Transparent Caching Market Growth Across North America's Digital Infrastructure

Other |

2026-06-10 12:36:36

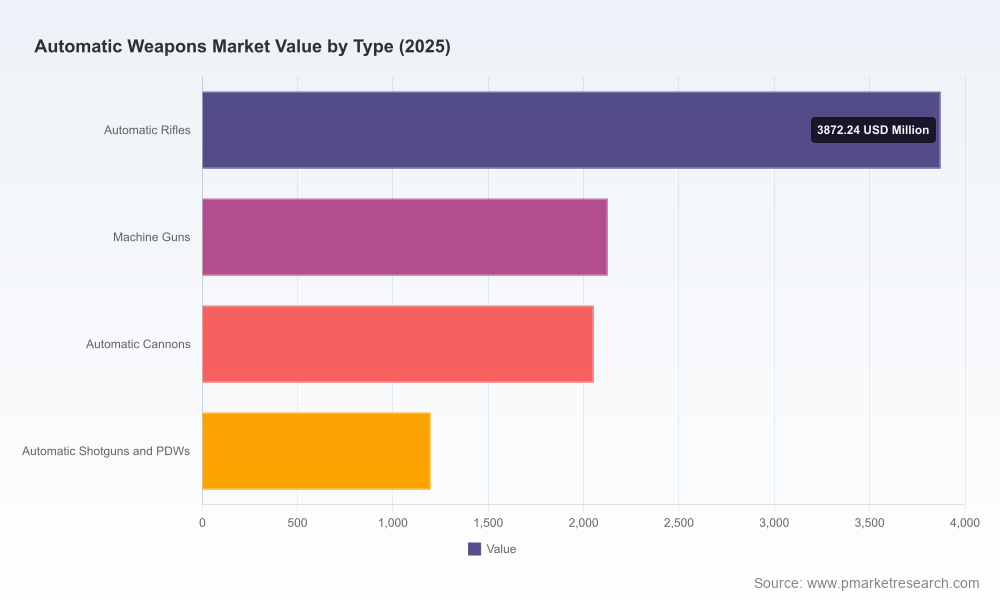

PW Consulting’s latest market intelligence — the Worldwide Automatic Weapons Market report (base year 2025; historical analysis 2020–2025; forecast period 2026–2032) — reframes how defence planners, prime contractors, suppliers and investors should approach procurement, industrial positioning and portfolio construction in 2026. Our model shows the market continuing on an above‑trend trajectory (compound annual growth rate of 7.0% across the forecast window), with the global market base reaching approximately USD 9.25 billion in 2025 and moving toward a near‑USD 10.0 billion volume in 2026 under the baseline scenario. These headline metrics signal expansion, but the operational implications for program timing, supply‑chain resilience and regulatory compliance require granular, actionable intelligence — which this report delivers, while retaining the core segmentation datasets as premium content to drive decision follow‑up.

Worldwide Automatic Weapons Market

Program cadence and procurement windows are compressing. Multiple NATO and allied modernization programs — including next‑generation squad‑level initiatives — are transitioning from trials and evaluation to production and fielding. That shift turns a multi‑year R&D cycle into near‑term production and sustainment demand.

Worldwide Automatic Weapons Market

Regulatory regimes have been recalibrated. Updates to multilateral control lists and national export controls in late 2025–early 2026 have altered licensing friction for critical components and certain dual‑use technologies, complicating cross‑border industrial cooperation and aftermarket supply strategies.

Worldwide Automatic Weapons Market

Input‑cost volatility and materials overcapacity are shaping margins. Steel benchmark behaviour in 2025 and limited recovery into 2026 are forcing procurement and manufacturing teams to re‑think price pass‑through, hedging and design choices that influence unit economics over a life‑of‑program horizon.

Growth with style: The market’s mid‑single‑digit to high‑single‑digit CAGR through 2032 masks heterogeneity — pockets of rapid innovation and procurement alongside mature sustainment spend. Our scenario suite identifies where growth will be driven by new‑build vs. aftermarket demand.

Moderate concentration, meaningful room for challengers: Competitive concentration metrics show a market neither atomised nor monopolised — the top three and top five firms together represent a majority share fraction that enables both scale advantages for incumbents and selective entry opportunities for focused specialists and regional champions.

Regulation and supply risk are first‑order constraints: Export control updates and materials pricing are not background noise — they directly change sourcing strategies, lead times and contract structures. Organisations that treat these as strategic levers rather than compliance checkboxes will gain decisive cost and schedule advantages.

Integrated financial model (Excel): A transparent, auditable model covering 2020–2025 history and 2026–2032 forecasts with configurable scenario switches (demand shocks, policy tightening, steel price stress tests). The full model includes line‑item forecasts by region, platform type and end‑user but those detailed tables are reserved for subscribers.

Scenario playbooks: Three enterprise scenarios (baseline, accelerated modernization, regulatory squeeze) with tactical decision trees for procurement timing, inventory buffers and subcontractor selection.

Supplier and technology scorecards: Objective scoring across capability, compliance posture, industrial footprint, and aftermarket potential — intended for OEM sourcing teams and M&A diligence.

Risk heatmaps and mitigations: Supply‑chain, regulatory and commodity risk matrices with prioritized mitigation roadmaps (including short‑term contractual clauses and medium‑term regional diversification strategies).

Commercial playbooks: Tender strategy templates, offset management frameworks and sustainment contracting options tailored for land, naval and air integrators.

M&A and partnership screeners: A curated list of mid‑market targets and partnership archetypes aligned to each scenario, with valuation sensitivity ranges and integration red flags.

We profile the full spectrum of incumbent and challenger firms active in automatic weapons systems, with in‑depth corporate profiles and strategic implications for each. Key manufacturers evaluated include European, North American, Israeli, Russian and Asia‑Pacific OEMs — each offering different mixes of platform heritage, export footprints and aftermarket capabilities. Recent industry developments underscore the strategic tempo:

Product innovation continues to shift procurement preferences. A January 2026 next‑generation launch by a major European manufacturer signalled further platform modularity, suppressor compatibility and mission‑tailored accessories. That release is already influencing RFP requirements and spare‑parts expectations.

Program certification milestones have de‑risked supply pipelines. A major Type Classification decision in mid‑2025 for a next‑generation squad weapon system unlocked full production and fielding paths for multiple suppliers, accelerating transition from prototype to series production for prime contractors and key subsystem suppliers.

What this means strategically: primes benefit from scale and platform commonality, but modularity and subsystem specialisation create entry vectors for technology providers and regional manufacturers to capture aftermarket, retrofit and training revenue. Governments and large integrators should therefore rethink supplier segmentation to prioritise capability clusters rather than single‑source incumbency.

Materials strategy: Persistent steel market pressure in 2025–26 imposes margin compression unless manufacturing and sourcing teams adopt substitution, yield improvements or fixed‑price hedging. The report quantifies the P&L sensitivity of common design choices to steel cost fluctuations.

Regulatory overlay: Changes to multilateral control lists and national export regimes add a temporal premium to cross‑border transfers and technology co‑development. We provide a compliance‑first integration checklist that aligns program delivery timelines to expected licensing lead times.

Sustainment as a strategic lever: As fleets expand, aftermarket, spare parts and training become predictable annuity streams. Our aftermarket models show where investment in depot capability and predictive maintenance tools delivers the highest ROI.

For primes: Rebalance bid strategies toward lifecycle value rather than lowest‑cost manufacturing. Emphasise modular architectures and open‑systems interfaces to secure long‑term aftermarket revenue.

For component suppliers: Focus on differentiators that reduce platform total cost of ownership — e.g., suppressor integration, lightweight modular mounting solutions and hardened sensor interfaces that remain compliant under tightened export lists.

For investors and M&A teams: Target bolt‑on assets with aftermarket service capability or niche high‑margin subsystems. Moderate market concentration means well‑timed acquisitions can create meaningful scale effects without requiring blockbuster multiples.

For procurement and defence policymakers: Incorporate licensing and commodity stress scenarios into multi‑year budget cycles, and prioritise industrial policies that preserve critical domestic manufacturing while enabling allied interoperability.

Consider this publication a strategic operating manual for the next procurement cycle. Practical uses include: feeding the scenario model into capital planning and inventory policy; running supplier scorecards during tender evaluation; using the risk heatmap to set contractual clauses and insurance provisions; and referencing company‑level intelligence during pre‑merger due diligence.

To preserve the report’s role as both a decision catalyst and a sales tool, PW Consulting intentionally keeps the detailed segmentation tables and the full, downloadable financial model behind our subscriber portal. Those datasets contain the granular regional, platform and end‑user breakdowns — the exact figures that procurement teams and corporate development units require to execute tactical plans in 2026.

Clients who require the full segmentation matrices, the live Excel model, confidential executive briefings, or bespoke scenario workshops should contact PW Consulting to request access. We offer tailored briefings that map the report’s findings directly onto client portfolios and procurement calendars, and we run rapid‑response workshops to update scenarios as new policy and program information is published.

PW Consulting’s Worldwide Automatic Weapons Market report is designed to convert headline growth and concentration signals into executable plans — without leaving programme managers to infer the regulatory, materials and competitive constraints that decide win/loss outcomes. In an environment where program windows are tightening and policy settings are shifting, that clarity is the difference between reactive procurement and proactive advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Automatic Weapons Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com