Prediksi Togel Online Lengkap dan Detail

Art |

2026-06-23 10:52:45

As healthcare providers, device manufacturers, investors and research institutions prepare budgets and roadmaps for 2026, PW Consulting’s latest market study on the Worldwide Functional Magnetic Resonance Imaging (fMRI) market frames both opportunity and risk with a data-driven, decision-oriented lens. Our analysis shows the fMRI market expanding from roughly USD 3.03 billion in 2020 to about USD 4.12 billion in 2025, and we forecast growth to approximately USD 6.37 billion by 2032—a compound annual growth rate (CAGR) of 6.42% across the 2026–2032 forecast horizon. This briefing highlights the strategic implications our report surfaces for allocation of capital, product strategy, clinical adoption, and ecosystem partnerships in 2026—while reserving the granular segment tables and proprietary vendor scorecards for the full report.

Worldwide Functional Magnetic Resonance Imaging Market

Market momentum: The fMRI market has shown steady expansion through 2020–2025 and enters 2026 from a stronger base. That momentum reflects simultaneous advances in scanner hardware, AI-enabled reconstruction and workflow automation, and increasing clinical/research use-cases in neuroscience and pre-surgical planning.

Worldwide Functional Magnetic Resonance Imaging Market

Concentration dynamics: Market concentration remains meaningful—our CR3 and CR5 analysis indicates leading vendors control a majority of market value. That structure creates a differentiated competitive landscape where technology platform decisions and OEM partnerships materially affect procurement risk and long-term service economics.

Worldwide Functional Magnetic Resonance Imaging Market

Disruption vectors: Raw-material shocks, regulatory shifts favoring low-helium platforms, and rapid software-enabled innovation (AI and cloud workflows) are simultaneously compressing total cost of ownership (TCO) uncertainty and creating windows for competitive substitution.

CapEx vs. OpEx trade-offs: With helium supply volatility and the emergence of virtually helium-free platforms gaining regulatory clearance, the classic trade-off between lower upfront cost and lower long‑term service exposure is shifting. Procurement teams should re-run three- to seven-year TCO models that incorporate helium contingency scenarios, service-partner concentration and software upgrade pathways rather than relying on historical service patterns alone.

Platform roadmaps matter more than ever: Buyers should prioritize vendor roadmaps that explicitly address multi-site harmonization, AI-enabled reconstruction, and validated fMRI workflows for both task-based and resting-state paradigms. Interoperability with trial platforms and standardized stimulus/response toolchains is an increasingly important procurement criterion for academic health systems and CROs running multi-center neuroimaging studies.

Software drives differentiation: As image acquisition hardware approaches physical performance bounds in mainstream field strengths, software (AI reconstruction, motion correction, accelerated sequences, and integrated analysis pipelines) is the primary lever for clinical throughput and diagnostic yield. Decision criteria should include validated clinical endpoints, head-to-head time-to-diagnosis metrics, and upgrade licensing models.

Service models and global supply chains: Given recent helium spot-price volatility and periodic supply disruptions, health systems should require contract-level guarantees and contingency clauses related to spare-parts availability and magnet maintenance. M&A and partnership evaluations should explicitly model service network resilience and regional service coverage.

Regulatory clarity shortens adoption cycles: The recent wave of 510(k) clearances for low‑helium and low‑cost field platforms expedites the path from pilot to scale for many health systems. Clinical teams and procurement should coordinate early with regulatory/compliance functions to accelerate local approvals and billing pathway analysis.

PW Consulting’s full study is structured to be immediately operational for executives and program leads. Highlights of deliverables include:

Market sizing and methodology: Transparent, auditable top‑down and bottom‑up models covering historicals and forecasts to 2032, with scenario variants for supply shocks and accelerated software adoption.

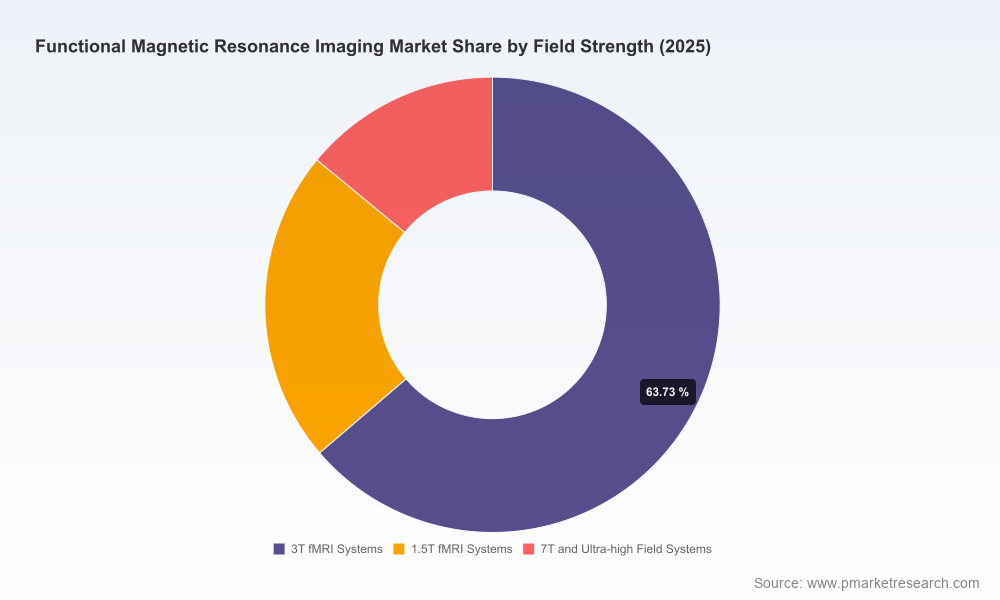

Technology and product roadmaps: Comparative analysis of field-strength trajectories, ultra‑high field adoption scenarios, and AI‑enabled reconstruction impacts on throughput and clinical sensitivity.

Vendor scorecards and competitive playbooks: Qualitative and quantitative benchmarking across product performance, service network, software ecosystems, regulatory posture, and commercial terms.

Procurement toolkits: TCO templates, contract negotiation checklists, and RFP language tailored to fMRI capabilities and multi-site harmonization needs.

Clinical adoption playbooks: Validation frameworks, study-design templates for local outcomes assessment, training programs for technologists and radiologists, and protocols for integrating fMRI into surgical planning pathways.

Risk and contingency planning: Helium supply mitigation strategies, spare‑parts mapping, and recommendations for staged fleet upgrades to minimize disruption.

Go‑to‑market and investment guidance: Market entry frameworks for new entrants, partnership matrices for OEMs and solution providers, and investment case models for private equity and corporate development teams.

The market is anchored by a mix of multinational OEMs and specialized suppliers. Understanding each player’s product focus, recent regulatory wins and ecosystem strategy is essential to making defensible 2026 decisions.

Siemens Healthineers (Erlangen, Germany; https://www.siemens-healthineers.com): A traditional MRI leader, Siemens’ MAGNETOM family spans mainstream to advanced platforms and emphasizes neuroimaging workflows for clinical and research use. Recent regulatory advances for low‑helium platforms reduce operating risk and make Siemens a strategic option for health systems prioritizing long-term reliability and integrated clinical applications.

GE HealthCare (Chicago, USA; https://www.gehealthcare.com): GE continues to push high-field innovation and integrated AI workflows. Recent 510(k) clearances for next-generation SIGNA platforms and an AI workflow suite signal an aggressive strategy to combine hardware upgrades with workflow monetization—an important consideration for centers targeting higher-throughput fMRI programs.

Philips Healthcare (Amsterdam, Netherlands; https://www.philips.com/healthcare): Philips’ focus on AI reconstruction and accelerated imaging (SmartSpeed and related tools) positions them as a strong partner for institutions that prize throughput and automated, reproducible pipelines for clinical neuroimaging.

Canon Medical Systems (Otawara, Japan; https://global.medical.canon): Canon’s Vantage platforms and integrated visualization toolsets offer a differentiated proposition for pre-surgical planning and BOLD‑based workflows. Their emphasis on clinical visualization and workflow integration is attractive to surgical centers and tertiary hospitals.

United Imaging Healthcare (Shanghai, China; https://www.united-imaging.com): With a portfolio that stretches from mainstream to higher-field systems and a growing software/services stack, United Imaging offers competitive technical performance and compelling commercial models—particularly in regions where pricing and local service depth are critical.

NordicNeuroLab (Bergen, Norway; https://www.nordicneurolab.com): As a specialist in fMRI stimulus hardware and integrated software suites, NordicNeuroLab is the go-to vendor for standardized stimulus presentation and plug‑and‑play workflows—an essential niche for multi-center studies and harmonized clinical protocols.

FDA clearances for low‑helium and helium‑free platforms in 2025–2026 materially reduce one axis of operational risk. Buyers evaluating fleet investments should now include low‑helium options as a strategic alternative to legacy magnet architectures.

Helium spot-price spikes and intermittent supply disruption in early 2026 increased service costs for conventional superconducting systems. Procurement teams must stress-test vendor service contracts and consider hybrid strategies that pair legacy systems with newer low‑helium units to smooth capital requirements.

510(k) pathways remain the primary regulatory route for fMRI-capable platforms. Manufacturers accelerating software-validated clinical claims will have a pathway to expand clinical indications—but buyers should require documented performance claims and peer-reviewed validation studies prior to enterprise-wide deployment.

Re-run capital planning scenarios incorporating helium risk, software subscription costs and multi-year service commitments—shift procurement criteria from lowest initial price toward lowest total cost of ownership under contingency scenarios.

Demand vendor evidence of validated clinical workflows and interoperability for multi‑center studies; include third‑party software and stimulus compatibility in RFPs.

Pursue partnerships with specialist suppliers for stimulus/response toolchains and external centers of excellence to accelerate clinical validation and build referral pipelines.

For investors and M&A teams: prioritize targets with defensible software IP, recurring revenue models, and service-network advantages that can be scaled across the concentrated vendor landscape.

PW Consulting’s Worldwide fMRI Market report combines macro forecasting, scenario modelling, vendor benchmarking, and plug‑and‑play procurement tools to help organizations convert market insight into executable plans for 2026 and beyond. The executive briefing above highlights the major strategic inflection points; the full report contains the granular segmentation, vendor-level scorecards, and downloadable procurement templates that operational teams rely on. Visit the report page to obtain the complete dataset, interactive models and proprietary vendor evaluations that underpin these recommendations.

For detailed analysis of this topic, please visit the official page:Worldwide Functional Magnetic Resonance Imaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com