Worldwide Lennox-Gastaut Syndrome Drug Market: Strategic Preview for 2026 Decision-Makers

Executive snapshot

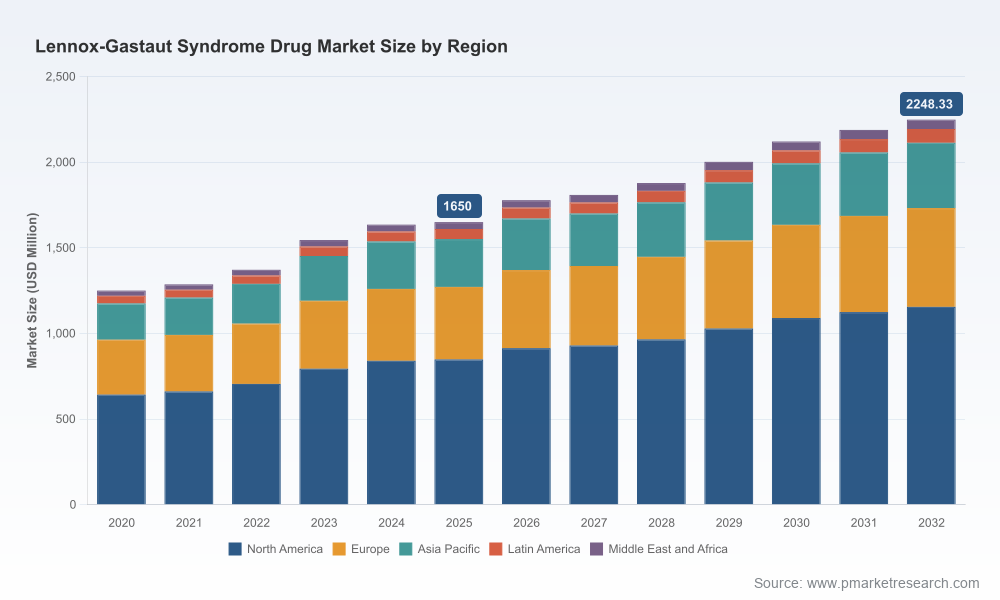

PW Consulting’s latest market intelligence on the Worldwide Lennox-Gastaut Syndrome (LGS) drug market synthesizes epidemiology, clinical comparators, payer dynamics, and commercial levers into a single decision-grade deliverable for 2026. At a macro level, the market has expanded from the low‑thousands (USD Million) in 2020 to an estimated USD 1,650 Million in the base year 2025, and—under our central projection—continues to grow at a compound annual growth rate (CAGR) of 4.52% across the 2026–2032 forecast window, reaching roughly USD 2,248 Million by 2032. This trajectory reflects both enduring demand for effective anti-seizure medications and structural shifts in access, pricing, and product mix that will define commercial outcomes over the next strategic planning cycle.

Worldwide Lennox-Gastaut Syndrome Drug Market

Why PW Consulting’s 2026 briefing matters

For corporate strategy, commercial, and BD&L teams, the LGS market is no longer a static niche. Several powerful forces are converging: a reshaped product landscape with recent regulatory activity and generic entries; growing payer scrutiny around high-cost branded therapies; and the emergence of real‑world evidence (RWE) that redefines value in payer conversations. Our report is built to be operationally useful in 2026: it reads like a battlefield manual rather than an academic treatise, pairing quantitative sizing and scenarios with concrete playbooks for market entry, formulary negotiation, and lifecycle defense.

Worldwide Lennox-Gastaut Syndrome Drug Market

- Macro sizing you can act on: consolidated historicals (2020–2025), base-year calibration (2025), and a probabilistic forecast (2026–2032)—all presented with sensitivity to reimbursement shifts and competitive stimuli.

- Concentration insight: the market shows mid-to-high concentration among the top players (CR3 ≈ 52.4%; CR5 ≈ 68.9%), indicating both incumbent advantage and meaningful opportunity for disruptive entrants with clear differentiation.

- Access-first perspective: scenario modelling of payer pathways, patient access barriers, and pricing elasticity under alternative reimbursement regimes.

Report composition — practical contents

The report is organized for rapid adoption by strategy teams and includes the following operational modules:

Worldwide Lennox-Gastaut Syndrome Drug Market

- Market sizing and validated forecasting framework with alternative scenarios reflecting differential uptake of branded ASMs and generics.

- Pipeline and launch impact analysis, including probability-weighted sales models and time-to-peak assumptions.

- Clinical comparator matrix and positioning playbooks mapping efficacy, tolerability, and monitoring burden to payer value drivers.

- Channel and distribution assessment tied to hospital, retail, and digital dispensing strategies—actionable guidance for contracting and hub services.

- Reimbursement playbook with dynamic pricing levers, evidence-generation pathways, and payer negotiation templates.

- Manufacturing and supply-chain risk assessment, with a focus on plant-derived cannabinoid sourcing and regulatory controls.

- Acquisition and partnership screening framework with candidate prioritization for add-on capabilities (formulation, specialty distribution, RWE platforms).

- Decision-support tools: purchase-ready slide decks, sensitivity calculators, and a one-page CEO briefing with recommended milestones for 12/24/36 months.

Competitive landscape — who matters and what to watch

The LGS therapeutic environment blends established broad-spectrum anti-seizure medication (ASM) manufacturers with specialist players commercializing novel or reformulated options. Key corporate actors profiled in the report include established innovators and specialty players—each with distinct strategic postures:

- Jazz Pharmaceuticals — with a plant-derived cannabidiol product that has anchored premium pricing and complex supply requirements.

- UCB S.A. — offering a reinvigorated entrant in fenfluramine that carries strong efficacy signals and evolving real-world persistence data.

- Lundbeck and Aquestive / Cosette — custodians of clobazam-based formulations where generic erosion and novel delivery formats coexist as both threat and opportunity.

- Eisai, GSK, AbbVie, Janssen, and Viatris-associated portfolios — long-standing ASM franchises with deep hospital relationships and broad formulary representation.

Across these players, strategic moves to monitor include lifecycle tactics (new formulations, indication expansions), defensive generics strategies, and evidence investments aimed at payer retention. Our profiles emphasize commercial playbooks—how each company currently wins formulary access, where they are most vulnerable, and the likely countermeasures incumbents will deploy when challenged.

Recent developments that change the playbook

- Generic approvals continue to reshape category economics. Early-2026 approvals for additional generics of established agents alter price reference points and create renegotiation pressure for hospital and retail contracts.

- Real-world evidence is influencing treatment persistence and payer coverage decisions. Claims-based analyses presented in 2026 highlight reasons for discontinuation and differential adherence that can be translated into targeted adherence programs and value-based contracting pilots.

- New clinical analytics—such as genetic DEE (developmental and epileptic encephalopathies) signal mining within trial datasets—are expanding the conversation about precision labeling and niche positioning for cannabinoids and other novel agents.

- Safety-led limitations remain salient: agents with severe adverse-effect profiles retain their place in therapy but are constrained to later lines with intensive monitoring requirements, which materially affects commercial potential and adoption timing.

Strategic imperatives for 2026 decision-making

Based on the market trajectory and competitive dynamics, PW Consulting recommends the following priorities for executive teams planning their 2026 agenda:

- Invest early in targeted RWE: prioritize studies that address payer-relevant endpoints—durability of response, healthcare resource utilization, and discontinuation drivers. Small, well-designed claims or registry programs can unlock formulary access and justify premium pricing.

- Differentiate beyond headline efficacy: articulate total cost of care propositions including monitoring burden, adverse-event management, and caregiver impact. Payers increasingly view value through net-system-cost lenses rather than unit price alone.

- Design a generics defense playbook: for brands facing imminent generic competition, deploy a suite of tactics—patient support programs, indication-specific data exclusivity strategies, novel delivery formats, and optimized contracting to preserve share.

- Secure cannabinoid supply resilience: for plant-derived products, invest in vertically integrated sourcing, controlled cultivation contracts, and redundancy in extraction capacity to avoid availability-driven market share loss.

- Pursue selective BD&L and M&A: target assets that fill portfolio gaps (e.g., pediatric formulations, digital adherence tools, specialty distribution partners) rather than undifferentiated scale.

- Implement flexible pricing & access models: consider outcome‑based contracts or indication‑based pricing where appropriate to bridge the short-term payer affordability gap while preserving long-term commercial upside.

- Prioritize hospital-channel tactics: the hospital setting remains a decision nexus for severe epilepsy; engaging pharmacy & therapeutics committees with peer-to-peer clinical evidence and burden-of-care analytics is essential.

How executives should use this report in 2026

The PW Consulting LGS market study is designed as a working document for the following use cases:

- Board-level go/no-go deliberations for late‑stage assets or geographic launches.

- Commercial launch planning—sequencing, pricing, and payer engagement schedules calibrated to our sensitivity scenarios.

- BD&L screening—shortlisting acquisition or licensing opportunities with quantifiable upside and defensible synergies.

- Operational planning—manufacturing scale decisions, supply-chain risk mitigation, and rare-disease patient support investments.

Methodology and confidence

Our forecasting integrates audited sales intelligence, regulatory timelines, claims and formulary data, and expert clinician input. Multiple scenarios were stress-tested—upside, downside, and policy-shock cases—to generate decision-ready probability-weighted outcomes. The result is a practical, defensible revenue curve for the market as a whole (2020–2032) and discrete, actionable implications for product- and company-level strategy without disclosing proprietary sub-segmentation that clients obtain in the full report.

Call to action

For teams charged with shaping 2026 priorities—whether prioritizing R&D investments, defending market positions, or pursuing strategic acquisitions—this analysis provides the tactical playbooks and quantitative backbone required to execute confidently. To access the full dataset, granular regional and channel modeling, and company-level commercial templates, please visit the PW Consulting report landing page where the complete Worldwide Lennox-Gastaut Syndrome Drug Market report and downloadable decision tools are available.

For detailed analysis of this topic, please visit the official page:Worldwide Lennox-Gastaut Syndrome Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com