Worldwide Antibody Fragments Market: Strategic Intelligence for 2026 Decision-Making

PW Consulting’s latest market study on the Worldwide Antibody Fragments Market delivers an actionable intelligence package designed to arm executives, R&D leaders, manufacturing chiefs, and corporate strategy teams with the context and operational playbook they need for 2026. The report synthesizes financial trajectories, technology inflection points, competitive positioning, and pragmatic go-to-market scenarios—showing where to commit capital, where to partner, and where to de-risk—while deliberately preserving proprietary segment-level data for subscribers.

Worldwide Antibody Fragments Market

Market snapshot: scale, trajectory, and what it means for 2026

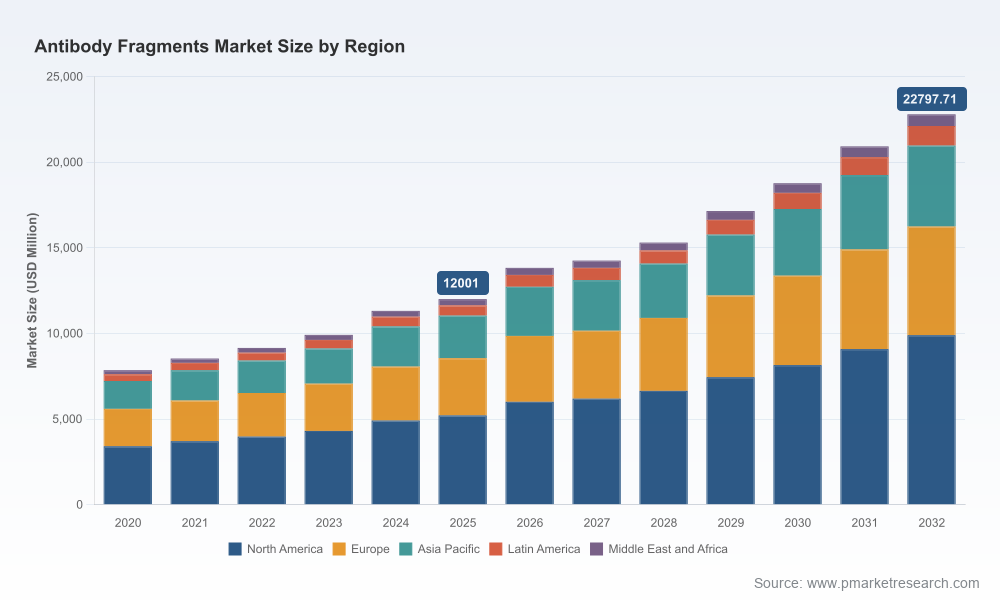

Our analysis finds the antibody fragments market reached approximately USD 12,001 million in 2025 and is forecast to grow to about USD 13,829 million in 2026. Under the base-case scenario, the market is projected to expand at a compound annual growth rate (CAGR) of 9.6% across the 2026–2032 forecast window, reaching roughly USD 22,798 million by 2032. This pace of growth underscores both the maturation of fragment-based modalities (Fab, scFv, single-domain formats) and an expanding set of clinical and non-clinical use-cases—creating an environment in which strategic timing, manufacturing design, and regulatory foresight materially affect ROI.

Worldwide Antibody Fragments Market

Why this report matters for 2026 corporate plays

- Investment prioritization: With double-digit growth outlook, executives must select between building in-house capabilities for novel fragment formats or purchasing access through M&A and partnerships. The report provides scenario-based financial modeling to quantify break-even horizons for both build and buy options.

- Manufacturing and COGS optimization: Antibody fragments present distinct downstream processing challenges and half-life engineering trade-offs. Our analysis translates those technical constraints into cost curves and capacity-planning heuristics intended for capital budgeting cycles in 2026.

- Regulatory and commercialization sequencing: Fragment therapeutics, diagnostics, and research reagents follow biologics-like regulatory pathways. The report maps risk-adjusted timelines and outlines the data packages that demonstrably accelerate approval and reimbursement conversations.

- Partnering and alliance strategy: We surface win-sets for asset-centric biotechs and platform providers so pharma companies can design early-stage partnerships that plug capability gaps without overpaying for non-core competencies.

Report contents: practical modules for immediate action

Rather than an academic catalog, this study is structured as a toolkit for 2026 decision-makers. Key modules include:

Worldwide Antibody Fragments Market

- Top-line market forecast and sensitivity testing under three macroeconomic scenarios (base, upside, downside).

- Technology assessment: trade-offs between Fab, scFv, and single-domain formats with a focus on tissue penetration, half-life engineering, and manufacturability.

- Manufacturing playbook: recommended expression platforms, downstream purification architectures, scale-up constraints, and capital-cost modeling.

- Go-to-market playbooks by use-case (therapeutics, diagnostics, R&D reagents) including commercialization cost models and payer-engagement checklists.

- Partner-screening framework and due diligence templates to evaluate CDMOs, platform licensors, and discovery partners.

- Deal comparables and M&A archetypes to inform valuations and structuring for 2026 transactions.

Competitive landscape: established titans and specialized innovators

The antibody fragments space is shaped by large, diversified biopharma companies that leverage franchise power and deep regulatory expertise, alongside nimble specialist firms offering platform technologies and contract production services. Leaders in large-cap pharma bring clinical development scale and commercial channels—critical for late-stage therapeutics—while platform players and CDMOs accelerate early-stage progress and reduce technical risk.

- Large pharmaceutical incumbents such as F. Hoffmann‑La Roche AG, Novartis AG, AbbVie Inc., Amgen Inc., Pfizer Inc., Johnson & Johnson (Janssen), Bristol‑Myers Squibb, Eli Lilly and Company, and UCB continue to anchor the market with late‑stage assets and established commercialization capabilities. Their strategic plays tend to focus on high-value indications where reimbursement dynamics justify premium pricing and complex lifecycle management.

- Sanofi, notably through Ablynx’s NANOBODY® platform, demonstrates how a focused single-domain technology can be translated into differentiated products with operational advantages in tissue penetration and manufacturing. Platform commercialization and internal promotion of these capabilities remain a key lever for market leadership.

- Specialist providers and service-platforms—such as Sino Biological and evitria—are increasingly critical partners for companies that want to accelerate discovery and scale production without incurring full in‑house CAPEX. Their role in custom expression and stabilization of complex fragment formats creates flexible options for program teams and corporate development pipelines.

Recent industry developments you can’t ignore

- Platform advancements: Continued R&D investment and public promotion of single-domain platforms signal a strategic focus on modalities that combine manufacturability benefits with improved tissue distribution—an important consideration for oncology and ophthalmology programs.

- Partnership momentum: Expanded collaboration activity across discovery platform owners and biopharma sponsors has compressed time-to-clinic for novel fragment formats. Our report quantifies typical milestone structures and common risk-sharing arrangements observed in recent deals.

- Industrialization trends: Reviews of nanobody development and industrialization show increasing patent activity, trial volumes, and standardization efforts—key inputs when assessing freedom-to-operate and platform scalability.

Operational realities: manufacturing, expression systems, and half-life engineering

Antibody fragments diverge from full monoclonal antibodies in several operationally material ways:

- Downstream complexity: Fragments lacking Fc domains cannot rely on Protein A affinity capture, forcing multi-step purification flows (ion exchange, hydrophobic interaction chromatography and others). This typically raises downstream processing complexity and cost relative to intact IgG workflows—an important driver of COGS and capital allocation decisions.

- Expression system choice: Microbial platforms (e.g., E. coli, Pichia) can yield cost-effective production routes for scFv and nanobodies, with optimized processes delivering competitive titers. Mammalian systems remain necessary for certain glycosylated or complex formats, but the economics and yield differentials make platform selection a pivotal early decision.

- Half-life and delivery trade-offs: Engineering solutions—PEGylation, albumin-binding tags, Fc fusions—extend systemic exposure but materially increase manufacturing complexity and COGS. Teams must model therapeutic value by indication to determine whether half-life augmentation strategies are value accretive.

Regulatory, reimbursement and payer context

Antibody fragments follow biologics-like regulatory pathways and require rigorous preclinical, clinical, and post-market evidence. From a reimbursement standpoint, stakeholders should anticipate heightened scrutiny on cost-effectiveness for indications with large patient populations. The additional manufacturing costs associated with half-life extension strategies can compress margins in price-sensitive segments; our report offers payer-engagement templates and value dossier outlines tailored to fragment therapeutics.

Strategic playbook for 2026

- Portfolio prioritization: Use the report’s risk-adjusted valuation templates to rank candidates by indication, manufacturing complexity, and expected reimbursement outcomes.

- Manufacturing footprint design: Apply the facility sizing and COGS models to choose between microbial and mammalian routes and to decide the optimal split between in-house capacity and CDMO partnerships.

- Partnership & licensing strategy: Target platform partnerships that deliver clear reductions in technical risk and time-to-clinic. The report includes a checklist for structuring milestone and royalty terms that align incentives.

- M&A and bolt-on criteria: For companies seeking inorganic growth, the study offers acquisition archetypes and integration playbooks tuned to fragment-platform economics.

- Regulatory & payer sequencing: Deploy accelerated development pathways where scientific rationale and unmet need converge; prepare payer dossiers early for high-volume indications where reimbursement will be decisive.

Conclusion: why PW Consulting’s study is essential for 2026

As antibody fragments evolve from niche modalities to mainstream tools in therapeutics, diagnostics, and research reagents, 2026 will be a pivotal year for firms that must choose between rapid scaling, platform consolidation, and focused clinical risk-taking. PW Consulting’s Worldwide Antibody Fragments Market report provides the strategic frameworks, operational models, and competitive intelligence necessary to make those choices with confidence. We present deep, actionable insight—while preserving the granular segmentation and model outputs for subscribers to ensure decisive commercial advantage.

To access the full suite of models, regional and application breakdowns, and proprietary segmentation data supporting our recommendations, visit the official report page or contact PW Consulting’s commercial team for subscription details.

For detailed analysis of this topic, please visit the official page:Worldwide Antibody Fragments Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com