Worldwide Water Tube Industrial Boilers Market — Strategic Imperatives for 2026 Decision-Making

As companies reframe capital allocation and technology roadmaps in response to accelerating decarbonization mandates, supply-chain volatility, and evolving fuel economics, the industrial water tube boiler sector is entering a phase that rewards foresight and operational rigor. PW Consulting’s latest market study — anchored on a 2025 base year and projecting through 2032 — distills the commercial realities and strategic options that will determine winners and laggards in the 2026 planning cycle.

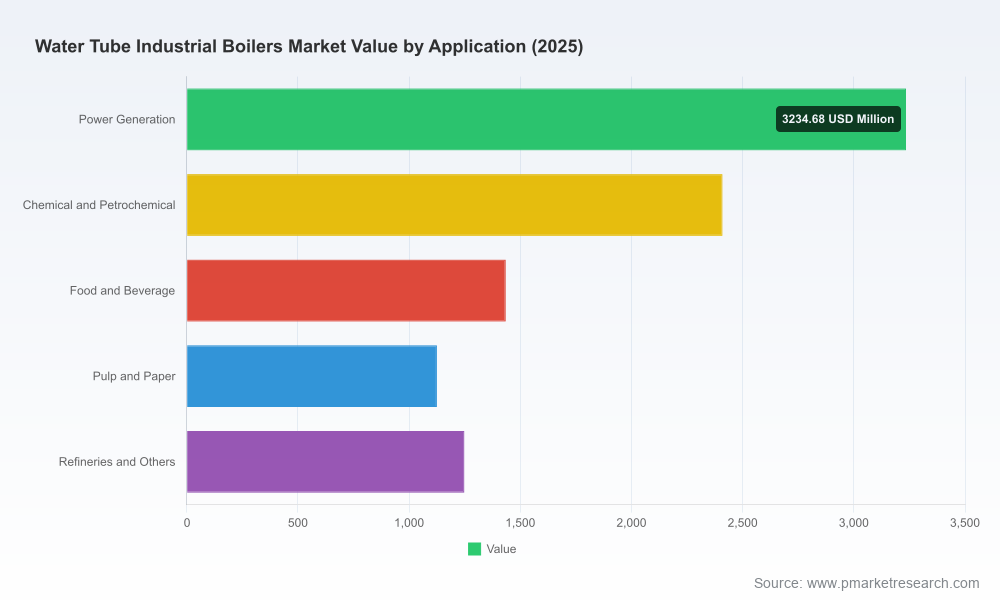

Worldwide Water Tube Industrial Boilers Market

Market trajectory at a glance

The market’s near-term momentum is underpinned by a steady recovery and structural demand for high-efficiency steam and process heat solutions. On a macro basis, PW Consulting’s model pegs the 2025 global market size at approximately USD 9,450.5 Million, expanding at a compound annual growth rate (CAGR) of 4.51% over the 2026–2032 forecast window. By 2032 the market is expected to surpass USD 12.8 billion (USD Million), reflecting a blend of replacement cycles, fuel-conversion projects, biomass and hybrid fuel uptake, and retrofit investments tied to air‑quality and CO2 mitigation requirements.

Worldwide Water Tube Industrial Boilers Market

Two structural features should guide 2026 choices: market consolidation that is meaningful but not prohibitive (the top three vendors account for roughly one-third of market value, while top five vendors approach half the market) and a persistent tug-of-war between incumbent fossil‑fuel designs and emerging low‑carbon technologies. These characteristics create both opportunity—through differentiated service, modularization, and fuel flexibility—and risk, for firms that under-invest in interoperability and emissions readiness.

Worldwide Water Tube Industrial Boilers Market

Why this report matters for 2026 decisions

Beyond headline forecasts, PW Consulting’s report is designed as an operational playbook for procurement officers, plant managers, corporate strategists, and investors making binding decisions in 2026. The study provides:

- Forward-looking total-cost-of‑ownership (TCO) models that capture CAPEX, fuel mix scenarios, maintenance regimes, emissions‑control retrofits, and financing alternatives;

- Scenario-driven sensitivity analysis (fuel price shocks, carbon pricing, disruption to steel supply) to stress-test investment returns across 3–10 year horizons;

- Technology-readiness assessments covering hydrogen‑capable burners, oxy‑combustion retrofits, biomass co‑firing, and modular plant deployment; and

- Commercial diligence tools: supplier scorecards, bid‑evaluation frameworks, and contracting templates tailored to industrial steam projects.

These elements translate the market projection into executable steps: where to allocate capex in 2026, which platforms to pilot for fuel‑conversion, and how to negotiate contracts that preserve future optionality.

Key dynamics shaping supplier and buyer strategy

- Decarbonization as a design constraint. Increasingly prescriptive policy and corporate net‑zero targets are moving low‑carbon capabilities from premium options to baseline requirements. The industry is seeing demonstrators of high‑capture oxy‑combustion and full hydrogen firing successfully commissioned, indicating that buyers who specify “hydrogen‑ready” or “oxy‑capable” designs will avoid early obsolescence.

- Fuel diversification and localized solutions. Adoption of biomass and alternative fuels is being driven by industrial consumers in energy‑intensive sectors seeking secure, lower‑emission heat. Grants and industrial decarbonization programs in several jurisdictions are accelerating retrofit and repowering projects.

- Input cost and supply‑chain pressures. Raw‑material dynamics are non‑trivial for boiler manufacturers: hot‑rolled coil prices have moved materially year‑over‑year, with recent spot adjustments observed in global and US markets. These cost dynamics feed into lead‑times and warranty conditions, and they require buyers to model supplier margin exposure and indexation mechanisms.

- Modularization and speed to steam. Demand for modular, factory‑assembled units continues to grow among buyers prioritizing schedule certainty and lower on‑site labor risk. Modular designs also support staged fuel transitions and can be deployed as temporary capacity while longer‑term decarbonization projects mature.

Competitive landscape — positioning and strategic moves

The market is served by an interplay of legacy engineering houses, specialized regional manufacturers, and agile modular players. PW Consulting’s competitor analysis synthesizes public disclosures, project wins, and product portfolios to map capability clusters and gaps.

- Babcock & Wilcox (Akron, Ohio, USA) — Longstanding in heavy industrial steam with a product range spanning custom and packaged water‑tube designs. Strengths: deep engineering credentials, broad aftermarket services, and project execution experience on complex industrial and power applications.

- Cleaver‑Brooks (Thomasville, Georgia, USA) — Focused on integrated boiler systems and packaged solutions that emphasize energy efficiency. Strengths: strong commercial product line for industrial steam and service networks that shorten downtime risk.

- Miura Boiler (Osaka, Japan) — Notable for modular, high‑efficiency designs with low NOx performance. Strengths: rapid startup units and compact footprints that suit facilities prioritizing operational flexibility.

- Indeck Power Equipment (Wheeling, Illinois, USA) — Large installed inventory and modular D‑type packages suitable for rapid supply. Strengths: speed to delivery and broad distribution capabilities for expedited projects.

- Thermax (Pune, India), ZOZEN (Wuxi, China), and regional specialists — Compete on cost and localized support; some are moving aggressively into biomass and hybrid fuel systems.

Recent industry moves validate strategic priorities: manufacturers and plant owners are publicly testing oxy‑combustion systems for CO2 capture and executing hydrogen conversion projects. These developments are early indicators that decarbonization solutions are migrating from lab to commercial scale — an immediate consideration for procurement specifications in 2026.

Supply‑chain and cost shocks — modeling implications

Material cost and availability should be explicitly modeled in procurement and scenario analyses. PW Consulting’s investigation confirms recent upward adjustments in hot‑rolled coil pricing in early 2026 relative to year‑ago levels, with comparable pressure in U.S. prices. For CFOs and procurement leads, this implies two practical mitigations for 2026:

- Include material indexation clauses and phased payments in supplier contracts to share price volatility risk; and

- Prefer modular and standardized platforms where possible to reduce bespoke steel content exposure and shorten lead times.

From insight to action: recommended 90‑day playbook for 2026

For companies preparing budgets and capital plans in 2026, PW Consulting recommends a focused, three‑step program to convert market insight into defensible decisions:

- Quarter 1 — Risk map and TCO baseline. Run the report’s TCO templates against your portfolio to identify plants with the highest sensitivity to fuel price and carbon costs. Prioritize facilities for piloting hydrogen‑ready burners or biomass conversions.

- Quarter 2 — Supplier short‑list and capability tests. Use the supplier scorecards to short‑list 2–3 vendors for competitive pilots. Structure contracts to include performance guarantees, retrofit pathways, and options for future fuel conversions.

- Quarter 3 — Capital optimization and financing. Evaluate blended financing (grants, green loans, EPC contractor financing) and phase investments to preserve optionality — start with modular additions that lower near‑term risk while reserving budget for larger decarbonization projects.

What the full PW Consulting report contains (and why you’ll need it)

To preserve the commercial value of our primary research while giving buyers a clear path forward, this briefing intentionally omits detailed segment and regional tables. The full report, however, includes:

- Comprehensive market sizing and validated vendor revenue benchmarking by product family (available in downloadable datasets);

- Proprietary supplier scorecards and capability matrices;

- Detailed scenario outputs for fuel, carbon, and material‑price sensitivities; and

- Implementation checklists, bid‑evaluation templates, and an actionable roadmap for decarbonization pilots.

These deliverables convert the headline CAGR and market trajectory into executable procurement and engineering decisions — the exact line items and proprietary splits are published in the full dataset and analyst decks available through our report portal.

Final strategic takeaways

- 2026 is a pivot year: buyers who embed emissions‑readiness and fuel flexibility in specifications will avoid costly late‑stage retrofits.

- Manage supply‑chain and material risk proactively through contract design and modular procurement to blunt steel and component price shocks.

- Prioritize pilots that deliver measurable CO2 reduction while maintaining operational reliability; use these pilots as learning platforms to scale across the asset base.

- Leverage competitive dynamics: the market shows room for differentiation via service, speed‑to‑steam, and low‑emission capability rather than purely on price.

PW Consulting’s Worldwide Water Tube Industrial Boilers Market report translates macro forecasts — including our 2025 base sizing and 4.51% CAGR to 2032 — into a practical, risk‑aware strategy for 2026. For suppliers seeking to sharpen product roadmaps and for buyers planning capital commitments, the full report provides the datasets, supplier benchmarking, and contractual templates needed to act with confidence. Visit our report portal to access the complete analysis, proprietary tables, and consultant support options that will convert these insights into competitive advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Water Tube Industrial Boilers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com