Laboratory Equipment Services Market Trends Driving the Future of Scientific Research

Causes |

2026-07-09 12:33:17

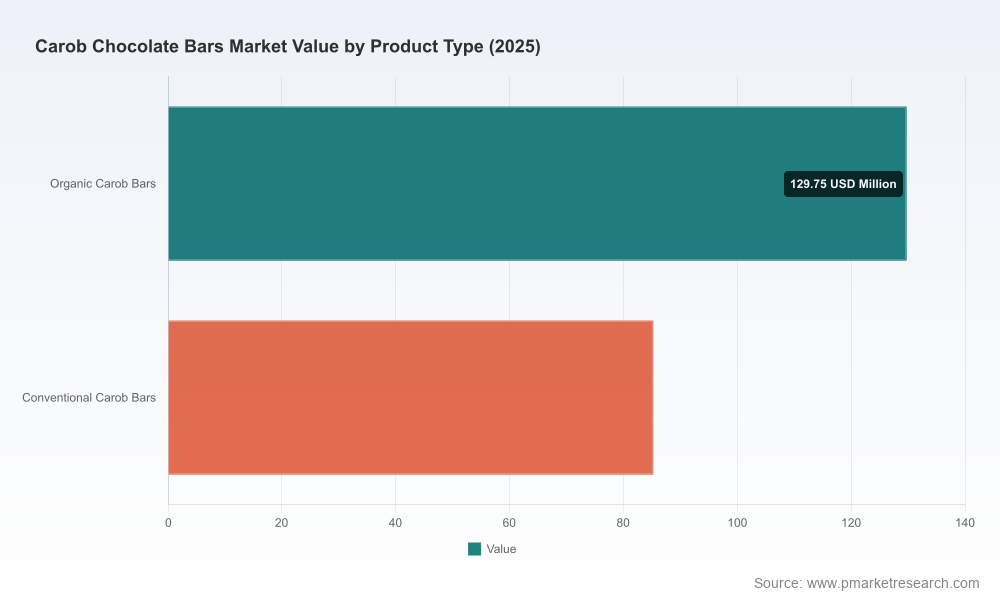

The niche yet fast-evolving carob chocolate bars market is transitioning from artisanal curiosity to a strategic growth category for health-first confectionery portfolios. Our new PW Consulting report, with base year 2025, models the market through 2032 and shows a robust compound annual growth rate (CAGR) of 7.2% from 2026–2032. After expanding from an estimated USD 150 million in 2020 to USD 215 million in 2025, the market is projected to pass USD 230 million in 2026 and continue toward a substantially larger mid-decade opportunity by 2032.

Carob Chocolate Bars Market

Timing and scale: The 7.2% CAGR reflects a window in which product investment, channel expansion, or targeted M&A can compound value meaningfully within a three- to five-year hold horizon.

Carob Chocolate Bars Market

Low concentration equals high optionality: The market’s headline concentration metrics point to a fragmented competitive structure (three- and five-firm concentration remain modest), creating multiple entry or consolidation points for market entrants and incumbents alike.

Carob Chocolate Bars Market

Margin leverage via formulation and ingredient innovation: Emerging ingredients and processing techniques reduce dependence on cocoa while creating distinct nutritional claims (clean-label, vegan, lower-sugar). These are not incremental product tweaks but potential margin and positioning levers for brands seeking differentiation.

PW Consulting’s Carob Chocolate Bars Market report is built as a practical, board-room-ready playbook rather than an academic exercise. Key deliverables include:

Quantified market trajectory and scenario forecasts (2026–2032) with downside, baseline, and accelerated-adoption scenarios for planning and valuation stress-testing.

Go-to-market blueprints: SKU prioritization matrices, retail assortment frameworks, and recommended margin stacks by channel for rapid retail trials and DTC scale-up.

Price-sensitivity and raw-material stress models integrating real-world pod and export price movements to quantify cost-pass-through and product-pricing elasticity.

Regulatory and labeling compliance matrix for priority export markets, including checklist-ready packaging and claims verification steps.

Supplier and sourcing playbook: mapped supplier archetypes, quality control KPIs, and contract templates for spot vs. long-term sourcing under volatile harvest cycles.

Commercial diligence annexes for M&A: target screening criteria, obtainable synergies, and a short-list methodology tailored to small-batch manufacturers and ingredient innovators.

Consumer segmentation and positioning guides built from primary interviews and retail shelf tests—designed to accelerate SKU-market fit in 90 days.

Three dynamics will shape executive decisions in 2026.

Consumer demand for functional indulgence: Clean-label and plant-based trends accelerate trial and repeat purchase. Carob formulations frequently achieve materially lower sugar content than conventional chocolate, enabling health-forward claims without sacrificing indulgence.

Ingredient and cost volatility: Carob pod supply can be subject to regional harvest cycles and logistical constraints. For example, trade data and market monitoring show wholesale carob pod prices in Spain reached approximately USD 8.97/kg in late 2025 for certain export volumes, while global average export and import price references from 2024 indicate export averages near USD 873/ton and import averages around USD 1,206/ton. These reference points matter when modeling cost pass-through and margin management.

Regulatory nuance in export markets: Nutritional labeling and plant-origin product rules vary. Some markets require explicit nutritional fact tables and origin declarations on imported plant-based items—an operational consideration for packaging, lead times, and trade compliance.

The category today is led by agile, purpose-driven brands and a set of ingredient innovators. The competitive map includes specialty producers and supplier brands that combine organic sourcing, vegan positioning, and sustainability claims. Key profiles covered in the report include:

Missy J’s (Colorado, USA): Focused on organic, gluten- and dairy-free carob confections leveraging Australian organic carob—positioned for North American health channels and premium DTC.

The Carob Kitchen (Port Elliot, South Australia): Farm-to-bar producer offering a range of milk-style, vegan and low-sugar formulations—illustrative of vertically integrated strategies that control sourcing and processing.

Caroboo (UK): A brand emphasizing flavor variety and sustainability (compostable packaging) and actively expanding health-retail distribution in the UK.

CarobMe / Carobmē (Australia / International): Producer of several organic and allergen-free bars with product innovation in texture and flavor, suitable as a model for export-oriented product development.

D&D Chocolates (UK): Family-run artisan strategy with a focus on multi-allergen-free positioning for specialty channels.

Carob World (Portugal) and The Australian Carob Co.: Supplier and exporter archetypes that provide raw material and ingredient services to the finished goods players.

Recent category moves underscore rapid commercialization: a key UK player secured expanded retail listings with a major health-food chain in late 2025, academic teams reported flavor-boosting techniques designed to close taste gaps with cocoa, and ingredient firms have launched prebiotic carob fiber ingredients that broaden the bars’ functional appeal. These developments accelerate both mainstream shelf presence and formulation innovation.

Our modelling emphasizes three levers for commercial resilience:

Diversified sourcing and hedging: Combining spot procurements with forward contracts and strategic inventory cushions reduces exposure to short-term pod-price spikes.

Ingredient upgrading: Emerging ingredients—such as prebiotic fibers derived from carob—offer opportunities for premium pricing, health claims, and consumer equity while also enabling blends that reduce dependence on single-origin harvests.

Local processing hubs: Near-market processing mitigates tariff and labeling complexity, shortens time-to-shelf, and supports certifications demanded by health retailers.

Based on our field testing and retailer interviews, three immediate moves can accelerate commercial traction:

Prioritize a compact SKU set for retail test-and-learn (two core formats, one seasonal flavor) while maintaining a broader DTC range to harvest consumer insights and lifetime-value data.

Leverage sugar-reduction messaging and allergen-free claims as primary trial drivers, with secondary messaging around sustainability and origin to uplift willingness-to-pay.

Adopt a hybrid distribution strategy: targeted health retail listings for brand credibility combined with DTC subscription models to build frequency and margins.

Run an 18-month pilot combining a defined retail test, DTC launch and promotional calendar, with KPIs tied to repeat rate, price elasticity and shelf velocity—use our provided templates to build the business case.

Negotiate supplier arrangements that include indexation clauses tied to defined pod-price or export-price benchmarks; use the report’s cost-sensitivity tool to stress-test P&L outcomes under adverse price scenarios.

Invest in incremental product R&D to adopt flavor-enhancement techniques and prebiotic formulations; early adopters can convert health-seeking consumers while defending against cocoa-substitution perceptions.

Assess bolt-on acquisitions or strategic partnerships in processing and ingredient supply to secure margin and supply continuity; the fragmented competitive landscape presents acquisition targets with realistic synergy pathways.

For executives planning 2026 capital allocation, product roadmaps, or distribution strategies, the carob chocolate bars market offers an attractive combination of growth, differentiation and acquisition potential—provided decisions are anchored in granular supply, cost and consumer data. PW Consulting’s report equips leadership teams with the quantitative scenarios, operational playbooks and due-diligence annexes required to move from concept to scale in under 12 months.

To access the full dataset, including the granular regional, product-type and channel breakdowns, SKU-level pricing scenarios and downloadable modeling templates, visit the report landing page. The public brief above intentionally highlights the strategic contours while reserving the detailed segmentation and proprietary forecasts for the full report and client workshops—designed to inform board-level decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Carob Chocolate Bars Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com