زراعة الثدي في الرياض وأحدث معايير السلامة الطبية

Home |

2026-06-16 04:22:45

PW Consulting’s newest market study on the Worldwide Buruli Ulcer Treatment Market (base year 2025; historical 2020–2025; forecast 2026–2032) frames a pragmatic growth story for decision-makers preparing strategies in 2026. The market has expanded from roughly USD 62.2 Million in 2020 to about USD 78.5 Million in 2025 and is forecast to surpass USD 108.9 Million by 2032, reflecting a steady compound annual growth rate (CAGR) of 4.8% over the forecast horizon. These headline metrics capture a market that is modest in commercial scale but rich in public-health and donor-driven dynamics — an environment where clinical guidelines, prequalification pathways, and procurement practices matter as much as product differentiation.

Worldwide Buruli Ulcer Treatment Market

Actionable timing: 2026 is the inflection year when incremental demand (driven by guideline consolidation and program expansion) meets supply-side rationalization. Our analysis isolates the moments where procurement cycles, prequalification updates, and donor commitments will create windows for market entry or scale-up.

Worldwide Buruli Ulcer Treatment Market

Risk-aware investment: The market’s modest absolute size belies concentrated supplier dynamics and dependence on generic antibiotic production. Investors and manufacturers need diagnostic frameworks to weigh low-margin supply economics against strategic access and corporate responsibility objectives.

Worldwide Buruli Ulcer Treatment Market

Program-level decision support: For ministries of health, international donors, and global NGOs, the report translates epidemiological burden, WHO policy direction, and procurement mechanics into operational scenarios for budgeting, stockpiling, and partner selection in 2026.

The market’s near-term growth is driven by three interlocking forces: (1) clinical standardization, (2) sustained donor-supported treatment programmes in endemic geographies, and (3) constrained commercial incentives that preserve a generics-based supply model. The WHO’s confirmation of an eight-week rifampicin–clarithromycin daily regimen as first-line care (October 2023 guidance) has sharpened procurement specifications and reduced regimen variability — a clear positive for predictable demand aggregation.

Our quantitative baseline shows progression from the low-60s (Million USD) in 2020 to the high-70s in 2025, with a steady climb through the forecast period to reach just under USD 109 Million by 2032 under the central-case 4.8% CAGR. This trajectory reflects predictable program roll-outs, incremental case detection improvements, and a slow but steady shift toward integrated wound-care services and rehabilitation. Importantly, the market’s commercial scale remains tightly coupled to public health funding flows rather than private payer dynamics.

Clinical and regulatory codification: WHO’s guideline reaffirmation streamlines product specifications and supports larger, pooled tenders — a structural tailwind for suppliers who can meet prequalification and supply-security criteria.

Supplier concentration and sourcing realities: The market displays a moderate concentration profile; a handful of producers account for the lion’s share of supply. This concentration is reinforced by reliance on WHO-prequalified generics and the operational advantages of established manufacturers in low-cost geographies.

Procurement and reimbursement mechanics: Treatment is often provided free through WHO-supported national programs in endemic regions, which elevates the importance of procurement compliance, donor alignment, and sustained funding commitments.

Downstream care complexity: Beyond antibiotics, wound management, surgical interventions for advanced lesions, and rehabilitation services are material components of total market value and operational requirements — areas where service providers, device suppliers, and capacity-builders can create differentiated propositions.

Raw material and manufacturing risk: The supply chain is dependent on generic antibiotic producers in India and similar hubs. This concentration introduces single-source risk vectors — regulatory, logistical, or commodity-driven — that can materially affect availability and pricing in short cycles.

The competitive map is dominated by manufacturers with WHO prequalification credentials, leading international generics divisions, and established players serving global health tenders. Our report profiles the core players active in the treatment supply chain and evaluates their strategic positioning along three axes: regulatory standing, product breadth, and supply reliability.

Macleods Pharmaceuticals and other WHO-prequalified suppliers: These organisations are central to programme procurement, having secured prequalification for key multidrug therapy packs. Prequalification remains the single most important credential for accessing large-scale donor-funded tenders and national programme contracts.

Sandoz (Novartis division): As a major generics provider with global reach, Sandoz plays a role in stabilising supply for standard antibiotics used in Buruli ulcer regimens. Its scale enables competitive pricing and broad distribution networks.

Cipla: A major Indian generic manufacturer with capabilities across rifampicin and other antibiotics relevant to neglected tropical diseases; Cipla’s presence reinforces the market’s dependence on competitively priced, WHO-compliant generics.

Recent developments that reshape supplier strategy include WHO’s October 2023 guideline update standardising regimen duration and the earlier WHO prequalification events that materially improved access to fixed-dose combinations. These regulatory milestones compress time-to-contract for compliant suppliers and raise the bar for new entrants lacking prequalification credentials.

Our full study is designed as a decision-grade toolkit for 2026. Key deliverables include:

A validated market-size model (2020–2032) with scenario testing for donor funding variations and program expansion assumptions.

Supply-chain vulnerability mapping that highlights manufacturing concentration points, raw-material exposure, and mitigation options for continuity of supply.

Procurement playbooks for ministries and international buyers that align tender design with prequalification, batch testing, and delivery risk management.

Competitive scorecards and supplier due-diligence templates that crystallise how to evaluate capacity, regulatory compliance, and supply security.

Go-to-market frameworks for manufacturers and service providers, including partnership models with NGOs, bundling strategies (antibiotics + wound care), and donor engagement roadmaps.

Policy briefs for advocacy groups that translate clinical guidelines into funding asks, integration into national programmes, and surveillance investment priorities.

For manufacturers: Prioritise WHO prequalification and supply-security guarantees. Scale labelling, packaging, and distribution capabilities to meet pooled procurement specifications. Consider strategic alliances with wound-care and rehabilitation service providers to offer bundled solutions that increase programme value.

For donors and procurement agencies: Use pooled tenders and multi-year contracting to stabilise pricing and incentivise suppliers to maintain buffer capacity. Invest in supplier diversification and conditional financing to reduce single-source risk.

For national health programmes: Align national formularies and procurement policies with WHO recommendations, and invest in integrated care pathways that encompass antibiotics, wound management, and rehabilitation. Prioritise surveillance in high-burden districts to improve demand forecasting.

For investors and corporate strategic teams: Evaluate upstream investments in generic antibiotic capacity and downstream service bundles. Financial returns in this market are modest per unit, but strategic value accrues through scale economies in adjacent neglected-disease portfolios and reputational benefits in global health partnerships.

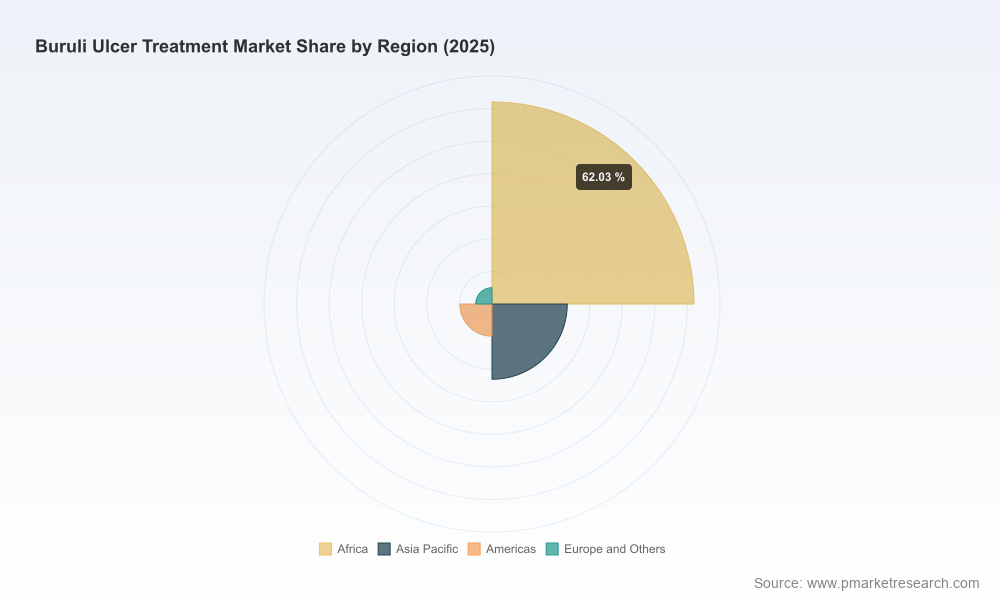

This article highlights the analytical depth and practical orientation of PW Consulting’s full report while intentionally withholding granular subsegment tables and detailed regional percentages. That “trailer” approach preserves the report’s commercial value while delivering enough evidence-based insight to inform high-level 2026 decisions. The full dataset includes disaggregated regional and treatment-type forecasts, supplier share analytics, and downloadable procurement templates that are critical for operational planning.

Leverage the market-size scenarios to stress-test 2026 procurement budgets under donor-funding upside/downside cases.

Deploy the supplier due-diligence templates before tender cycles to ensure continuity of supply and WHO-compliance.

Use the go-to-market frameworks to structure partnership pilots that bundle antibiotics with wound-care interventions in targeted high-burden districts.

PW Consulting’s full Worldwide Buruli Ulcer Treatment Market report provides the complete quantitative models, supplier scorecards, and playbooks that operational teams, strategy groups, and procurement officials need for confident decisions in 2026. For access to the full dataset, downloadable templates, and bespoke advisory engagements, please visit the report landing page on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Worldwide Buruli Ulcer Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com