Argentinas Team Chemistry for the 2026 World Cup

Gardening |

2026-06-02 02:09:29

PW Consulting’s new market research brief on the Piston Connecting Rod Unit market delivers a compact, action-oriented view intended to shape executive decisions for 2026 and beyond. Built on a consistent historical baseline (2020–2025) and an out-year forecast (2026–2032), the analysis synthesizes macro trajectories, supplier positioning, raw-material dynamics, and practical playbooks that procurement, product and corporate strategy teams can act on immediately.

Piston Connecting Rod Unit Market

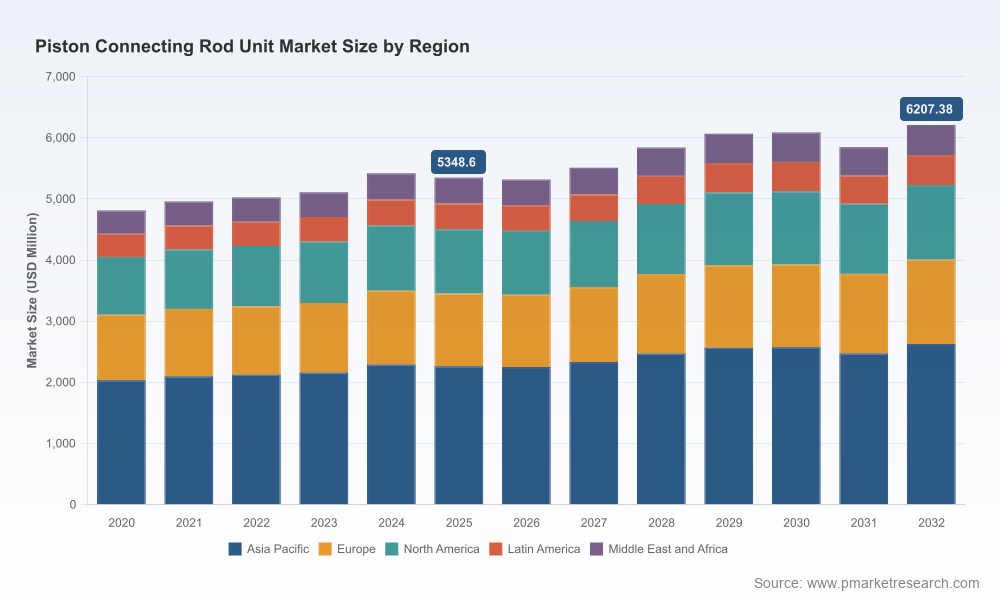

Constrained but stable topline: after a multi-year recovery through 2024, our market sizing shows a near‑term recalibration in 2025–2026 and an overall moderate expansion through 2032. The market recorded USD 5,348.6 Million in 2025, a projected USD 5,316.93 Million in 2026, and is expected to reach USD 6,207.38 Million by 2032 — representing a compound annual growth rate (CAGR) of 2.15% across the 2026–2032 forecast window. This profile is fundamentally different from boom-cycle markets: it requires allocation discipline, margin protection strategies, and selective growth investments.

Piston Connecting Rod Unit Market

Decision timing matters: small shifts in raw-material costs, forging capacity utilization, or OEM engineering direction can meaningfully alter supplier economics in a market growing at a low single-digit CAGR. This means 2026 is a pivot year for aligning procurement contracts, capital investments and R&D roadmaps with medium-term demand visibility.

Piston Connecting Rod Unit Market

Concentration and competition: the market exhibits moderate concentration (top‑three players ~31.4%, top‑five ~45.8%), which creates both supplier leverage pockets and attractive niches for specialist providers. The competitive topology supports targeted consolidation plays and bolt‑on acquisitions for OEMs and Tier‑1s seeking near-term capacity or technology access.

Robust market sizing and credible forecasting: a transparent reconciliation of historical production, aftermarket flows and macro vehicle/engine trends framed by scenario-based projections for 2026–2032.

Actionable cost and margin models: component-level cost curves tied to primary manufacturing routes (forging, powder metallurgy, casting), with sensitivity modules that quantify margin exposure to steel price moves and capacity utilization.

Supplier heatmaps and capability benchmarking: a scored view of global suppliers across technology (e.g., high-strength alloys, titanium, powder metal), quality systems (ISO and OEM approvals), geographic footprint, and scale—designed to inform sourcing RFIs/RFPs and make-vs-buy decisions.

Product and technology roadmap insights: evaluation of advanced forging processes, alloy selection, precision machining investments and lightweighting trade-offs that impact total system mass, NVH (noise, vibration, harshness) and engine efficiency.

Commercial playbooks: go-to-market approaches for OEMs, Tier‑1s and independent manufacturers—from captive supply optimization to aftermarket scaling, pricing strategies, and distributor channel design.

M&A and partnership templates: prioritized target archetypes, valuation considerations in a low‑growth environment, and integration checklists emphasizing quality systems, IP, and production ramp risk.

Risk matrix and mitigation plans: raw-material volatility, capacity misalignment, regulatory compliance, and supplier single‑source exposures — each mapped to mitigation levers and contingency triggers.

Raw-material and input-price behavior: forged alloy steel remains the predominant raw material for piston connecting rod manufacture, and steel benchmark prices and availability will continue to be primary cost levers. Recent market signals show steel benchmark levels that matter to producers’ cost pass-through and capital planning, while projections indicate subdued recovery in prices amid overcapacity — conditions that favor cost discipline but also compress margins for lower-efficiency operators.

Technology and material migration: manufacturers are investing in advanced forging, new alloys and precision‑engineering methods to improve strength‑to‑weight ratios — especially in performance and premium segments. Powder metallurgy and specialty materials (including titanium in niche racing/performance applications) are growth vectors, but these require different supply chains and CAPEX profiles.

Regulatory and quality compliance: OEM expectations and aftermarket acceptance hinge on validated quality systems; suppliers maintaining ISO 9001:2015 and OEM material/dimensional approval will continue to command preferential access in global supply chains.

Market structure implications: moderate market concentration coupled with many specialized regional suppliers creates opportunities for selective consolidation, strategic sourcing, and captive-supplier partnerships to secure advanced capabilities or to de-risk supply continuity.

Our competitive analysis synthesizes corporate positioning, capabilities and strategic intent across established suppliers and high‑performance specialists. Notable players profiled in the report include global integrators and specialist manufacturers:

Mahle GmbH (Stuttgart, Germany) — a diversified engine component supplier with integrated piston‑connecting rod offerings; its scale and OEM relationships make it a bellwether for systems-based value capture.

thyssenkrupp Forged Technologies (Essen, Germany) — focused on forged crankshafts and rods across duty ranges; strength in heavy‑duty and mid‑range segments positions it well where scale and metallurgical competence matter.

CP‑Carrillo (Irvine, CA, USA) and Pankl Racing Systems (Austria) — performance and racing specialists that are early adopters of exotic alloys and titanium; their product introductions often signal material and process innovations that later diffuse into mainstream applications.

AECO Products / Arrow Engine Parts (India) and Shriram Pistons and Rings Ltd. (India) — large‑scale manufacturers with broad application portfolios (automotive, agricultural, marine) and export capabilities that are important for cost-competitive supply and aftermarket channels.

Regional and boutique specialists — including Chorng Ko (TOP Rod), Oliver Racing Parts, GRP, MGP, Pauter Machine and Motorservice (Kolbenschmidt) — which capture performance niches and aftermarket opportunities; these firms are frequently targets for OEM partnerships, co-development, or private equity interest.

Recent corporate actions that matter for 2026 strategy include alliance and product developments in the performance segment and engineering updates impacting service and OEM requirements. These actions validate two strategic themes: (1) continued investment in high‑strength, lightweight solutions; and (2) incremental aftermarket and service activity that requires updated service instructions and component standards.

Procurement: lock in multi‑year frameworks indexed to validated steel benchmarks, negotiate capacity‑with‑options clauses to manage demand volatility, and run dual‑sourcing pilots for critical SKUs to mitigate single‑site risk.

Product and R&D: prioritize alloy/process investments that improve fatigue life per unit mass, and establish rapid validation pathways with OEMs to shorten adoption cycles for lighter or powder‑metal solutions.

Finance and M&A: focus on targets that provide either immediate cost savings through offshoring/scale or complementary technological capabilities—valuations should reflect slow structural growth but high strategic optionality.

Aftermarket and service: capitalize on service instruction updates and targeted component releases by OEMs and aftermarket players to grow higher-margin replacement channels and extended‑lifecycle services.

The full Piston Connecting Rod Unit Market report is designed as a decision‑centric toolkit: it pairs quantitative market constructs (including reconciled historicals and scenario forecasts) with qualitative supplier assessments, technical deep dives and executable playbooks. For 2026, the report’s value is threefold: it clarifies where to preserve margins in a low‑growth environment, identifies where selective investment will unlock disproportionate returns, and prescribes the sourcing and product moves that reduce operational risk.

We deliberately avoid publishing detailed segment and regional breakout in this press brief to preserve the competitive advantage that granular data affords our clients. The full dataset — including regional, material and application splits, supplier scorecards, and modelable Excel workbooks — is available through PW Consulting’s report page and client engagement channels.

Run a 90‑day sourcing stress test using our steel‑price sensitivity templates to determine breakpoint triggers for contract re‑negotiation.

Initiate a small number of co‑development pilots with specialist alloy suppliers to validate lightweighting options in a controlled program.

Map critical SKUs to supplier concentration and quality certifications; create contingency plans where single‑source exposures intersect with OEM program timelines.

Review M&A shortlist against the report’s target archetypes and integration checklists to accelerate due diligence.

To obtain the full report, datasets and client‑grade models that underpin these strategic recommendations, please visit the PW Consulting report page. Our analysts are available to brief executive teams and to run a tailored workshop that translates market scenarios into a prioritized action plan for 2026.

For detailed analysis of this topic, please visit the official page:Piston Connecting Rod Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com