North America Water Quality Monitoring Systems Market to Benefit from Rising Water Safety Initiatives

Other |

2026-06-05 09:51:44

PW Consulting’s latest market study—Worldwide Elemental Fluorine Market (Base Year 2025; Forecast 2026–2032)—lays out a pragmatic, risk-focused roadmap for corporate decision-makers preparing plans and capital allocations in 2026. The market for elemental fluorine (F2) is entering a phase of steady expansion, driven by electronics, nuclear fuel cycle activity, specialty fluorochemicals and evolving energy-materials applications. Our analysis synthesizes historical performance (2020–2025), a quantitative forecasting framework and qualitative supplier intelligence into a set of actionable recommendations tailored to manufacturers, specialty gas users, raw-material traders and strategic buyers.

Worldwide Elemental Fluorine Market

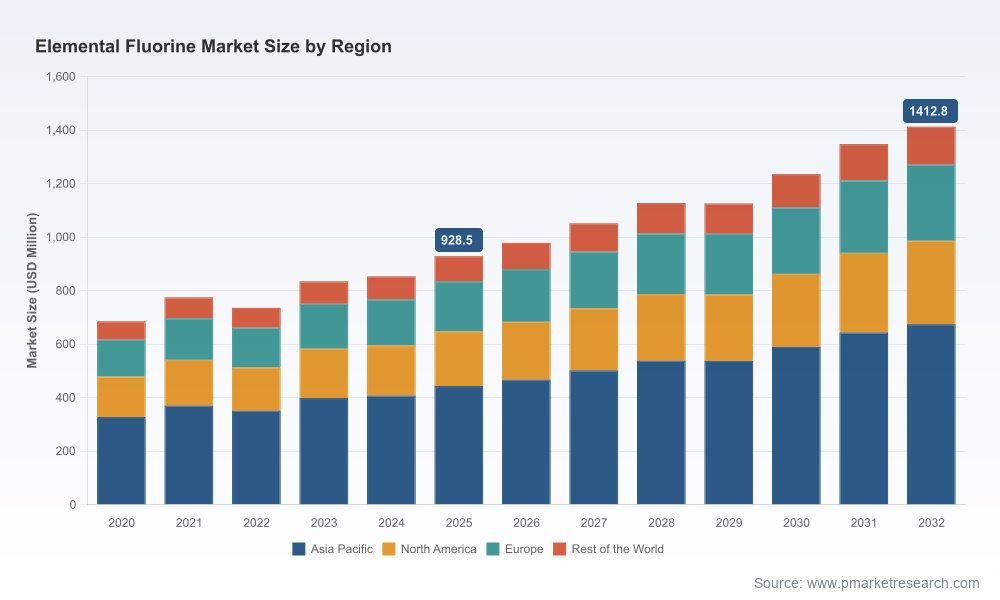

PW Consulting’s central projection shows an industrial market expanding at a compound annual growth rate (CAGR) of approximately 6.18% through the 2026–2032 forecast window. Using 2025 as the base year, the market value on our revenue metric stood at just under USD 930 million (Million USD units), with our modelling indicating a rise toward the low‑to‑mid USD 1.4 billion range by 2032 under the reference scenario. The growth trajectory is neither hypercyclical nor static—rather it reflects a market with solid underlying demand and meaningful supply-side constraints that create both commercial risk and strategic opportunity.

Worldwide Elemental Fluorine Market

Concentration is material: the top three producers control roughly two-thirds of the market, and the top five account for close to four-fifths. This supplier concentration amplifies the commercial impact of plant outages, regulatory actions and raw-material price volatility—factors we observed repeatedly in the 2020–2025 period and which inform our 2026 guidance.

Worldwide Elemental Fluorine Market

Procurement stability becomes a competitive differentiator. With concentrated supply and complex handling/transport regulations (elemental fluorine is classified under UN 1045 as a toxic gas with specialized transport requirements), procurement teams must plan beyond spot buys and short-term contracts.

Price and feedstock exposure are real. Upstream raw-material pressures—most notably fluorspar and anhydrous hydrogen fluoride (HF)—have raised feedstock cost baselines. Recent commodity moves have materially tightened producer margins and passed costs through the supply chain, signaling higher baseline operating costs for 2026 unless firms hedge or re-engineer inputs.

Regulatory and logistical frictions will affect on-the-ground availability. EU REACH authorization processes and stringent transport rules complicate rapid redeployment of supply; companies that proactively align compliance and transport strategies will reduce downtime risk.

Feedstock and raw-material risk: Acid-grade fluorspar and HF markets tightened materially in the last two years, with upward price pressure reflected in producer cost structures. Buyers should expect continued sensitivity to global fluorspar supply dynamics—and the company-level consequences of any further raw‑material shocks.

Geopolitical and regional concentration: China’s dominant role in global fluorspar production has downstream implications for HF and F2 availability when export quotas, trade policy or logistics are adjusted. Clients that rely on single-region sourcing must build contingency plans for 2026 and beyond.

Regulatory overlay: Elemental fluorine’s classification and REACH oversight impose non-trivial compliance demands on manufacturers and users. Exporters, transporters and end-users must maintain certification, documentation and specialized handling capabilities—areas that often prolong lead times for new supply relationships.

Operational fragility: Historical incidents—such as force majeure declarations following facility incidents and planned restarts after maintenance—underscore the operational concentration embedded in the supply chain. The cadence of maintenance, the timing of plant turnarounds, and the scarcity of spare capacity combine to make proactive supply planning essential in 2026.

PW Consulting’s competitive analysis profiles the largest, dedicated and strategically positioned producers. These profiles are synthesized from primary interviews, company disclosures and on-the-ground verification—designed to help buyers and investors assess counterparty risk, partnership potential and M&A targets.

Air Products and Chemicals, Inc. (Lehigh Valley, PA) — A global leader in ultra-high-purity F2 supply to the semiconductor sector and specialty chemical markets. Strengths: broad global service footprint, long-term supply contracts with electronics manufacturers, advanced purity control capabilities. Strategic implication: preferred partner for high-reliability electronics customers; prime target for supply continuity arrangements and co-location strategies with chip fabs.

Solvay SA (Brussels) — Integrated producer using electrolysis platforms serving fluorochemicals and nuclear applications. Strengths: vertical integration into HF and intermediates, global customer channels. Risks: past incidents (notably a 2022 force majeure at an HF site) demonstrate the downstream vulnerability that can ripple across industrial F2 markets. Strategic implication: counterparty diligence and contingency clauses are essential when engaging with producers that operate complex multi‑product platforms.

Pelchem SOC Ltd (Pelindaba, South Africa) — One of the world’s largest dedicated F2 producers with a strong footprint in enrichment and specialty markets. Strengths: dedicated capacity for elemental fluorine and experience servicing nuclear clients. Recent restart events demonstrate both maintenance discipline and the potential for short windows of constrained supply. Strategic implication: ideal for high‑purity legacy supply needs, but buyers should structure multi-tier sourcing to buffer restart risk.

Kanto Denka Kogyo Co., Ltd. (Tokyo) — Specialist in high‑purity F2 for electronics and solar applications. Strengths: focus on electronics-grade gases and advanced materials fluorination processes. Strategic implication: technology- and quality-driven customers will find strategic alignment in partnerships around new node development and speciality gas formulations.

Stella Chemifa Corporation (Osaka) — Supplies F2 and fluorine compounds for semiconductor cleaning, battery materials and pharma intermediates. Strengths: product breadth linked to battery and pharmaceutical chains; agility in developing tailored gas solutions. Strategic implication: suitable for firms seeking co-development of novel fluorine chemistry for emerging battery chemistries or pharma intermediates.

The report is designed as a working tool for 2026 strategy teams. Key deliverables include:

Scenario-based demand forecasts and a transparent pricing model calibrated to spot and contract HF/fluorspar dynamics—enabling finance and procurement to stress-test budgets under alternative commodity scenarios.

Supplier scorecards and an outage‑risk heatmap that combine technical capability, geographic exposure and compliance posture to rank counterparties for sourcing strategies and strategic partnerships.

Supply-chain topology maps and node-level vulnerability analysis—showing where single-point failures matter most for particular applications (e.g., semiconductor etch gases versus uranium enrichment feedstocks).

Contract playbooks and negotiation levers—templates for term sheets, escalation clauses, inventory consignment models and joint‑capex options that materially reduce supply interruption risk.

Regulatory and transport compliance checklist—covering UN 1045 handling, DOT/EU ADR transport constraints and REACH authorization considerations, plus pragmatic remediation steps for 2026 readiness.

M&A and partnership screening toolkit—weighted scoring to prioritize targets and JV partners where capacity, technology or geographic footprint complement corporate strategy.

Elevate supplier risk management to board-level attention. Given market concentration and the regulatory/logistical overlay, supply-risk should be tied directly to capital and continuity planning in 2026.

Adopt a layered sourcing model. Combine strategic long-term contracts with secured volume from concentrated, creditworthy producers and shorter-term agile supply to cover maintenance windows and demand spikes.

Hedge or vertically integrate upstream exposure where feasible. For large consumers, selective investment or offtake in HF / fluorspar supply reduces cost volatility and creates lasting commercial advantage.

Invest in compliance and specialized logistics. Ensuring that in‑house or third-party logistics are certified for UN 1045 handling reduces transport delay risk and insulates operations from regulatory friction.

Use procurement playbooks to convert risk into value. Include indemnities tied to force majeure events, defined turnaround notice periods, and tiered pricing tied to raw-material indices.

Consider strategic partnerships with technology-focused producers for co-development of lower‑risk F2 substitutes or alternative fluorination chemistries—particularly relevant to battery and semiconductor customers seeking supply diversification.

PW Consulting’s Worldwide Elemental Fluorine Market report is structured to move stakeholders from diagnosis to decision. The full study includes the underlying datasets, supplier scorecards, contract templates and scenario models referenced above. For companies preparing 2026 budgets, procurement strategies or M&A roadmaps, the report supplies the calibrated intelligence required to convert fluorine-market uncertainty into competitive advantage.

Contact PW Consulting to access the full dataset and operational annexes that contain the granular segmentation, pricing curves and supplier-level data omitted from this executive primer.

For detailed analysis of this topic, please visit the official page:Worldwide Elemental Fluorine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com