Bearing Lubricant Market 2026: Strategic Playbook for Procurement, R&D and M&A — PW Consulting Industry Brief

Executive summary

As global manufacturing and mobility systems enter a second phase of electrification and efficiency-driven retrofit, bearing lubricants have moved from commodity inputs to strategic enablers of reliability, energy efficiency and regulatory compliance. PW Consulting’s latest Bearing Lubricant Market report (base year 2025) models the market across a six-year historical window and a seven-year forecast, delivering a granular, executable roadmap for decision-makers preparing for 2026.

Bearing Lubricant Market

Why this report matters for 2026 decision cycles

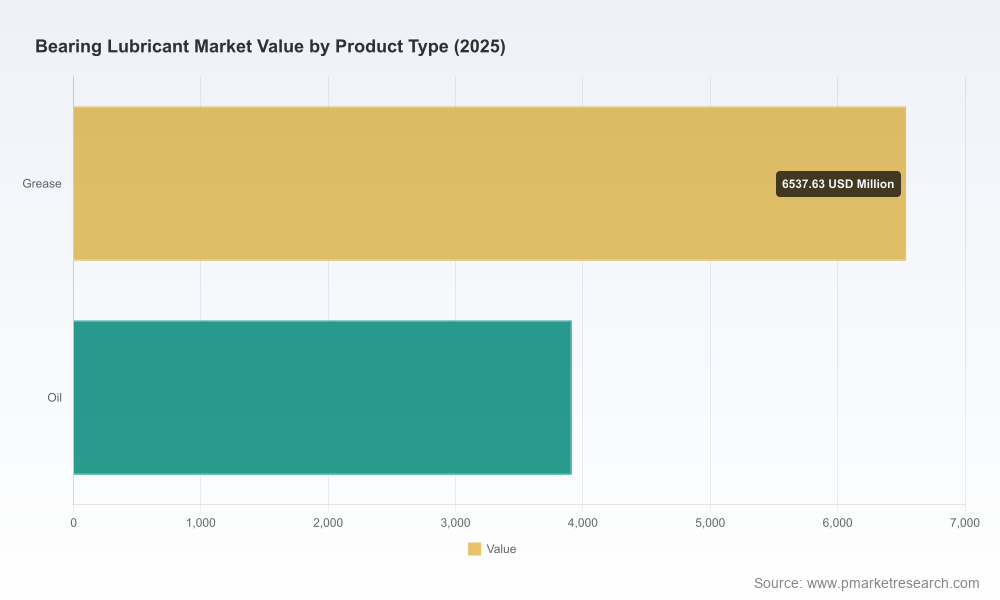

- Actionable foresight: Our forecast shows continued expansion from the 2025 baseline (USD 10,450 Million), projecting steady growth into the forecast period with an average CAGR of 4.12% and a 2032 market size in the neighborhood of USD 13,863 Million. These macro trajectories should inform capital allocation, inventory provisioning and pricing strategy planning for the year ahead.

- Concentration and consolidation signals: Market concentration metrics indicate meaningful scale benefits for leading suppliers (CR3 ≈ 38.4%, CR5 ≈ 52.15%), but there remains opportunity for niche differentiation — particularly in high-performance and regulated segments.

- Regulatory inflection points and raw-material volatility: 2026 will be the first operational year in which major regulatory and input-cost shifts converge, making integrated regulatory-compliance and procurement hedging plans imperative.

Market trajectory: what the numbers imply

From our historical analysis (2020–2025) through the forecast window (2026–2032), the bearing lubricant market demonstrates resilient, mid-single-digit growth driven by equipment electrification, longer-bearing life requirements, and a shift toward higher-performance formulations for demanding applications. The immediate implication for 2026 is twofold: firms must prepare for modest top-line growth while prioritizing margin protection against raw-material inflation and compliance-cost increases.

Bearing Lubricant Market

Competitive landscape — what incumbent and challenger strategies look like

The competitive map is shaped by legacy oil majors, specialist lubricant houses, and bearing OEMs that bundle lubricants with bearing systems. Our report profiles leading vendors and synthesizes recent commercial moves to extract strategic lessons for suppliers, users and investors.

Bearing Lubricant Market

- Klüber Lubrication (Germany) — Specialist focus on high-performance greases and oils, with strength in automotive, industrial and wind-energy bearings. Recent product launches targeting food-grade and high-speed applications underline a premium, compliance-first route to market.

- Shell Lubricants (Netherlands) — Global scale with advanced synthetic portfolios; strategic expansions into EV-bearing solutions indicate a play for OEM and Tier-1 partnerships in electrified powertrains.

- Mobil / ExxonMobil (USA) — Broad application reach, including electric-motor and food-grade bearings. Mobility of their brand and distribution remains a competitive edge for industrial conversions.

- SKF (Sweden) — An OEM-affiliated lubricant strategy that optimizes grease formulations for proprietary bearings. Compliance updates and product recertifications for wind turbines show an emphasis on lifecycle value for heavy applications.

- Timken (USA), Fuchs (Germany), Dow Corning / DuPont (USA), TotalEnergies, BP / Castrol, Chevron — Each brings differentiated capabilities: OEM integration, application-specific chemistries, silicone and PFPE offerings for precision, and scaled supply-chain footprints for heavy industry.

Recent product and compliance moves (e.g., food-grade launches, REACH-driven reformulations, and expanded EV-targeted greases) underscore three strategic themes suppliers are racing to master: regulatory-resilient chemistries, OEM co-development for electrified platforms, and geographically resilient distribution models.

Key 2026 risks and opportunities

- Input-cost pressure: Base oil volatility is no longer episodic. Our monitoring flagged a double-digit swing in base oil benchmarks into early 2026, with synthetic PAO pricing notably higher in key manufacturing hubs. Procurement teams must update hedging assumptions and consider formula redesigns that reduce exposure without degrading performance.

- Regulatory reshaping of formulations: The phase-out of certain persistent fluorinated chemistries under recent regulatory updates requires product reformulation roadmaps and accelerated testing for alternatives. Compliance-driven reformulation presents first-mover advantage for suppliers that can validate performance quickly against ISO and industry-specific standards.

- Trade policy and supply localization: Elevated tariffs and trade barriers in some corridors increase landed cost volatility. Manufacturers should evaluate near-shore sourcing and multi-sourcing strategies for both base stocks and additive packages.

- Electrification and OEM-specification growth: Bearing lubrication demand for electric motors and high-speed, low-vibration bearings is growing. This opens premiumization pathways — both in product price and in value-added services like condition-monitoring-compatible greases.

What PW Consulting’s report contains (practical deliverables)

Our report is designed for deployment by strategic and procurement teams preparing 2026 plans. Deliverables include:

- Top-line market model with historical calibration and scenario-based forecasts (base year 2025; forecast 2026–2032).

- Segment and application demand frameworks with elasticities and substitution matrices to estimate the financial impact of formulation changes and equipment shifts.

- Supplier benchmarking toolkit: capability matrices, go-to-market archetypes, R&D posture, and M&A heatmaps aligned to concentration indicators.

- Procurement playbook: hedging and contracting templates, specification harmonization checklists, and a supplier-risk scoring model incorporating tariffs, raw-material exposure and compliance timelines.

- Regulatory and chemistry risk register, including mitigation pathways for PFAS phase-outs and ISO-standard-driven testing requirements.

- Practical case studies and rapid-deployment pilots showing how leading buyers reduced lifecycle costs through lubricant optimization and predictive relubrication programs.

How executives should use this intelligence in 2026

- Procurement leaders: Integrate the report’s hedging scenarios into Q1 sourcing cycles; prioritize contracts that provide pricing collars or indexed mechanisms for base oil exposure. Implement multi-sourced specifications where regulatorily permissible.

- Product and R&D heads: Reassess additive platforms to accelerate PFAS-free and food-safe formulations. Use the supplier benchmarking to identify co-development partners for EV and high-speed applications.

- Operations and maintenance: Use the condition-monitoring matrices to shift from calendar-based to performance-based relubrication regimes, improving uptime while lowering total cost of ownership.

- M&A and corporate development: Apply the market-concentration and capability maps to prioritize tuck-in targets that add high-margin specialty formulations or regional manufacturing footprints to hedge trade-risk.

Competitive moves to watch in 2026

Keep an eye on three early indicators that signal winner-takes-most dynamics in selected subsegments:

- Speed of validated reformulation to replace restricted chemistries under REACH and related jurisdictions.

- Depth of technical partnerships with OEMs for electrified drivetrains and wind-energy bearings — co-engineered lubricants tend to lock-in long-term volume commitments.

- Ability to demonstrate lifecycle benefits through field data — players that can quantify bearing life extension or efficiency gains will command pricing power.

Case examples and recent vendor activity

Recent vendor activity reflects these strategic priorities. Leading companies have launched food-grade and EV-targeted greases, and updated established formulations to comply with recent REACH and ISO updates. This behavior is consistent with a market where product differentiation and regulatory compliance increasingly determine competitive advantage.

Why the detailed segment numbers are intentionally gated

PW Consulting’s approach balances transparency with the commercial necessity to convert deep, proprietary segment modeling into client engagements. This brief highlights strategic implications and directional figures (market size baselines and CAGR). The report contains full segmentation granularity, pricing curves, and regional demand matrices — these detailed models are gated to ensure commercial viability and to provide clients with interactive scenario tools that are updated in real time.

Next steps — how to leverage the report for immediate 2026 impact

- Schedule a 90-minute executive briefing with our industry practice to align the forecast scenarios with your 2026 planning calendar.

- Request the procurement playbook and supplier-risk model to run a Monte Carlo sensitivity on your raw-material exposure and tariff scenarios.

- Commission a tailored supplier-benchmark or M&A heatmap for priority segments where you seek scale or capability acquisition in 2026.

Conclusion

The bearing lubricant market in 2026 is neither a simple commodity game nor an exclusively premiumized niche. It is a layered market where regulatory compliance, raw-material management, and technical partnership with OEMs create differentiated pockets of value. PW Consulting’s Bearing Lubricant Market report provides the market sizing, scenario modeling and executable toolkits executives need to protect margins, accelerate product development and make opportunistic investments in 2026. For full access to the segmented models, pricing curves and interactive scenario tools, refer to the report landing page or contact our industry practice for a briefing.

For detailed analysis of this topic, please visit the official page:Bearing Lubricant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com