Spiral Bevel Gear Boxes Market — Strategic Outlook for 2026: A PW Consulting Intelligence Brief

PW Consulting’s latest market research report on Spiral Bevel Gear Boxes delivers a focused, action-oriented intelligence package designed to inform executive decisions in 2026. Using 2025 as the base year, the global market has been modeled across a 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 5.45%. After steady expansion through the early 2020s, the market is projected to continue ascending into the early 2030s — a trajectory that has immediate implications for capital allocation, product strategy, and supply‑chain planning.

Spiral Bevel Gear Boxes Market

Why this report matters for 2026 decision-makers

- Translates macro momentum (demonstrable recovery and sustained growth) into concrete decisions for product investment, capacity planning and M&A prioritization.

- Balances market sizing and scenario modeling with practical playbooks — enabling manufacturers, OEMs and investors to move from insight to implementation within quarters, not years.

- Highlights where margin expansion is achievable (precision, aftermarket and integrated systems) and where margin compression risk is highest (raw‑material exposure and commoditized components).

- Delivers a competitive heat map and supplier assessment to guide partner selection, localization, and technology licensing decisions.

Market snapshot and trajectory

Our analysis tracks the market’s evolution from the historical period (2020–2025) into a detailed forecast window (2026–2032). The industry expanded meaningfully during the historical window and reached a substantial global size in 2025 (base year). The near-term forecast shows a continuation of growth into 2026 and beyond, with the market expected to compound annually at c. 5.45% through 2032. This growth is not uniform: it is concentrated where system-level integration, precision engineering and aftermarket services intersect. The market concentration indicators in the report show a mid-level consolidation pattern (CR3 and CR5 metrics), signalling that the sector remains contestable — large suppliers exert influence, but opportunities persist for focused challengers and regional specialists.

Spiral Bevel Gear Boxes Market

Key market dynamics shaping 2026 decisions

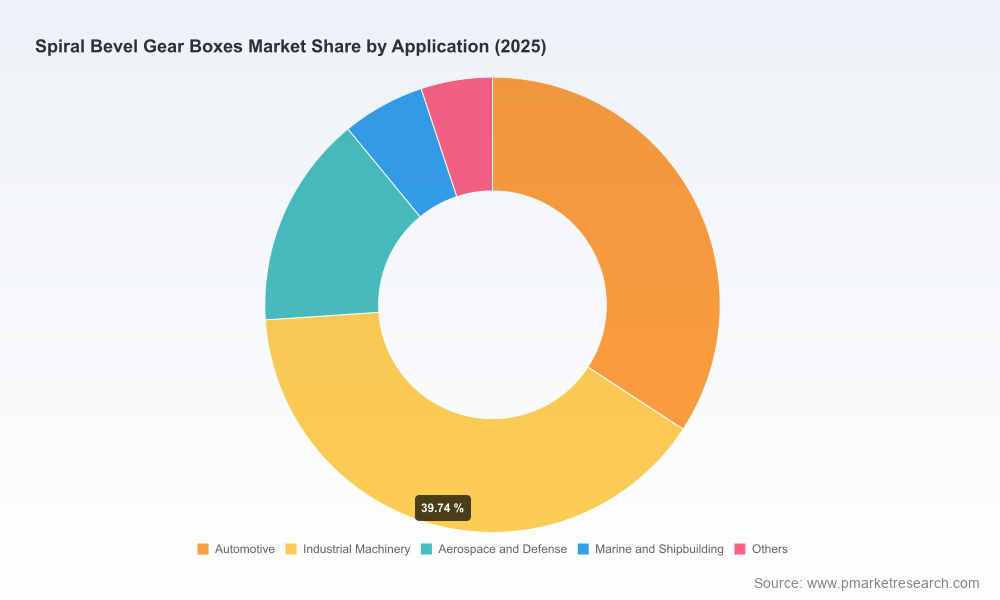

- End‑market interplay: Demand drivers include industrial automation (motion control), heavy‑duty power transmission, and premium segments such as aerospace/defense and precision robotics. Automotive transitions (including electrification of drivetrains and auxiliary systems) are reallocating requirements toward higher torque density and precision.

- Technology and differentiation: High-precision geometries, low-backlash assemblies and advanced heat‑treatment/hardening processes are premium levers. Providers that combine process control (Gleason/Klingelnberg workflows) with design-for-manufacturability capture superior margin.

- Aftermarket and service monetization: Service, repair, and retrofit represent outsized lifetime revenue per unit, especially for heavy-industrial and marine applications. Investing in diagnostics, spare-part availability and field support pays off faster than incremental product variants.

- Supply‑chain volatility: Production economics remain sensitive to alloy-steel and stainless-steel pricing dynamics (nickel, chromium inputs). Hedging, dual sourcing and localized processing (hardening/finishing) reduce cost-to-serve volatility.

- Standards and compliance: AGMA and ISO standards — including geometry and strength calculation protocols — are baseline requirements. Certification and traceability increasingly influence procurement decisions among tier‑one OEMs and defense buyers.

Supply‑side considerations and risks

Raw material cost swings and capacity constraints in niche finishing processes (case hardening, grinding for low backlash) are the two most immediate supply risks. Manufacturers that integrate downstream finishing or secure long‑term arrangements with specialty heat‑treat vendors will be better positioned on lead times and margin protection in 2026. Parallel mitigation measures — strategic safety stock, forward contracts for critical alloys, and selective vertical integration — are profiled with scenario modeling in the report.

Spiral Bevel Gear Boxes Market

Competitive landscape — strategic read on core players

The report provides a qualitative and quantitative competitive benchmarking of established suppliers and fast‑moving niche players. Below is a succinct strategic characterization of the principal participants we track:

- Amarillo Gear Company (Amarillo, Texas) — Depth in heavy‑duty alloy steel spiral bevel gears and right‑angle drives. Strengths: material engineering for rugged applications and broad product breadth for industrial use. Strategic implication: attractive partner or acquisition target for companies seeking to bolster heavy‑duty credentials and metallurgy competencies.

- TANDLER (Bremen, Germany) — High‑precision, low‑backlash gearboxes with servo and stainless options. Strengths: precision engineering and performance positioning for motion‑control markets. Strategic implication: a technology benchmark for premium segments; licensing or distribution partnerships can accelerate access to servo‑grade assemblies.

- GAM Enterprises, LLC (Illinois, USA) — Highly configurable miniature gearboxes with high efficiency and motor‑mount ecosystems. Strengths: compact, high torque density solutions for precision automation. Strategic implication: an inorganic/strategic partnership candidate for firms targeting miniaturized applications and robotics.

- KHK Gears (Japan) — Global manufacturer of standard and custom gears for 90° shaft solutions. Strengths: high-volume manufacturing and global reach. Strategic implication: core competitor in commoditized product lines; collaboration on standardized modules can lower cost-to-serve.

- Circle Gear & Machine Co. (Cicero, Illinois) — Custom spiral bevel gears using Gleason systems; reverse-engineering capability. Strengths: flexibility in materials and bespoke production. Strategic implication: go‑to partner for retrofit work and rapid prototyping for OEMs.

- Bevel Gears (India) Pvt. Ltd. (Bangalore, India) — Longstanding producer of ground spiral bevel gears across a wide diameter range. Strengths: breadth, cost competitiveness, and scale in specific regional markets. Strategic implication: near‑term outsourcing option for cost reduction, with caveats around delivery lead times and certification for regulated end uses.

- Superior Gearbox Company (USA) — OEM-focused bevel drives emphasizing service life and quiet operation. Strengths: established OEM relationships and reputation for reliability. Strategic implication: candidate for long-term supply agreements and co‑development for OEM programs.

- Overton Chicago Gear (USA) — High‑precision large‑diameter gears including hard-cut and Klingelnberg types for mining/marine. Strengths: capability for large, demanding applications. Strategic implication: strategic supplier for large project wins where scale and precision converge.

Recent product and market moves to note

- Product communications and catalog enrichments that clarify application boundaries (e.g., recent explanatory content on TANDLER gearboxes) are shortening buyer education cycles — a tactical advantage for firms with clear specification documentation.

- New product introductions in the miniature, high-torque-density segment signal growing demand in robotics and precision motion control. Manufacturers should evaluate whether their roadmap addresses both torque density and configurability.

Actionable strategic recommendations for 2026

- Prioritize investment in precision and low‑backlash product lines where customers will pay a premium (robotics, motion control, aerospace). Develop modular architectures to serve multiple end markets from a common platform.

- Build a tiered aftermarket strategy: fast spare parts, condition‑based maintenance offerings, and long‑term service contracts to convert installed base into predictable recurring revenue.

- Mitigate raw‑material exposure via a three‑pronged approach — long‑lead procurement, regional processing partnerships, and material‑substitution R&D where feasible.

- Pursue targeted partnerships or bolt‑on acquisitions: precision specialists to accelerate entry into high-margin niches; regional manufacturers to reduce logistical cost and lead times.

- Invest in certification, traceability and digital product passports aligned with AGMA/ISO norms to win regulated procurement and defense contracts.

- Differentiate on time-to‑market through digital configuration tools, 3D‑printing‑enabled prototyping and a streamlined quotation-to-delivery process.

- Evaluate price segmentation and contract structures that transfer part of raw-material inflation risk to long-term customers through index‑linked clauses.

What the full PW Consulting report delivers (practical contents)

The report is structured for direct operational use. Key deliverables include:

- Top‑line market size and validated forecast models (base year 2025; detailed 2026–2032 scenarios with sensitivity analysis).

- Segmentation frameworks by product type, application and region (with dynamics and buyer behavior mapping).

- Competitive benchmarking and detailed company profiles, including capability matrices and go‑to‑market positioning.

- Supply‑chain heat map, raw‑material impact analysis, and mitigation playbooks.

- Technology radar on manufacturing and materials (heat treatment, grinding, inspection systems) and an innovation adoption timeline.

- Commercial playbooks: pricing strategies, channel strategies, aftermarket monetization templates, and partner selection criteria.

- Excel databook and scenario models ready for executive and board-level briefings.

PW Consulting’s approach is intentionally pragmatic: the public brief above surfaces the most consequential themes and immediate actions while preserving the granular segmentation and proprietary models that underpin high-confidence recommendations. For procurement managers, product leaders, and private equity investors in 2026, the choice will be between tactical survival (managing cost and availability) and strategic advantage (securing precision platforms, aftermarket revenues and supply resilience). The full report equips you to choose and operationalize the latter.

Next steps

To access the complete dataset, company scorecards and executable 90‑day action plans derived from our models, please visit our report landing page. The full intelligence package includes downloadable models and optional advisory hours for bespoke scenario planning and integration into your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Spiral Bevel Gear Boxes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com