Worldwide Cold Formed Steel Frame Market: Strategic Imperatives for 2026 — PW Consulting Announces New Industry Brief

PW Consulting’s latest market study on the Worldwide Cold Formed Steel (CFS) Frame Market provides a timely, operationally focused roadmap for executives making strategic decisions in 2026. Drawing on five years of historical performance (2020–2025), with 2025 as the base year, and a forward-looking forecast to 2032, the report quantifies market size trajectories and stresses the commercial actions that will separate winners from laggards in the evolving steel framing ecosystem.

Worldwide Cold Formed Steel Frame Market

Executive snapshot: growth, scale and structure

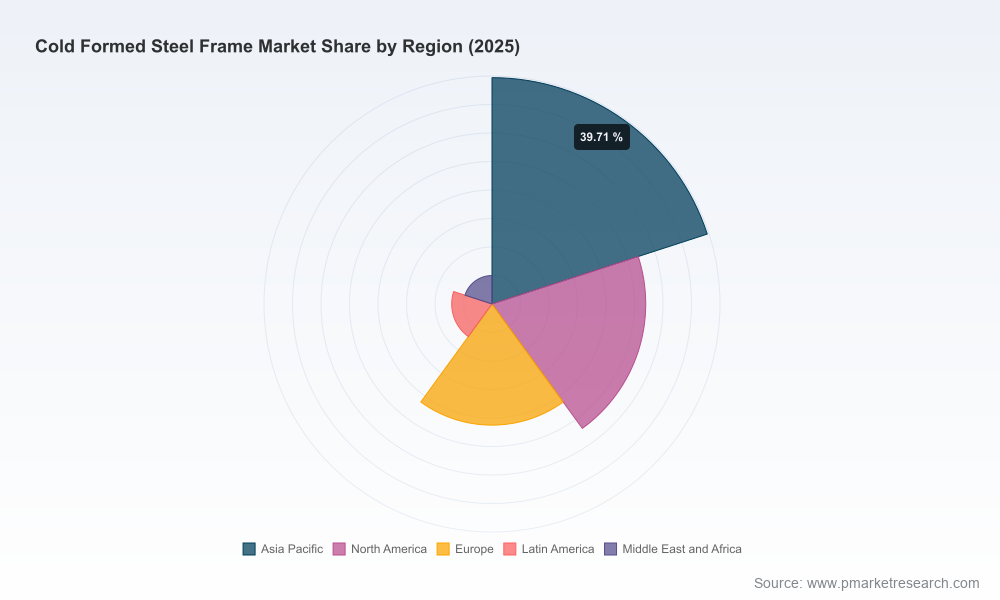

The global CFS frame market expanded from its post-2020 recovery base to reach approximately USD 39.86 Billion in 2025. Our model projects sustained expansion through the forecast horizon, reaching roughly USD 57.19 Billion by 2032, under a mid-cycle compound annual growth rate (CAGR) of 5.29% across 2026–2032. These headline metrics signal consistent demand growth, while a low market concentration (CR3 ≈ 12.5%, CR5 ≈ 18.8%) underscores an industry characterized by numerous regional specialists, niche roll-formers, and vertically integrated steel producers — a dynamic that shapes competitive strategy and M&A calculus.

Worldwide Cold Formed Steel Frame Market

Why this matters to 2026 decision-makers

- Budgeting and capital allocation: The mid-single-digit CAGR supports expansion or modernization of roll-forming capacity, but the fragmented competitive landscape argues for targeted, rather than blanket, capacity investments. Companies must prioritize flexible, scalable capital deployments over large, fixed expansions.

- Procurement and risk management: Volatility in hot-rolled coil (HRC) pricing is no longer theoretical. As of April 2026, U.S. Midwest HRC reached ~1,075 USD/T (up nearly 18% YoY), and North American HRC benchmarks were reported at roughly 1.05 USD/kg in March 2026. These raw-material movements materially affect margin profiles and contract negotiation strategies — firms need hedging playbooks, indexed contracts, and close supplier partnerships.

- Regulatory and code-driven product development: Recent updates in technical guidance and design specifications materially change product acceptance windows and engineering standards. Compliance-first players will gain faster market access in code-sensitive segments such as mid-rise and high-rise construction.

What the report contains — practical, transaction-ready insight

PW Consulting’s report is structured to move executives from insight to action. Core contents include:

Worldwide Cold Formed Steel Frame Market

- Market sizing and methodology: transparent models and assumptions with historical reconciliation (2020–2025) and scenario-based forecasts for 2026–2032; downloadable model included for client customization.

- Demand drivers and end-use dynamics: granular narrative on construction activity, modular and offsite adoption, and replacement cycles for renovation markets — with sensitivity analyses for macro and commodity shocks.

- Supply-side mapping: plant-level roll-forming capacity review, supplier tiers, integration pathways, and logistics constraints affecting lead times and working capital.

- Raw material price playbook: analysis of HRC price drivers, pass-through mechanisms, contract structures, and practical procurement hedging strategies.

- Regulatory and standards tracker: implications of recent technical guide and standards updates for product certification, testing, and go-to-market timing.

- Sustainability and compliance assessment: evaluation of Environmental Product Declarations (EPDs), embodied carbon scoring, and buyer procurement criteria that are increasingly shaping spec selection.

- Competitive landscaping: in-depth profiles of the sector’s strategic actors (steelmakers, roll-formers, system integrators, and machinery/software providers), with alignments, recent moves, and tactical playbooks for partnerships and M&A.

- M&A and corporate strategy toolkit: valuation yardsticks for platform and tuck-in opportunities, integration risks, and post-merger synergies for scale, distribution, and product breadth.

- Go-to-market playbook: prioritized sales motions by customer archetype, channel economics, lead-time guarantees, and prefabrication/installation value propositions.

- Implementation annexes: sample RFP language for low-carbon products, template supplier scorecards, and a list of KPI metrics for monitoring 100-day and 12-month rollouts.

Competitive landscape — who matters and why

The market is populated by a spectrum of participants — global steelmakers, regional roll-formers, precision equipment suppliers, and integrated framing system providers. Rather than presenting exhaustive rank tables, PW Consulting’s analysis highlights strategic roles and competitive postures among several market-shaping organizations:

- Major roll-formers and system providers (e.g., ClarkDietrich Building Systems, CEMCO): These players excel in distribution reach, code-compliant product portfolios, and project-based prefabrication for commercial and mid-rise construction. Their scale in North American channels and participation in industry bodies translate to early adoption of code updates and strong institutional relationships.

- Steel producers with downstream presence (e.g., Nucor, ArcelorMittal, Tata Steel, SSAB, BlueScope): Vertically integrated producers supply coil and finished sections, enabling margin capture through the value chain. Their strategic options include captive supply arrangements, long-term offtake contracts, and differentiated high-strength or coated offerings.

- Precision and niche specialists (e.g., Hadley Group, Metsec/voestalpine, FRAMECAD, Scottsdale Construction Systems): These firms provide high-accuracy roll-forming technology, software-driven design-to-fabrication workflows, and equipment sales that enable local partners to scale quickly. Technology licensing and machine-as-a-service models are emerging monetization pathways.

- Sustainability-first manufacturers (e.g., MarinoWARE, MRI Steel Framing): Producers publishing EPDs and offering low embodied carbon systems are increasingly specified by owners and developers pursuing green building certifications — a differentiator in public procurement and corporate real-estate strategies.

- Solutions integrators and component specialists (e.g., The Steel Network, Eisen Group, Network Framing Solutions, The Steel Network): These companies optimize connectors, bridging, and prefabricated systems for faster site assembly and modular construction — translating manufacturing innovations into on-site schedule compression.

PW Consulting’s company dossiers combine operational benchmarking, go-to-market maps, recent initiatives, and potential strategic moves tailored to each archetype. Recent industry events — from trade-show product introductions to updated technical guides and awards for code-compliant projects — are analyzed for their competitive implications.

Regulation, standards, and sustainability: turning compliance into advantage

Three contemporaneous developments are shifting the competitive landscape: (1) release of updated technical guidance by industry bodies aligning products with the latest building codes; (2) publication of the newest North American specifications for cold-formed structural members; and (3) broader buyer emphasis on embodied carbon measurements and EPD transparency. Firms that proactively align R&D, testing, and marketing with these touchpoints will shorten sales cycles and increase spec wins. PW Consulting’s report translates the standards language into specific product development checklists and certification timelines so teams can operationalize compliance within project delivery windows.

Raw-material dynamics and margin management

Rapid HRC price movements have a direct and immediate effect on cost of goods sold and contract profitability. The report provides tactical playbooks for procurement teams, ranging from short-term hedging models and index-linked pricing templates to supplier diversification scenarios and strategic inventory policies. We also quantify margin sensitivity across product families under several HRC price paths — enabling CFOs to stress-test budgets and negotiate resilient customer contracts.

Strategic implications and actions for 2026

- Prioritize modular/pre-fab capability: Buyers increasingly prize schedule certainty and reduced site labor. Investment in offsite fabrication and partner ecosystems delivers measurable premium capture in targeted channels.

- Differentiate on sustainability data: EPDs and cradle-to-gate reporting are no longer optional for certain customer segments — they are procurement must-haves. Early EPD publication shapes RFP outcomes and access to institutional pipelines.

- Lock in raw-material flexibility: Adopt layered procurement strategies combining spot, forward, and supplier-owned stock options to mitigate short-term price shocks while preserving working capital.

- Adopt a technology-first lens: Invest in design-to-fabrication software and precision roll-forming that reduce waste, lower per-unit labor, and speed project fulfilment.

- Be selective with M&A: Given the fragmented market, carefully structured tuck-ins that add distribution, prefabrication capacity, or unique technology often yield outsized returns versus platform mega-deals.

Recent industry signals we track

- Trade show activity and product launches continue to catalyze specification conversations for mid-rise and high-rise projects.

- Industry awards and technical guide updates are tightening the corridor for accepted practice — benefiting early adopters and certified vendors.

- Steel price volatility and supply-chain tightness have real implications for margin management and contractual terms in 2026.

- EPD publication and low embodied carbon claims are reshaping buyer shortlists in institutional and commercial procurement.

Conclusion — the practical value of the PW Consulting study

For executive teams preparing budgets, negotiating supplier agreements, evaluating M&A targets, or modernizing operations in 2026, our report translates market-level forecasts into executable playbooks. We combine quantitative forecasting with qualitative, operations-oriented guidance — and deliver tools that let commercial, procurement, and strategy teams implement actions within 90–180 day windows.

To preserve the competitive edge of subscribers and to comply with the “teaser” distribution approach for this release, our public summary highlights high-level market sizing, macro trends, and strategic implications, while detailed segment matrices, company-level dashboards, and downloadable financial models are available in the full report package. PW Consulting clients receive an interactive model, a 12-month implementation calendar, and a tailored briefing with our senior analysts.

Next steps

Executives interested in converting insight into prioritized action for 2026 should request PW Consulting’s full market brief and model. The package is designed to accelerate decision-making — whether you are optimizing procurement, plotting capacity investments, or shaping M&A strategy in the cold formed steel frame market.

For detailed analysis of this topic, please visit the official page:Worldwide Cold Formed Steel Frame Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com