PW Consulting Strategic Preview: Worldwide Twist Dispensing Closure Market — What Every Executive Needs to Know Going into 2026

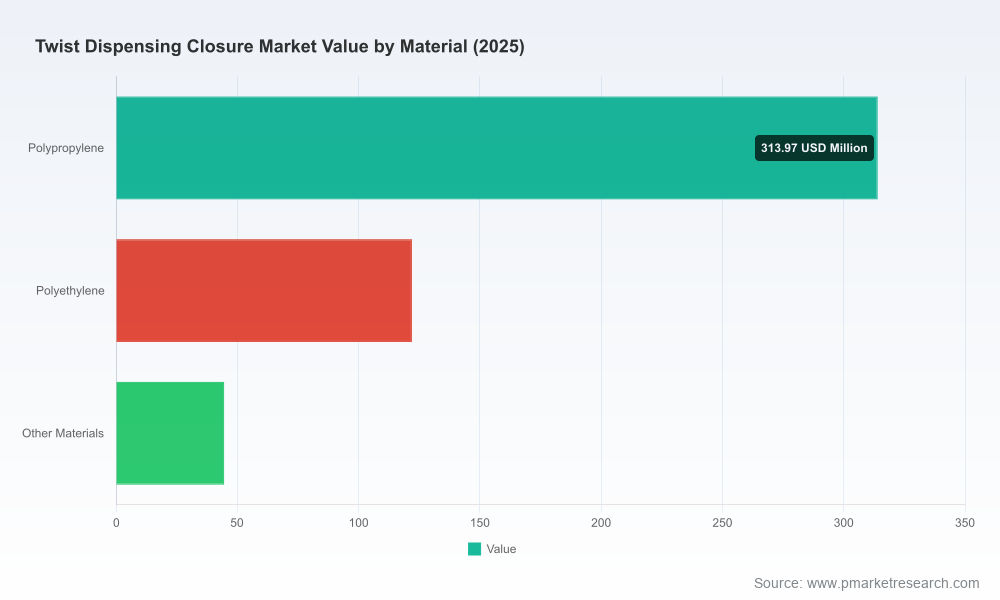

PW Consulting’s forthcoming Worldwide Twist Dispensing Closure Market report (base year 2025; forecast 2026–2032) synthesizes market-scale rigor with practical, decision-focused guidance for packaging executives, procurement leaders, R&D heads, and corporate strategists. The global market has expanded from roughly USD 375.2 million in 2020 to an estimated USD 480.5 million in 2025, and our modeling projects continued momentum through the forecast window — reaching roughly USD 678.8 million by 2032 under a 5.06% compound annual growth rate (CAGR) across 2026–2032. This preview explains why 2026 is a pivotal year for choices that will determine competitive positions through the end of the decade, and outlines the specific, actionable intelligence the full report delivers.

Worldwide Twist Dispensing Closure Market

Why 2026 Is a Strategic Inflection Point

- Regulatory acceleration: Extended Producer Responsibility (EPR) frameworks and single‑use plastics measures in Europe — and spreading policy signals in North America — materially change design and procurement trade-offs. Tethered-closure mandates and recyclability targets are forcing choices between legacy multi-material constructs and mono-material, recyclable alternatives.

- Material-price volatility: Resin markets are no longer a background input cost. Regional polypropylene price differentials observed in early 2026 (for example, pronounced variation between Europe, North America and Northeast Asia) create short- and medium-term margin pressure and influence regional sourcing, inventory strategies, and supplier selection.

- Consumer and retail expectations: Convenience, perceived safety (child-resistance, tamper evidence), and environmental credentials are converging as non-negotiables for household and personal-care formats — forcing earlier-than-expected upgrades to closure functionality and composition.

- Industry consolidation and supplier innovation: The mix of global incumbents and regional specialists, plus an uptick in product launches and hybrid material solutions, is reshaping channel dynamics and speed-to-market advantages.

Market Dynamics That Will Drive 2026 Decisions

- Design-for-recyclability is now table stakes. The combination of regulatory pressure and retailer sustainability targets is rapidly increasing demand for mono-material, fully recyclable dispensing closures. This creates both technical challenges (seals, liners, gas-tight requirements) and commercial opportunities for suppliers who can deliver validated mono-material solutions at scale.

- Sustainability is a supply-chain conversation. The adoption of post-consumer recycled (PCR) content — particularly in polyethylene overcaps and related components — is accelerating. The immediate implication: specifications, testing protocols, and supplier audits must be updated in 2026 to ensure performance and circularity claims hold up under scrutiny.

- Price and availability of feedstocks will affect sourcing strategies. With polypropylene and HDPE price divergence across regions, many firms will need to redesign vendor contracts, implement hedging or index-linked pricing, and consider nearshoring or multi-sourcing to mitigate exposure.

- Product complexity is increasing. Modern twist-dispensing closures are no longer simple injection-molded parts; they may incorporate child-resistant mechanisms, induction seals, elastomeric inserts for gas-tight seals, or tethered constructs. These features alter tooling amortization, cycle times, and capital requirements for converters and brand owners alike.

Competitive Landscape — What Leading Suppliers Are Signaling

The sector is characterized by a mix of multinational integrators and nimble specialists. Market concentration is moderate: the top three suppliers account for roughly 32.4% of market revenues and the top five for about 45.8%, indicating both the presence of established scale players and meaningful opportunities for niche or regional competitors.

Worldwide Twist Dispensing Closure Market

- Silgan Holdings Inc. (Stamford, CT) — Silgan’s strength lies in proven twist-off and PT closure platforms and in mono-material variants designed for food and beverage applications. Their product depth and packaging integration capabilities make them a natural partner for large beverage and food companies looking to transition to recyclable formats with minimal SKU disruption. Strategic consideration for buyers: Silgan is well positioned for volume transitions but may command premium pricing for integrated application systems.

- AptarGroup Inc. (Crystal Lake, IL) — Aptar has been intentionally pushing innovation at the intersection of convenience and sustainability. Recent product activity evidences a focus on child-resistant and eco-forward twist dispensers for personal care and pharma. For 2026, Aptar represents a high-probability partner for brands pursuing rapid performance upgrades while maintaining sustainability claims.

- Berry Global Group, Inc. (Evansville, IN) — Berry brings scale in closure molding and integrated dispensing systems for personal care and household products. Their ability to pair closures with compatible pump/valve systems is an advantage for customers seeking end-to-end solutions rather than discrete components.

- Closure Systems International (CSI) (Indianapolis, IN) — CSI is notable for sustainable closure designs and high-speed application competencies. Their tethered and flip designs address both regulatory compliance and high-volume application needs, making them an attractive choice for beverage and dairy customers transitioning under regulatory timelines.

- O.Berk Company LLC (Hackensack, NJ) and Mold‑Rite Plastics (MRP Solutions) — These suppliers dominate in flexible catalog breadth and rapid prototyping for specialty applications (e.g., viscous formulations, niche industrial uses). Their agility suits early-stage pilots and regional rollouts.

- Amcor Plc, TriMas Packaging, BERICAP, and Guala Closures — Each brings differentiated strengths in global footprint, tamper-evidence, and high-margin specialty closures. For executives contemplating strategic M&A or supplier rationalization in 2026, these firms represent both potential consolidation partners and competitive benchmarks for product and sustainability roadmaps.

Recent Supplier Activity — Signals to Watch

- Aptar’s 2024 launches emphasize built-in child-resistant functionality paired with eco-friendly material choices — a template for how premium solutions combine regulatory compliance with sustainability positioning.

- New product introductions such as TulipCap™ (2026) show a practical middle path: hybrid morphologies that use polyethylene overcaps with elastomeric inserts to deliver gas-tight performance while enabling use of PCR content and easier recycling streams.

What the Full Report Delivers — Executive-Level, Operationally Ready

Beyond headline market sizing, the report is structured as a tactical playbook for 2026 decisions. Highlights include:

Worldwide Twist Dispensing Closure Market

- Robust market-sizing methodology with reconciled historicals (2020–2025) and forward-looking scenarios (2026–2032) — enabling stress-testing of strategic plans against alternate policy and price futures.

- Supplier scorecards that evaluate technical capability (e.g., mono-material sealing), application engineering support, tooling economics, and sustainability credentials — designed for use in RFQs and strategic sourcing discussions.

- Detailed materials and cost-sensitivity analysis, including regional resin-price scenarios and their impact on unit economics and margin sensitivity.

- Regulatory tracker and implementation playbook for EPR and tethered‑closure mandates — including recommended timelines for design conversion, testing protocols, and retailer engagement templates.

- Product-roadmap templates that align closure innovation to channel needs (e.g., e-commerce, retail shelving, on‑the‑go formats), plus a prioritized list of pilot projects that deliver fastest ROI.

- Scenario-based M&A and partnership screens, leveraging concentration benchmarks and capability gaps to identify likely targets and integration risks.

- Operational deployment guides: pilot testing checklists, quality-acceptance criteria for PCR usage, supplier qualification workflows, and capital-equipment decision criteria for converters.

How Leading Companies Should Use This Intelligence in 2026

- Procurement and sourcing: Recalibrate supplier contracts to include feedstock-indexed clauses, PCR quality specifications, and acceleration pathways for mono-material substitution. Use our supplier scorecards to streamline supplier rationalization.

- Product development: Prioritize mono-material and tethered closure pilots for SKUs at highest regulatory and retail scrutiny. Incorporate elastomeric or induction‑seal solutions where gas-tight performance is essential.

- Manufacturing and capex planning: Model line upgrades or new tooling investments against our scenario suite. Decide in 2026 whether to retrofit current tooling for mono-material runs or invest in new, higher‑automation cells that reduce per-unit costs over the forecast period.

- Sustainability strategy: Translate policy exposure into tangible timelines for PCR adoption, labeling claims, and end‑of‑life takeback or design-for-recycling programs — using our regulatory tracker as the operational calendar.

- M&A and partnership strategy: Use the concentration metrics and capability assessments to identify consolidation targets that fill functional gaps (e.g., sealing expertise, regional fill-and-apply strength) or material supply chain weaknesses.

Concluding Perspective

The twist dispensing closure sector is transitioning from a largely commoditized component market to a strategic battleground defined by material science, regulatory compliance, and system‑level integration. With global market value growing from mid‑single digits in the early 2020s to an expected USD 678.8 million by 2032 under a 5.06% CAGR (2026–2032), companies that make disciplined, evidence-based choices in 2026 — about materials, supplier partners, and capital allocation — will capture outsized share and margin improvements across the decade.

This article is a strategic preview designed to demonstrate the depth of analysis available in PW Consulting’s full Worldwide Twist Dispensing Closure Market report. To preserve the tactical value of the research to subscribers and clients, we have intentionally withheld detailed segment-level figures in this public summary. For the complete dataset, supplier scorecards, scenario models, and an operational playbook tailored for immediate deployment in 2026, visit our report page or contact PW Consulting to arrange a briefing and data license.

For detailed analysis of this topic, please visit the official page:Worldwide Twist Dispensing Closure Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com