The Middle East Blood Pressure Monitors Market Gains Momentum with Rising Focus on Early Disease Detection

Other |

2026-06-04 07:10:47

PW Consulting’s latest market research, “Worldwide Dal Mill Machine Market — Base Year 2025; Forecast 2026–2032,” delivers a focused intelligence package designed to inform capital allocation, product strategy, and operational planning for the coming planning cycle. The study synthesizes historical performance (2020–2025), a rigorous forecast (2026–2032 at a 6.12% CAGR), and a practical playbook for equipment manufacturers, processors, investors, and procurement teams operating in the pulse-processing value chain. While this announcement outlines the study’s strategic takeaways and signature findings, detailed segment-level tables and supplier scorecards are intentionally reserved for the full report to preserve the high-value, proprietary analysis that supports executive decision-making.

Worldwide Dal Mill Machine Market

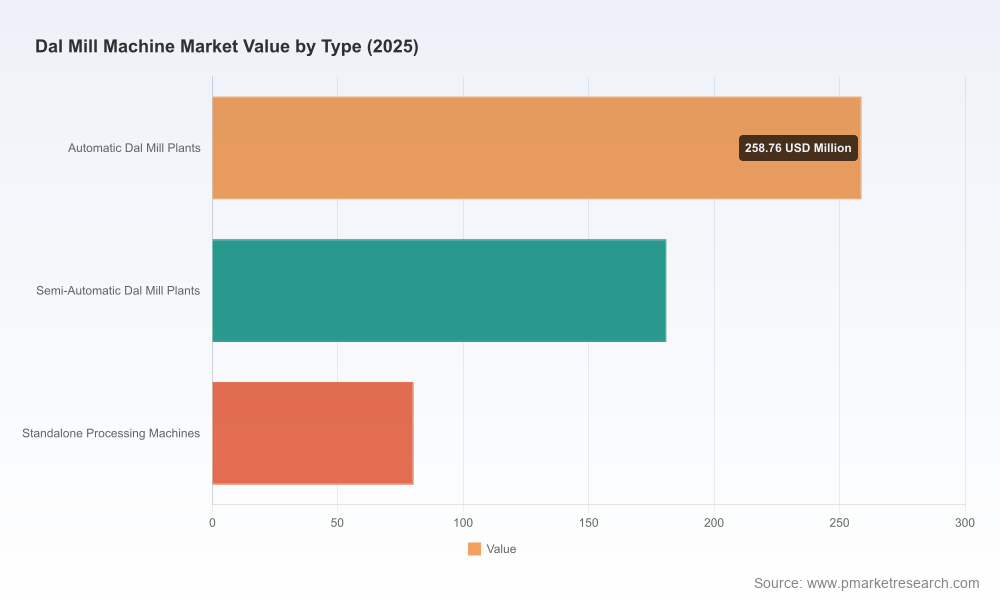

Base-year scale: The global dal mill machine market is anchored by a 2025 industry value defined in PW Consulting’s base-year assessment. From 2020 through 2025 the market exhibited steady expansion, driven by mechanization across key producing nations and increasing quality requirements from both domestic and export buyers.

Worldwide Dal Mill Machine Market

Forward trajectory: Our forecast conservatively models a compound annual growth rate of 6.12% between 2026 and 2032. This trajectory reflects a mix of demand-side modernization (automation, food-safety compliance) and supply-side constraints (raw-material cost pressure and skilled-labor dynamics).

Worldwide Dal Mill Machine Market

Market structure: Competitive concentration is moderate—our concentration metrics indicate a market where top-three vendors do not dominate, and the top-five collectively hold a minority share. This fragmentation creates opportunities for both focused niche players and acquisitive consolidators.

Regulatory inflection: The introduction of stricter equipment- and-process food-safety mandates has shifted procurement criteria from CAPEX-only decisions to CAPEX+COMPLIANCE models. Buyers that prioritize HACCP-ready, easy-to-validate systems will gain quicker route-to-market for export contracts and institutional customers.

Automation premium: Rising wages in the food-processing workforce and the need for consistent product quality are accelerating uptake of automatic and PLC-integrated plants. Decisions made in 2026 about whether to retrofit or replace will determine operating margins for a multi-year horizon.

Supply-cost shocks: Raw-materials used in machine fabrication experienced upward pricing pressure in late 2025. Procurement teams that lock in strategic supplier contracts or adopt design-for-cost approaches will be better insulated from margin erosion.

Feedstock growth: Expanding pulse production in principal growing regions has elevated the downstream need for higher-throughput and higher-yield milling solutions. This macro agricultural trend is a durable demand pull for modern dal-milling equipment.

Export dynamics and policy: Changes to export policy that favor domestic processing have nudged volumes toward local milling. This policy environment is increasing domestic investment in processing capacity while also reshaping equipment specifications for exporters seeking higher-grade outputs.

Cost and labor dynamics: Wage inflation in food processing and episodic increases in fabrication inputs are reinforcing the business case for automated, energy-efficient designs that reduce operating labor and improve throughput per square meter.

The market exhibits healthy product innovation and differentiated go-to-market models. PW Consulting’s vendor mapping identifies a spectrum of providers from highly integrated, fully automatic plant suppliers to compact, energy-efficient mini-mill manufacturers targeting small processors. Below are high-level profiles and strategic contrasts of representative market participants we examined in depth.

Milltec Machinery Pvt. Ltd. (Bengaluru, India) — Positioned as a leader in fully automatic plants, Milltec has increasingly focused on integrated cleaning, grading, splitting, and polishing lines. Recent showcase activity introduced AI-enabled sorting to the market, signaling a move toward higher-margin, tech-enabled solutions for large processors and exporters.

Pramick Engineering Consultants Pvt. Ltd. (Hyderabad, India) — Specializes in compact and semi-automatic machines tailored to micro-to-small processors. Their February 2025 launch of an energy-efficient 500 kg/hr model underscores the attractiveness of low-footprint products where energy efficiency and capex constraints matter most.

GBS Engineering Enterprises (Hyderabad, India) — Known for turnkey processing lines with yield-optimizing modules such as emery polishers and gravity selectors. Their recent delivery of a high-capacity plant to a major exporter demonstrates their capability to execute large-scale, export-oriented projects.

Jay Khodiyar Industries & Narnoli Engineering Works (Rajkot, India) — These firms emphasize compact plant design, high mechanical reliability, and aggressive after-sales networks—appealing to decentralised millers upgrading from manual operations.

Bharat Agritech, Masoor Industries, United Oil Mill Machinery — These vendors show differentiated strategies: PLC-integrated systems for quality assurance, product-specific mills (e.g., specialized masoor machines), and equipment variants optimized for finish and shelf-life via unique polishing and aspirating subsystems.

Collectively, the vendor landscape is characterized by modular innovation, targeted product portfolios, and varying degrees of digital integration. The market’s moderate concentration leaves room for specialist players to defend niches while larger suppliers pursue system sales and technology-led differentiation.

Technology adoption: Demonstrations of AI-driven sorting and end-to-end automation at industry shows in late 2025 indicate that premium buyers will soon expect data-centric quality assurances as a baseline.

Project wins: Major turnkey deliveries signal continued investment by large processors and exporters—an important validation of demand for higher-capacity plants among export-oriented operators.

Cost inputs: A notable uptick in fabrication-grade steel pricing in late 2025 has direct implications for BOM costs and capital budgeting; prudently, buyers should incorporate supply-price contingency allowances into 2026 capex requests.

Buyers (Processors & Cooperatives): Prioritize HACCP-ready equipment and modular designs that allow phased automation. When evaluating bids, incorporate lifecycle cost models (energy, labor, spare-parts) rather than focusing solely on sticker price.

OEMs & Equipment Vendors: Invest in retrofit kits and service platforms to capture the large installed base seeking incremental automation. Build partnerships for local steel procurement or hedge material costs; consider offering long-term service contracts to stabilize revenue streams.

Investors & PE Firms: The modest market concentration suggests attractive roll-up opportunities. Targets with strong service franchises and digital upgrades are preferable—these assets can be scaled and stitched into national service networks to capture aftermarket margins.

Policy & Development Agencies: Programs that subsidize upgrades to HACCP-compliant equipment can catalyze modernization among smaller processors. Technical assistance should be paired with credit access to accelerate adoption.

Detailed historical and base-year market sizing by product type, capacity band, and geography, plus a seven-year scenario forecast under alternative macro assumptions.

Vendor benchmark matrix and supplier scorecards covering technology stacks, service footprints, installed-base profiles, and go-to-market positioning.

Procurement playbook including specification checklists, compliance validation templates, CAPEX/OPEX modeling worksheets, and vendor negotiation tactics.

Case studies and implementation roadmaps for both retrofits and greenfield plants, with payback timelines calibrated to current input-cost environments.

2026 represents a strategic inflection point for stakeholders in the dal mill machinery ecosystem. The combination of regulatory tightening, feedstock availability, labor-cost inflation, and mounting requirements for consistency and export-quality output means that capital and operational decisions made this year will shape competitiveness for the remainder of the decade. PW Consulting’s study encapsulates the market’s scale, a disciplined forecast (6.12% CAGR to 2032), and an operationally-focused set of recommendations intended to shorten time-to-value for buyers and suppliers alike.

For executives seeking the full segment-level intelligence, vendor scorecards, and the proprietary financial tools referenced above, the complete report and supporting datasets are available through PW Consulting’s official channels. Access to the comprehensive tables and granular segmentation is the fastest path to converting the strategic direction outlined here into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Worldwide Dal Mill Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com