Privacy Filters Market Dynamics: Key Indicators, Drivers, and Future Trends

Art |

2026-05-29 08:18:23

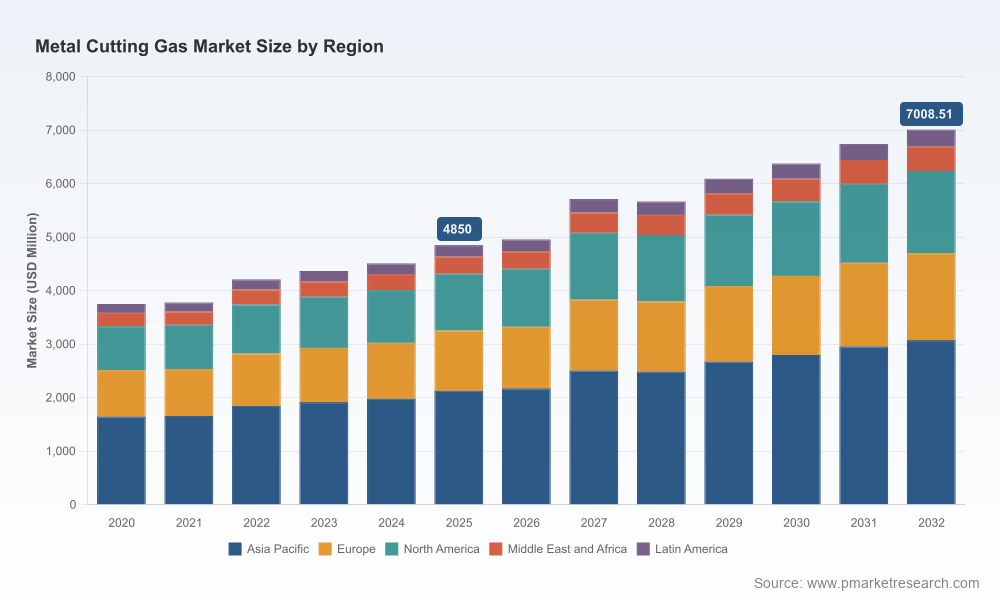

As global industrial value chains recalibrate after a period of uneven recovery, the metal cutting gas market has reached an inflection point. PW Consulting’s latest market research—anchored on a 2025 base year and projecting through 2032—shows the sector expanding at a compound annual growth rate (CAGR) of 5.4%. The global market value was approximately USD 4,850 Million in 2025 and is projected to approach USD 7.01 billion by 2032. For executives planning capital allocation, procurement, or go-to-market moves in 2026, this research is designed to translate macro trajectories into actionable commercial playbooks.

Worldwide Metal Cutting Gas Market

Timing: 2026 is a decision year. Policy shifts on trade and emissions, evolving upstream feedstock prices, and accelerating automation in metal fabrication mean near-term actions will determine who captures the next wave of margin improvement.

Worldwide Metal Cutting Gas Market

Market momentum: A steady mid-single-digit CAGR through 2032 presents both growth and disruption opportunities. Suppliers who align pricing, logistics and product innovation with end-user productivity gains will outperform.

Worldwide Metal Cutting Gas Market

Competitive structure: The market displays moderate concentration — the top three and five suppliers represent a material share of global supply — creating both barriers and openings for regional players and specialist entrants with differentiated value propositions.

Feedstock and pricing volatility: Acetylene feedstock and LPG-derived cutting gas prices remain a primary margin and sourcing risk. Recent market reads show regional divergence in acetylene sourcing costs, underscoring the need for dynamic procurement strategies that combine hedging, local sourcing, and blending flexibility.

Regulatory and logistics pressure: Regulatory developments in major markets are affecting both demand-side compliance and supply-chain costs. For example, tightened emissions rules for integrated metal production facilities and ongoing transport safety standards for compressed gases necessitate proactive compliance and logistics investments.

Trade policy and cost pass-through: Changes to trade measures on steel and aluminum inputs have a second-order impact on fabrication economics and, by extension, cutting gas demand. Manufacturers and suppliers must stress-test pricing models under tariff and landed-cost scenarios.

Technology and process substitution: Laser and plasma cutting adoption, fuel-blend optimization, and digital process controls are steadily changing per-cut economics. The companies that can demonstrate per-piece productivity gains, lower total cost of ownership, and stronger safety metrics will win commercial preference.

Top-down market sizing and transparent methodology: A full explanation of data sources, assumptions and reconciliation between supply-side and consumption-side estimates for 2020–2025 and baseline projections for 2026–2032.

Demand-driver decomposition: Detailed examination of macro drivers (construction, automotive, shipbuilding, heavy machinery, aerospace/defense) with scenario-based demand sensitivity to GDP, trade policy, and capital investment cycles.

Cost and price benchmarking: End-to-end cost stacks including feedstock, processing, cylinder and bulk logistics, blending, and regulatory compliance costs—plus regional price comparisons and scenario modelling for raw-material swings.

Regulatory impact assessment: Practical guidance on the implications of emissions standards and hazardous materials transport rules for facility retrofit, permitting lead times, and cross-border movements of compressed gases.

Competitive landscape and capability matrices: Strategic profiles of global and regional suppliers with a focus on distribution footprint, product breadth (standard gases, LPG-based variants, specialty blends), equipment integration, and service capabilities.

Commercial playbooks: Procurement levers, supplier segmentation strategies (core vs. contingency), pricing playbooks, and contracting templates designed to be actioned in 90–180 days.

Investment and M&A framework: Value-creation roadmaps for bolt-on acquisitions, greenfield blending and bottling capacity, and digitization investments with expected payback ranges under multiple demand scenarios.

Operational toolkits: KPIs and dashboards for cut-cost per unit, cylinder turn metrics, safety incidence tracking, emissions per ton of output, and recommended contract clauses for logistics and force majeure.

Global integrated suppliers (e.g., Linde plc, Air Liquide, Air Products): These incumbents leverage scale in feedstock procurement, hydrogen and oxygen portfolios, and global cylinder and bulk logistics to offer bundled solutions to large OEMs and fabricators. Their strategic advantages include cross-border supply networks, R&D capabilities in specialty blends, and the ability to pilot integrated service models combining gas supply with cutting equipment and digital monitoring.

Regional and national champions (e.g., Messer, TotalEnergies, major national oil companies and LPG suppliers): These players compete on regional logistics excellence, cost-competitive LPG formulations, and close partnerships with local industry clusters. Their agility in tailoring blends and logistics to market-specific requirements is a critical differentiator.

Specialist and equipment-focused players (e.g., ESAB, equipment manufacturers, and technical gas specialists): These companies combine consumables and equipment to capture aftermarket revenue streams, prioritizing service, training, and productivity improvements that justify premium pricing.

Emerging and niche providers: Smaller suppliers and regional distributors deploy flexible blending, rapid response logistics, and aggressive pricing to capture accounts sensitive to supply continuity. Strategic partnerships or consolidation by larger groups are likely as incumbents seek to strengthen last-mile presence.

Hedge and hybrid sourcing: Combine long-term offtake contracts with flexible spot access and regional blending options to manage feedstock cost spikes while protecting margins.

Differentiate via outcomes, not commodity: Sell productivity improvements—lower cut-time, reduced rework, improved safety—rather than pure volume. Guaranteeing productivity gains enables value-based pricing.

Invest selectively in logistics and safety: Strengthen hazardous-material transport compliance and invest in leak-detection and tracking technology. These investments reduce disruption risk and shield customers from regulatory exposure.

Pursue targeted partnerships and bolt-ons: For suppliers seeking scale in adjacent regions, prioritize acquisitions that add critical last-mile distribution or specialized blending capability rather than generalized capacity.

Operationalize tariff and emissions scenarios: Build financial models that stress-test profit pools under a range of trade and regulatory outcomes; embed trigger points for tactical responses such as rerouting supply or accelerating product substitution.

For suppliers: Use the report’s pricing and cost-stack models to redesign commercial contracts—move to indexed pricing with productivity-linked clauses and layered supply commitments for strategic accounts.

For fabricators and OEMs: Deploy the procurement playbook to assess the total cost of supply, not just unit price—incorporating safety incidents, downtime and logistics reliability into supplier scorecards.

For investors and M&A advisors: Apply the valuation and value-creation templates to identify targets that offer immediate operational synergies or rare blends/equipment capabilities that close the service gap with leading clients.

For policy and compliance teams: Leverage the regulatory impact module to minimize permitting lag and to quantify the cost of compliance under tightening emissions and transport regulations.

Real-world KPIs: cylinder turn rates, cut-cost per meter, emissions intensity per tonne, safety incident rate per 10,000 hours, and logistics on-time delivery rates.

Scenario outputs: demand and pricing under base, upside, and downside cases with sensitivity to feedstock price swings and tariff shocks.

Supplier heatmaps: capability, reliability, and price-positioning across customer segments to inform shortlist and negotiation strategy.

In keeping with our “trailer” approach, this release emphasizes strategic conclusions and executable frameworks while withholding the granular segment-level tables, regional and application-specific revenue breakdowns, and the full set of supplier financial proxies. These detailed datasets—along with downloadable models and configurable scenario dashboards—are available in the full PW Consulting report and are essential for direct implementation of the recommendations outlined above.

Audit supply contracts for indexation and force majeure exposure; institute a secondary supplier qualification process.

Run a two-week cost-to-cut pilot on strategic accounts to quantify productivity improvement opportunities tied to alternative gas blends or process changes.

Map regulatory exposure for production and transport across your footprint and prioritize investments where permit lag or transport risk is highest.

Establish a cross-functional rapid response team to execute playbook steps if feedstock costs move beyond predefined thresholds.

PW Consulting’s Worldwide Metal Cutting Gas Market report is built to convert macro forecasts into boardroom-ready actions for 2026. For access to the full dataset, scenario models, and supplier playbooks that support deal execution and operational change, visit PW Consulting or contact our industry team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Metal Cutting Gas Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com