HIFU Treatment and Modern Medical Trends

Other |

2026-04-10 10:24:58

As PW Consulting publishes its latest Worldwide Areca Nut Market report, this briefing articulates the strategic value embedded in the research for corporate decision‑makers preparing plans for 2026. The study synthesizes market history, near‑term developments and medium‑term forecasts to deliver an operationally focused intelligence package: a revenue‑grade market trajectory, competitive dynamics, policy and trade risk mapping, and playbooks that translate insight into executable moves. Below we summarize the report’s high‑level signals and the judgment calls leaders should be making now — while intentionally withholding granular segment spreadsheets to preserve the report’s role as the authoritative source for teams that require full, proprietary detail.

Worldwide Areca Nut Market

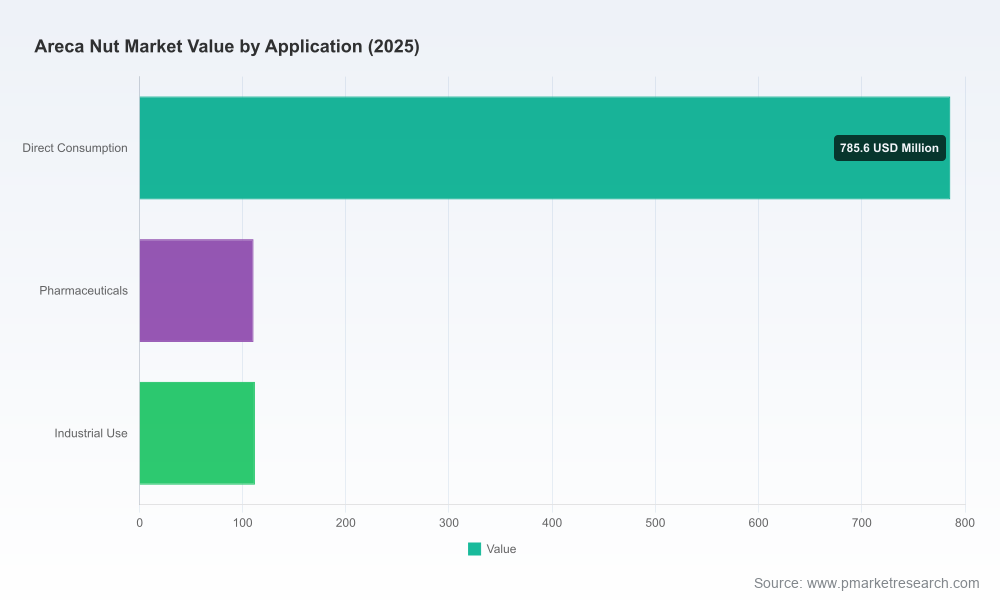

The global areca nut market has shown steady expansion through the base period. On a USD Million basis, the market grew from roughly USD 840 million in 2020 to approximately USD 1,008 million in 2025. Our forecast framework anticipates continued growth across the 2026–2032 horizon, underpinned by steady demand pockets and increasing emphasis on hygienic processing and specialized industrial uses. The model yields a compound annual growth rate (CAGR) of 3.88% for the forecast period, projecting a mid‑decade market size comfortably north of the 2026 starting point and reaching a market value in the low thousands of USD Million by 2032.

Worldwide Areca Nut Market

These aggregates matter because they define the realistic scale of opportunity for manufacturing investments, export capacity expansion and product diversification initiatives. For buyers, the trajectory shapes procurement sourcing windows and long‑term contracts; for processors and exporters, it frames the business case for capital expenditure in sorting, drying and packaging lines that meet global compliance standards.

Worldwide Areca Nut Market

Validated market sizing and a transparent forecasting model calibrated to 2020–2025 history and extending through 2032, with scenario and sensitivity layers for price, input cost and trade shock assumptions.

An industry playbook covering procurement strategies, post‑harvest loss mitigation, processing upgrade sequencing, and export readiness checklists tailored for commercial teams and investor due diligence.

Competitive intelligence dossiers on leading players, including procurement structures, value‑added propositions, processing capabilities and likely strategic responses to policy shifts.

Regulatory and trade risk mapping that links enforcement regimes and tariff interventions to near‑term price volatility and demand reallocation opportunities.

Operational KPIs and investment thresholds — e.g., break‑even capex envelopes for optical sorting and hygienic packaging lines, throughput targets to justify greenfield plants, and metrics for measuring supplier resilience.

In line with the “trailer” principle, this brief signals the kinds of segment and regional detail contained in the report without reproducing the proprietary splits. Corporates will find full regional, type and application breakdowns in the primary report, together with downloadable dashboards that support procurement, M&A and export planning workflows.

Regulatory enforcement: Import controls and food‑safety enforcement are active levers. Notably, as of March 2026, the U.S. Food and Drug Administration continues to maintain import alerts and detention without physical examination (DWPE) guidance for products containing areca nut — a persistent trade risk for exporters targeting North American markets. Exporters must invest in traceability and contaminant controls if they seek to maintain or grow NAFTA or U.S. access.

Trade policy protectionism: India’s October 2025 extension of minimum import price measures and a 100% basic customs duty on areca nut imports signals a durable, protective posture intended to safeguard domestic growers and processors. This creates both a commercial moat for domestic suppliers and a friction point for global buyers sourcing from elsewhere.

Input‑cost pressure: Agricultural input inflation — fertilizer and pesticide costs — has materially raised smallholder breakeven points in producing regions. The report’s scenarios show that a sustained increase in input costs of the magnitude observed in recent years materially compresses farm margins and increases volatility in raw material availability and quality.

Health and reputational constraints: The International Agency for Research on Cancer (IARC/WHO) classification and resulting local bans and labeling mandates in various jurisdictions elevate compliance, packaging and marketing costs for value‑added consumer products containing areca.

Government support and cluster initiatives: Subnational programs — such as recent agro‑processing cluster expansions and incentives for mechanization — enhance prospects for reducing post‑harvest losses and scaling processing density. These are decisive when evaluating greenfield or brownfield investments.

The areca nut industry remains moderately consolidated at the top: three‑firm and five‑firm concentration metrics indicate a market where leading cooperatives and processors meaningfully shape price formation and quality benchmarks. This concentration favors players who can integrate procurement with processing and export capabilities.

Cooperative advantage — The CAMPCO Ltd (India): As a major cooperative, CAMPCO’s recent infrastructure expansion and warehouse investments are classic examples of a member‑centric model reducing procurement friction and stabilizing farmer economics. For firms considering procurement partnerships, cooperatives offer a route to secure traceable volumes at stable quality.

Exporters upgrading for compliance — Surya Exim and peers: Upgrades in optical sorting and hygienic packaging underline a clear market bifurcation: exporters that achieve international food‑safety alignment retain access to premium channels, while non‑compliant suppliers risk exclusion. Capital prioritization toward hygiene, sorting and certification is now non‑negotiable for export‑oriented processors.

Regional processors and traders — GM Group, Swastika International, and a wide set of Indian traders: These players continue to dominate domestic and regional value chains, supplying a wide array of grades and finishing services for local consumption and cross‑border trade. Their agility in grading and distribution remains a competitive asset in price‑sensitive segments.

Emerging processing hubs — SSB Agro and regional entrants in Northeast India and Southeast Asia: New high‑capacity units backed by subnational support signal a diffusion of processing capacity away from traditional geographies. Investors should evaluate logistics and feedstock stability when considering these newer hubs.

International suppliers — Indonesian and Vietnamese exporters: Suppliers from Indonesia and Vietnam maintain strategic relevance for buyers seeking diversification, but they must navigate buyer preferences and regulatory compliance in end markets.

Recent, report‑covered developments (Q1–Q2 2026) — foundation laying for CAMPCO’s Vitla warehouse, Karnataka’s cluster program expansion, Surya Exim’s facility upgrade, and SSB Agro’s plant inauguration in Mizoram — illustrate the interaction of policy, cooperative action and private capex that will shape medium‑term capacity and quality trajectories.

Prioritize export‑grade compliance investments. For processors and exporters that target developed‑market buyers, investing early in optical sorting, hygienic packaging and documented traceability is a market‑entry gatekeeper and a pricing lever.

Hedge raw‑material and policy risk. Use blended sourcing strategies (cooperatives, integrated suppliers, and diversified geographies), layered with short‑term price hedges and contractual quality agreements to manage volatility arising from input‑cost inflation and sudden trade policy shifts.

Partner with cooperatives and cluster programs. Public‑private collaboration can accelerate access to farm‑level volumes and quality improvements — and reduce procurement costs linked to post‑harvest losses.

Assess concentration dynamics for M&A and alliance plays. The market’s concentration profile favors bolt‑on acquisitions that secure processing capacity and procurement catchment. Acquisition targets should be evaluated for certification readiness and shelf‑life compliance capabilities.

Embed public‑health and reputational risk into product strategy. For brands and ingredient buyers, repositioning, reformulating or seeking clear regulatory pathways will be essential in jurisdictions with labeling or use restrictions.

Clients tell us they need forecasts that are not just directional but actionable. Our report pairs a transparent, replicable forecasting engine with an operational playbook: thresholds for capex, procurement contract templates, export readiness checklists and prioritized vendor mappings. The work is explicitly designed for cross‑functional teams — strategy, procurement, operations and compliance — so that insights become decisions within a quarter‑by‑quarter planning cycle.

We also provide scenario constructs that stress‑test strategies against calibrations of input inflation, tariff shocks and trade‑policy enforcement. This allows executives to identify “no‑regret” moves (e.g., hygiene upgrades) and contingent plays that become attractive under specific policy outcomes.

This brief intentionally omits proprietary segment tables and detailed regional or application splits to preserve the report’s role as the primary source for full market granularity. PW Consulting’s comprehensive report contains the granular breakdowns, company dossiers, downloadable datasets (USD Million unit standard) and the interactive tools described above.

Senior executives preparing 2026 budgets — whether considering greenfield processing capacity, export market entry, or downstream product reformulation — should schedule a briefing with our team to review the full dataset, model assumptions and tailored scenario outputs. For project teams, the report can be licensed with onsite modeling support and a customized nine‑week implementation playbook.

PW Consulting remains available to partner on rapid due diligence, supplier audits, and investment screening to convert the market’s projected steady growth and structural shifts into measurable strategic advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Areca Nut Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com