PW Consulting Releases Strategic Preview: Worldwide Non-Thermal Food Processing Market — Essential Intelligence for 2026 Decisions

PW Consulting today publishes a strategic preview derived from our forthcoming market research report, Worldwide Non‑Thermal Food Processing Market (base year 2025, historical coverage 2020–2025, forecast 2026–2032). This briefing highlights the report’s value for corporate leaders planning capital allocation, technology adoption, and M&A activity in 2026 — while deliberately reserving detailed segment-level figures and proprietary models for the full report.

Worldwide Non-Thermal Food Processing Market

Top‑line market context

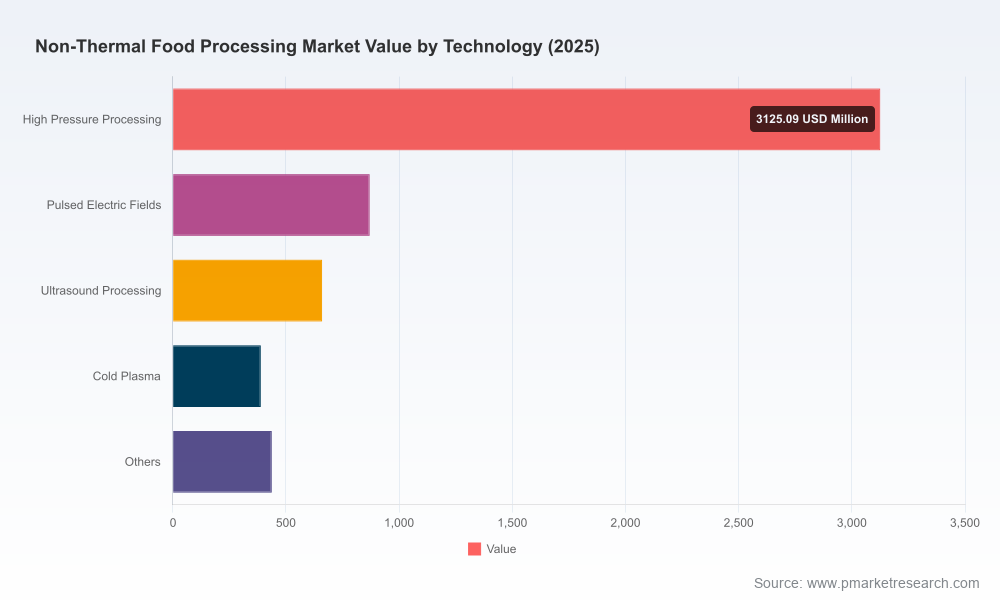

The global non‑thermal food processing market is at an inflection point. After sustained expansion in the early 2020s, the market reached roughly USD 5.48 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of around 10.0% over the 2026–2032 forecast period, with the total market roughly doubling by the end of the horizon. This trajectory reflects accelerated commercial adoption across beverages, meat and seafood, fresh produce, dairy, and adjacent formats as processors seek shelf‑life extension and quality retention without thermal degradation.

Worldwide Non-Thermal Food Processing Market

Why this matters for 2026 strategic decisions

- CapEx prioritization: A double‑digit CAGR means equipment investment windows will create advantage for early movers in 2026 — but the timing, scale, and technology choice (HPP, PEF, ultrasound, cold plasma, etc.) materially affect ROI and plant throughput. Our report provides decision frameworks to align CapEx cadence with product mix and margin targets.

- Commercial differentiation: Brands that can credibly market “fresh‑like” quality with verified safety and shelf‑life will capture premium placement. Non‑thermal processing is a route to differentiation, but execution risk (packaging, cold chain, regulatory alignment) is non‑trivial.

- M&A and partnership playbook: Market concentration and supplier dynamics signal both consolidation opportunities and strategic supplier partnerships. We quantify target attributes and integration risk in a 2026 context to accelerate due diligence.

- Regulatory compliance as a competitive moat: Regulatory recognition of specific non‑thermal methods has created a compliance floor, but cross‑jurisdictional requirements (e.g., novel food frameworks, export clearances) create friction for scaling. The report maps these friction points to go‑to‑market timelines.

What the PW Consulting report delivers — practical, operational, and actionable

The full report is structured to move beyond high‑level forecasts and into operational decision support for 2026. Highlights include:

Worldwide Non-Thermal Food Processing Market

- Executive decision dashboards: Scenario‑driven KPI dashboards that translate market growth paths into plant throughput, estimated CapEx timing, and revenue potential for defined product portfolios.

- Technology selection playbooks: Comparative frameworks for HPP, PEF, ultrasound, cold plasma and hybrid approaches — considering cycle times, energy and utility profiles, packaging constraints, throughput economics, and product quality outcomes.

- Capital and lifecycle economics: Total cost of ownership models, unit economics under multiple utilization bands, and break‑even analyses that incorporate maintenance schedules and spare‑parts logistics for 2026 procurement planning.

- Implementation checklists: Plant layout guidance, cold‑chain integration points, sanitation and HACCP adaptations, and workforce skilling roadmaps that reduce time‑to‑value.

- Regulatory and market access matrix: A practical guide to export and labeling pathways across major trading corridors, plus compliance checklists tied to non‑thermal method validation protocols.

- M&A and supplier diligence tools: A scoring template for vendor selection, acquisition target screening, and integration risk heatmaps — designed to streamline 2026 transaction cycles.

- Commercial adoption playbooks: Pricing sensitivity models, trade promotion simulations, and retailer submission templates to accelerate shelf entry while protecting margin.

- Risk and contingency scenarios: Monte Carlo‑based downside scenarios and stress tests for raw material volatility, labor cost inflation, and regulatory changes through 2032.

To respect the “trailer” principle, we showcase these capabilities and the intellectual property embedded in them here, while withholding the granular tables, regional/application splits, and proprietary scoring outputs which are available in the full report and online portal.

Competitive landscape — who will shape adoption in 2026

Non‑thermal processing is supported by a defined set of equipment and systems suppliers, with varying strategic positions across technologies and value‑chain roles. The market exhibits moderate concentration — reflecting both a set of global leaders and a competitive long tail of specialized providers — and this concentration dynamic is central to 2026 sourcing and partnership strategies.

- Hiperbaric (Burgos, Spain): A recognized global leader in high‑pressure processing (HPP) equipment, Hiperbaric continues to push yield and throughput improvements designed for juices, meats, and dairy. Recent product updates demonstrate a focus on operational efficiencies that matter in 2026 procurement decisions.

- JBT FoodTech (Chaska, Minnesota, USA): Offers industrial HPP systems and integrated non‑thermal processing lines. JBT’s expansion of manufacturing capabilities in growth markets signals capacity to support large‑scale rollouts and service networks crucial for fast adopters.

- Multivac Group (Wolfertschwenden, Germany): Specializes in coupling HPP with packaging systems, enabling integrated solutions that reduce handling steps and regulatory friction — a compelling proposition for food processors targeting retailer specifications.

- Elea Technology GmbH (Quakenbrück, Germany): Focused on Pulsed Electric Field (PEF) systems, Elea is positioning PEF as a go‑to for cell disruption applications in fruits, veg and potato processing — a segment where texture and color retention are commercial differentiators.

- Pulsemaster (Ochten, Netherlands): Supplies PEF equipment optimized for extraction and preservation workflows and serves as an important supplier for processors pursuing ingredient efficiency and product quality gains.

- Steriflow (Thyssenkrupp) (Quimper, France): Offers a portfolio spanning autoclaves and HPP systems, blending thermal and non‑thermal capabilities suitable for processors requiring flexible processing lines.

Recent vendor developments point to both incremental improvement and strategic capacity moves: product launches that optimize yields, trade‑show demonstrations validating new use cases, and manufacturing expansions in growth geographies. These supplier actions influence lead times, total cost of ownership, and service access for 2026 adopters.

Regulatory and supply‑side dynamics that will influence 2026 outcomes

- Regulatory validation: Key jurisdictions increasingly recognize defined non‑thermal methods as equivalent alternatives for pathogen control in certain product classes. This recognition shortens certification timelines but does not eliminate the need for product‑level validation — a nuance that affects launch sequencing and international trade plans.

- Cross‑border market access: Exporters must navigate novel food and import authorizations in some trading corridors. Compliance timelines and dossier requirements should be factored into 2026 commercialization roadmaps to avoid costly delays.

- Raw material and labor pressures: Processors should plan for commodity price and wage pressures that can compress margins if not mitigated by yield gains or pricing power. Supplier selection, automation levels, and process yields directly determine sensitivity to these cost inputs.

How executives should use this strategic preview in 2026 planning

Use this preview as a decision filter in three practical ways:

- Prioritize pilots with measurable economics: Select one or two product lines for near‑term non‑thermal pilot programs and require business cases with payback horizons aligned to the 2026 budget cycle.

- Negotiate capacity and service guarantees: Given supplier concentration patterns, secure service level agreements and spare‑parts commitments up front to de‑risk supply bottlenecks in 2026 rollouts.

- Integrate regulatory strategy with commercial launch: Build dossier preparation and validation timelines into the go‑to‑market plan to avoid market access delays, especially for cross‑border exports.

PW Consulting’s full Worldwide Non‑Thermal Food Processing Market report contains the detailed models, vendor matrices, and playbooks that operationalize the guidance summarized above. For procurement teams, operations leaders, corporate strategy groups, and private‑equity sponsors sizing investments in 2026, the full publication translates market potential into executable actions and measurable KPIs.

Next steps

To access the complete dataset, segmentation breakdowns, vendor scoring, and the 2026 decision playbook, please visit the PW Consulting report page. The full report includes interactive Excel models, scenario dashboards, and a subscription option for quarterly market updates through the forecast period.

PW Consulting remains available for bespoke briefings, capital planning workshops, and vendor due‑diligence engagements tailored to clients preparing decisive moves in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Non-Thermal Food Processing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com