Geospatial Market Transforming Industries Through Advanced Location Intelligence And Analytics

Other |

2026-06-18 06:50:55

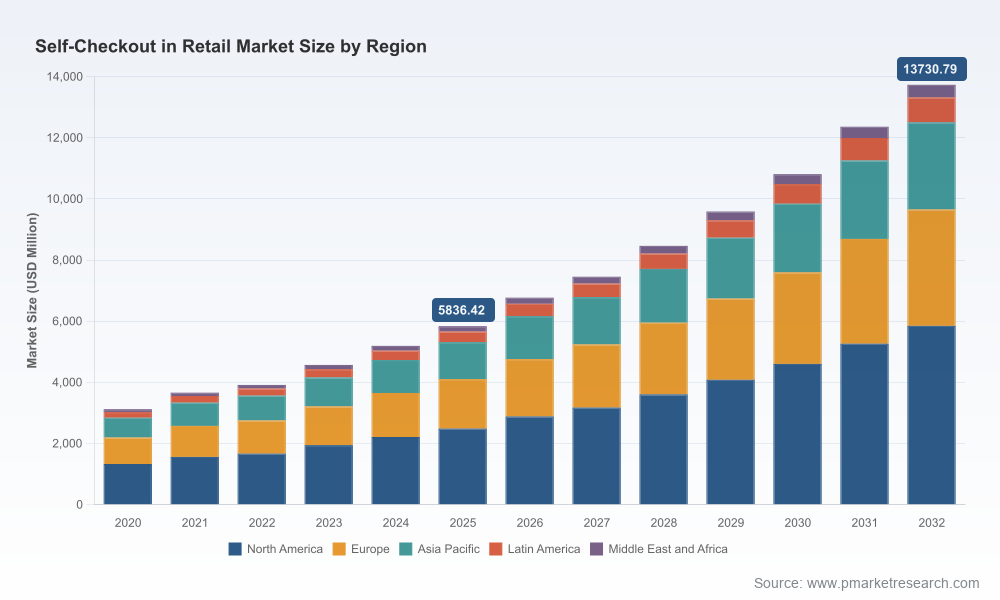

Retail leaders entering 2026 face a market in structural acceleration. PW Consulting’s new Worldwide Self‑Checkout in Retail Market study (base year 2025; forecast 2026–2032) documents how self‑checkout has moved beyond convenience into a core operational lever: between 2020 and 2025 the market more than doubled in scale, and our forecast shows the sector expanding from roughly USD 5.8 billion in 2025 to an expected USD 13.7 billion by 2032, reflecting a compound annual growth rate of 13.01% across the forecast horizon. For executives evaluating investment, rollout, and vendor strategies this report translates macro momentum into tactical next steps—without giving away the proprietary segmentation that will be available in the full release.

Worldwide Self-Checkout in Retail Market

Self‑checkout is no longer a single technology choice. It is a systems decision that touches stores, payments, shrinkage controls, data governance, and customer experience. The PW Consulting report is designed as a decision support tool: it quantifies market momentum, assesses vendor positions, and delivers executable playbooks for pilots, scale‑ups, and M&A diligence. Below are the strategic takeaways we expect boards, CIOs, and heads of retail operations to prioritize in 2026.

Worldwide Self-Checkout in Retail Market

Invest with conviction, but in modular increments. The market’s sustained double‑digit growth justifies meaningful capital allocation toward checkout automation. However, the optimal path is a staged program that emphasizes modular, cloud‑native platforms and interchangeable hardware so retailers can shift between assisted, hybrid, and fully autonomous models without forklift upgrades.

Worldwide Self-Checkout in Retail Market

Tie ROI to labor‑cost sensitivity and shrinkage metrics. Rising labor costs and seasonal staffing shortages continue to push adoption. Use the report’s operator models to map local labor economics against expected shrinkage dynamics and determine break‑even timelines specific to store archetypes.

Prioritize data governance and privacy by design. New state‑level privacy laws in the U.S. and expanding data‑protection expectations globally mean self‑checkout deployments that use cameras, vision, or biometric sensors must be architected for compliance from day one. Our compliance checklists and threat models convert legal exposure into procurement requirements.

Design for loss prevention that complements customer experience. AI‑enabled vision, weight verification, and integrated shrink‑reduction modules are now standard discussion points—not optional extras. The report presents frameworks to balance frictionless checkout with measurable shrink reduction without alienating customers.

Make vendor modularity a mandatory procurement specification. High vendor concentration in core platform layers means negotiation leverage varies by component. Our vendor scorecards and negotiation playbook help buyers secure open APIs, cloud portability, and clear SLA provisions for software updates and machine availability.

PW Consulting’s full study was built to be used, not shelved. Highlights include:

Robust market trajectory and topline forecasts (2020–2032) to inform capital planning and five‑year programs.

Segment and scenario analyses that outline which solution types, components, and store formats drive value under alternative labor and regulatory environments (note: the detailed segment tables and regional splits are available in the full report release).

Vendor profiles and competitive benchmarking, including capability matrices, go‑to‑market strategies, and recommended engagement models for tier‑1 and specialist suppliers.

Implementation playbooks: pilot design templates, rollout sequencing (store selection criteria, KPI dashboards), integration checklists for POS/payment systems, and TCO/ROI calculators tailored to retail formats.

Regulatory and privacy risk matrix coupled with practical mitigations—covering camera and vision data, retention policies, and the contractual language needed to limit liability.

Case studies and operator interviews that illustrate shrink management, customer adoption curves, and hybrid staffing models that preserve service while reducing labor intensity.

The self‑checkout ecosystem is a mix of systems integrators, hardware specialists, sensor suppliers, and AI start‑ups. Market concentration metrics indicate that a relatively small group of platform providers controls a large share of installed value at the top end, while an active long tail supplies commoditized hardware and regional services. Key strategic positions we highlight in the report include:

NCR Voyix Corporation — positioning around cloud‑native, modular solutions and continuous software delivery. Their emphasis on adaptive checkout models makes them a default choice for large, multi‑format chains seeking centralized control with local customization.

Diebold Nixdorf — strong focus on AI for shrink reduction and item recognition. Their Vynamic Smart Vision capabilities illustrate how shrink prevention is being embedded into transaction flows rather than layered on afterwards.

Toshiba Global Commerce Solutions — known for highly customizable kiosks and hybrid checkout strategies that balance throughput and supervision, attractive to retailers with complex payment and loyalty integrations.

Fujitsu — a leader in RFID and computer‑vision approaches for high‑velocity supermarkets and hypermarkets; partnerships and hackathons show active experimentation with new interfaces and faster scanning models.

Component and sensor specialists (Zebra, Honeywell, Datalogic) — their hardware robustness and integration experience remain a procurement differentiator for high‑traffic stores where uptime and ruggedness matter.

AI disruptors (e.g., Mashgin) — represent a ‘vision‑first’ approach that can bypass barcode dependence; useful in higher‑SKU mix environments but requiring careful shrinkage and privacy controls.

Regional and specialty vendors — companies with strong European, Asian, or convenience‑store footprints offer important local capabilities and integration services that large platform vendors may not provide natively.

Recent vendor moves underscore market direction. In March 2026, NCR Voyix emphasized a next‑generation cloud offering with modular hardware and real‑time software updates—validating the shift to SaaS‑style checkout. Earlier launches of compact AI kiosks and AI shrink‑reduction modules reflect a competitive dynamic where cloud, vision, and compact form factors intersect. Partnerships and hackathons (for example, Fujitsu’s collaboration with GK Software) show vendors racing to lock in integrations and proof points in strong regional markets.

Deployments in 2026 must be assessed through three non‑negotiable lenses:

Regulatory compliance: Multiple U.S. state privacy laws that came into force in 2025 increase obligations for systems that capture camera or sensor data. Contractual clauses, data retention policies, and localized compliance checklists in the report help mitigate legal exposure.

Operational resilience: The business case for self‑checkout must include loss prevention strategies and fallbacks. Some retailers have scaled back deployments in high‑shrink locations; others have reduced shrink through AI‑assisted verification and optimized attendant placement. The report quantifies tradeoffs and provides templates for experiment design.

Cybersecurity and privacy: Retail privacy maturity lags many industries, while the average cost of a data breach remains material (industry benchmarks show average breach costs near USD 3.91 million). We provide a prescriptive security baseline for camera and vision systems, and contract language to limit vendor risk.

Practical uses we recommend for 2026:

Shortlist vendors using our vendor-scorecard approach to rapidly filter for cloud portability, API openness, and proven shrink‑reduction capability.

Run a two‑phase pilot: (a) prove technical integration and shrink metrics in a small, representative store set; (b) demonstrate operations and customer adoption at scale. Use our KPI dashboards and A/B templates to measure impact.

Negotiate commercial terms that separate hardware refreshes from software subscriptions and secure upgrade pathways to ensure long‑term TCO predictability.

Embed privacy and cybersecurity requirements into procurement RFPs, using our clauses and threat model to force vendor alignment early.

Consider strategic partnerships or bolt‑on acquisitions to capture in‑house capabilities that are differentiating for your customer base (e.g., computer vision, RFID, or payment orchestration).

This preview highlights macro momentum, strategic choices, and competitive direction. The full Worldwide Self‑Checkout in Retail Market report from PW Consulting contains the detailed segment-level datasets, regional and application splits, proprietary vendor scoring, and downloadable TCO/ROI models that commercial buyers and corporate strategists rely on to finalize 2026 budgets and pilots. If you are preparing a rollout plan, negotiating multi‑year platform contracts, or assessing acquisition targets, the full dataset and playbooks will convert headline growth into executable plans.

For practitioners seeking a high‑fidelity, actionable view of how to prioritize investments in 2026, PW Consulting’s complete report delivers the granular evidence and tactical templates you need—while this preview outlines the strategic context that makes acting this year imperative.

For detailed analysis of this topic, please visit the official page:Worldwide Self-Checkout in Retail Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com