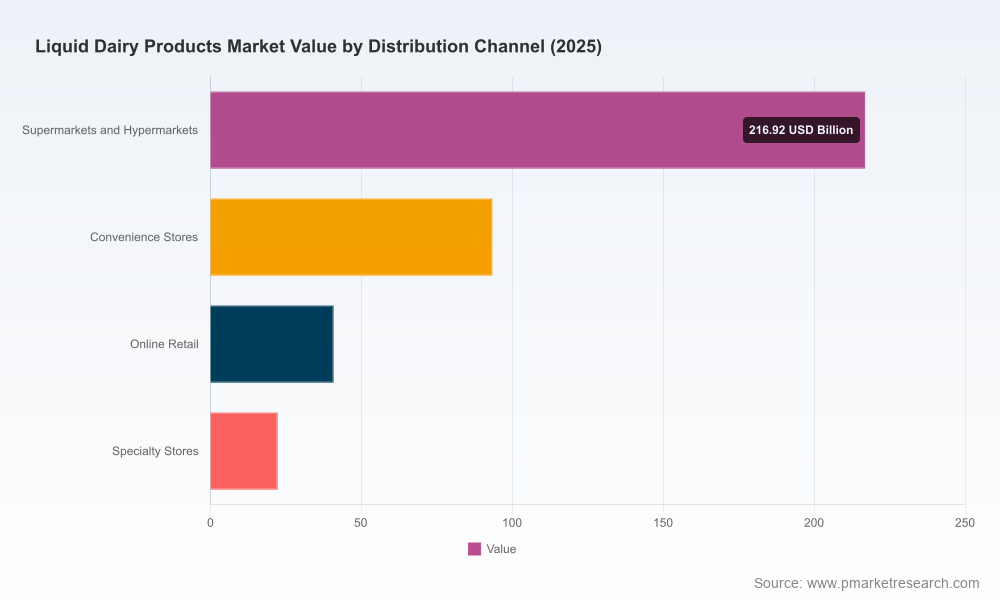

Liquid Dairy Products Market — Strategic Outlook 2026: PW Consulting Market Brief

Executive summary

The global liquid dairy products market reached an estimated USD 373.6 Billion in 2025 and, under PW Consulting’s baseline scenario, is projected to expand to roughly USD 508.5 Billion by 2032. This trajectory represents a compound annual growth rate (CAGR) of approximately 4.51% across the 2026–2032 forecast window. After an uneven recovery from 2020–2022, demand dynamics stabilized in 2023–2025, driven by renewed consumer demand in emerging markets, innovation in value-added beverages, and renewed institutional purchasing patterns.

Liquid Dairy Products Market

This market brief translates those macro dynamics into concrete strategic implications for executives preparing budgets, capex plans, commercial initiatives, and M&A activity in 2026. It highlights where upside is most likely, where margin pressure will persist, and what capabilities will determine winners as the sector shifts from volume-driven recovery to value-driven growth.

Liquid Dairy Products Market

Why PW Consulting’s 2026 perspective matters

- Actionable horizon: We align the market forecast (base year 2025; forecast 2026–2032) to the fiscal and investment cycles most corporate leadership teams use for 2026 planning.

- Decision-focused outputs: Our analysis translates demand and cost scenarios into prioritized strategic initiatives — pricing levers, channel investments, and capacity decisions — rather than simply reporting historical statistics.

- Risk-adjusted view: Each recommendation is stress-tested across commodity cycles, regulatory shifts, and supply-chain disruptions observed through Q1–Q2 2026 intelligence.

Market dynamics shaping 2026 decisions

Three interlocking dynamics will define competitive advantage in 2026:

Liquid Dairy Products Market

- Supply-side pressure and input-cost volatility. Global milk production rose in 2025 (estimated increase in the low single digits year-on-year), creating temporary oversupply that exerted downward pressure on raw milk prices into early 2026. In the U.S., all-milk price forecasts for 2026 reflect this rebalancing. For CFOs, this creates a narrow window to re-price finished goods and rebalance margin via mix and cost-to-serve optimizations.

- Regulatory and programmatic shifts that alter institutional demand profiles. Recent policy changes — including national moves to align animal-health standards and new school-meal legislation in the United States authorizing additional fluid milk options — will reshape category demand at scale. Manufacturers and ingredient suppliers must sequence compliance investments and reformulate timelines against market access priorities.

- Channel and product innovation accelerating premiumization and convenience plays. Innovations in packaging, shelf-stable formats, and functional liquid beverages continue to increase willingness-to-pay in urban consumers across multiple regions. At the same time, online and convenience channels are forcing shorter lead times and restructured distribution economics.

Competitive landscape — implication for 2026 strategies

The market remains moderately fragmented with concentration ratios that leave room for both global champions and strong regional challengers. The top three players account for roughly one-fifth of the market by revenue, while the top five approach just over one-third — a structure that favors scale in procurement and distribution but leaves niches for differentiated local players.

- Global scale players (e.g., Lactalis, Nestlé, Danone): These firms retain advantages in procurement, cross-border distribution, and branded innovation pipelines. Strategic moves to watch in 2026 include targeted capacity investments, platform acquisitions to secure route-to-market, and accelerated launches of value-added liquid dairy beverages tailored to health and convenience trends.

- Large cooperatives and regional leaders (e.g., DFA, Fonterra, Amul, Yili): Cooperatives and national champions are doubling down on supply-chain integration and domestic market penetration. Expect partnership activity — co-manufacturing, co-pack, ingredient supply agreements — particularly where export orientation meets domestic demand growth.

- Specialized and premium innovators (e.g., Meiji, Arla, FrieslandCampina, Bright Dairy, Saputo): These players compete on product differentiation (organic, lactose-free, premium drinking yogurts) and faster NPD cycles. In 2026, their success will hinge on nimble SKUs and targeted marketing to premium urban cohorts.

Recent corporate moves underscore these dynamics: packaging and prototyping investment by systems suppliers to accelerate time-to-market; factory capacity expansions targeting export corridors; and new distribution infrastructure in key growth markets. For incumbents, responding to competitor capex with complementary capabilities (e.g., data-driven route-to-market optimization) will be a critical priority.

Operational levers and playbooks included in the report

PW Consulting’s full report is designed for operators who must make 2026 decisions today. Key operational modules include:

- Forward-looking P&L scenarios linking commodity cost curves to finished-good pricing across three demand scenarios (base, upside, downside).

- Channel economics playbook — normalized cost-to-serve and margin models for modern trade, convenience, and digital channels, with recommended investment sequencing for 12–24 month horizons.

- Capex prioritization matrix — ROI-calibrated guidance on capacity expansion, packaging automation, and cold-chain investments under varying utilization and freight-cost assumptions.

- M&A and partnership heatmaps — a shortlist of capability gaps (e.g., aseptic processing, regional cold-chain networks, branded functional formats) and the types of targets that unlock immediate synergies.

- Regulatory and food-safety readiness checklist tailored to major jurisdictions with actionable timelines — including compliance pathways triggered by recent policy shifts and outbreak surveillance protocols.

Note: this brief intentionally omits the granular segment tables and regional/applicational splits contained in the full report. Those detailed breakdowns — essential for SKU-level pricing, territorial prioritization, and specific M&A target sizing — are available via our subscription portal and downloadable report package.

Risks and mitigation playbook for 2026

- Price compression risk: Short-term oversupply could compress margins. Mitigations include dynamic pricing pilots, SKU rationalization, and hedged supply contracts.

- Regulatory shocks: New animal-health rules or school-meal policy shifts can reallocate volume. Maintain agile formulations and prioritize certifications in markets with pending regulatory alignment.

- Food-safety events: Ongoing investigations into product-borne outbreaks underscore the need for robust traceability and rapid recall playbooks. Invest in batch-level digital traceability and third-party food-safety audits.

- Distribution disruption: Channel shift to convenience and e-commerce requires redesigned logistics. Test micro-distribution hubs and third-party fulfillment pilots before full rollout.

How commercial leaders should act in 2026

- Rebase 2026 pricing assumptions on the scenario models we provide; do not rely exclusively on 2025 realized prices.

- Prioritize high-return capex that improves flexibility (e.g., modular packaging lines that can handle aseptic and chilled SKUs) over single-purpose expansions.

- Lock in strategic raw-milk supply contracts with tiered pricing to smooth input volatility, pairing these with demand-shaping commercial incentives to protect utilization.

- Create a 12–18 month product roadmap that balances premiumization with accessibility — use targeted small-batch launches to validate consumer willingness-to-pay before national rollouts.

- Build a monitoring dashboard that combines inventory, commodity indices, and regulatory events to trigger pre-defined strategic responses.

What’s in the full PW Consulting report (high level)

- Proprietary market-sizing and 2026–2032 forecast models (with downloadable spreadsheets)

- Channel and SKU-level margin simulators and elasticity matrices

- Competitive scorecards with capability maps and prioritized M&A/partnership targets

- Regulatory matrix and compliance timelines for priority markets

- Operational playbooks: capex prioritization, route-to-market optimization, and crisis readiness templates

Conclusion and next steps

As 2026 planning cycles begin, executives need not only the headline growth rate — a market expanding from USD 373.6 Billion in 2025 to an estimated USD 508.5 Billion by 2032 (CAGR ~4.51%) — but the tactical translation of that growth into prioritized investments and mitigations. PW Consulting’s Liquid Dairy Products Market report provides that translation: forecasting that informs pricing, capex, channel and M&A choices, and a risk playbook tested against recent supply and regulatory signals.

For boards and executive teams preparing 2026 strategy workshops, the full report provides the validated inputs and scenario tools needed to finalize budgets and strategic roadmaps. To access the detailed segmentation tables, company-level benchmarking, and downloadable decision-support models, please visit our report portal to obtain the complete intelligence package.

For detailed analysis of this topic, please visit the official page:Liquid Dairy Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com