk during demand spikes.

Adopt an evidence-led pricing and reimbursement playbook. Demonstrate not just symptomatic relief but reductions in downstream costs (dressings, wound-care consultations, treatment interruptions) to strengthen payer negotiations.

Consider bolt-on acquisitions to accelerate capability gaps. For firms lacking clinical evidence or hospital access, selective M&A or licensing deals can compress time-to-market without the full cost of organic development.

Invest in patient support and adherence solutions. Digital adherence programs, nurse-led helplines, and integrated packaging that supports clinician protocols can lift real-world effectiveness and brand preference.

Our Radiation Dermatitis Cream Market Research report is designed as a board-level decision tool for 2026 planning cycles. It contains:

A granular market model with historical (2020–2025) and forecast (2026–2032) sizing, sensitivity scenarios, and SKU-level unit economics.

Competitive landscaping with strategic profiles of leading and challenger firms, patent and pipeline mapping, and go-to-market benchmarks.

Regulatory and reimbursement dossiers aligned to major guidance and payer landscapes — including practical templates for preparing reimbursement submissions in key markets.

Operational playbooks covering manufacturing decisions, raw-material sourcing strategies, and distribution/channel optimization tailored for hospital pharmacy, retail, and e‑commerce dynamics.

Commercial strategies: pricing frameworks, contracting negotiation guides, and sales-force deployment models for oncology and dermatology channels.

M&A and partnership screening criteria, plus a short list of target archetypes for market-entry or capability-acquisition scenarios.

Our findings are synthesized from primary interviews with KOLs and procurement leads in oncology and dermatology, proprietary manufacturer and payer interviews, regulatory and guideline analyses, and triangulation with public company disclosures. The market model integrates demand drivers (radiotherapy utilization, treatment protocols), product-level adoption curves, and channel-specific uptake assumptions. Note: while this brief summarizes macro trends and strategic guidance, the full report contains the detailed segmentation matrices, regional splits, and company-level revenue estimates that underpin our recommendations.

Guideline updates: The clinical community increasingly favors steroid‑sparing topical management for mild-to-moderate dermatitis. Manufacturers should align labeling and study designs with these evolving recommendations to maximize clinician uptake.

Material science: Silicone occlusive and hydrogel platforms provide demonstrable physiologic benefits in moisture conservation. Securing ingredient quality and demonstrating comparative benefits will be a differentiator.

Payer behavior: Existing reimbursement routes in major markets (including certain Medicare pathways) are evolving. Firms that present robust cost-offset models and payer-ready dossiers will captivate formulary decision-makers.

For executives evaluating tactical moves in 2026, three immediate actions are high-impact:

Run a 90-day evidence gap assessment to identify essential RWE or randomized data required for reimbursement and clinician adoption.

Conduct a supply-chain stress test focused on silicone and hydrogel inputs and sign strategic supply agreements where vulnerabilities are identified.

Map strategic partnerships with oncology networks and hospital pharmacy buyers to pilot formulary adoption and gather early outcome data.

This industry brief is intentionally selective — it surfaces the strategic implications and high-level market dynamics but omits the full segmentation tables, regional breakdowns, and company revenue estimates to preserve the integrity of our proprietary modelling. The full Radiation Dermatitis Cream Market Research report from PW Consulting includes the complete data sets, scenario models, and downloadable templates that drive the recommendations above.

To request the full report or a bespoke executive briefing that maps these insights to your portfolio, contact PW Consulting via our website for licensing and advisory engagements.

— PW Consulting, Healthcare Strategy & Industry Analysis

For detailed analysis of this topic, please visit the official page:Radiation Dermatitis Cream Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com