Rhinoplasty in Riyadh for Functional Breathing and Cosmetic Improvement

Health |

2026-07-08 06:16:07

PW Consulting’s latest market study — the Worldwide Automotive Optoelectronic Market (base year 2025; forecast 2026–2032) — distills the rapid evolution of light- and sensor-driven subsystems that are reshaping vehicle architecture, safety systems, and user experience. With the global market having reached roughly USD 6.25 billion in 2025 and forecast to expand at a compounded annual growth rate of approximately 13.85%, the sector is entering a phase where product innovation, regulatory qualification and supply-chain positioning will decide winners and losers.

Worldwide Automotive Optoelectronic Market

Timing matters: 2026 will be the first full planning year after several regulatory inflection points and supply shocks — firms need a strategy that is calibrated to accelerated demand for sensing and dynamic lighting while accounting for persistent geopolitical and materials risks.

Worldwide Automotive Optoelectronic Market

Capital allocation: the market’s growth profile warrants both growth-stage investments (product R&D, LiDAR/VCSEL/CMOS scaling) and defense spending (qualification, reliability, ISO/ASIL compliance). Our report identifies the priority investment buckets and the expected time-to-revenue for each.

Worldwide Automotive Optoelectronic Market

Competitive playbook: consolidation and differentiation are happening simultaneously. The top tier of suppliers already captures a material share of industry sales; the tactical options we outline (vertical integration, IP licensing, specialized partnerships) are designed to help mid-tier suppliers and OEMs choose repeatable paths to margin improvement and share gains.

Operational risk management: supply continuity, wafer availability and qualification lead times have become strategic constraints. This study gives procurement and operations leaders the scenario-based roadmaps needed to keep vehicle programs on schedule while optimizing cost and quality.

This is not a collection of high-level forecasts alone. The report is structured as a decision-support toolkit, combining market sizing and trend analysis with practical artifacts that are immediately usable in boardrooms and program reviews.

Validated market sizing and growth trajectories (base year 2025; seven-year forecast window 2026–2032) with sensitivity bands and upside/downside scenario modeling tied to macro and regulatory catalysts.

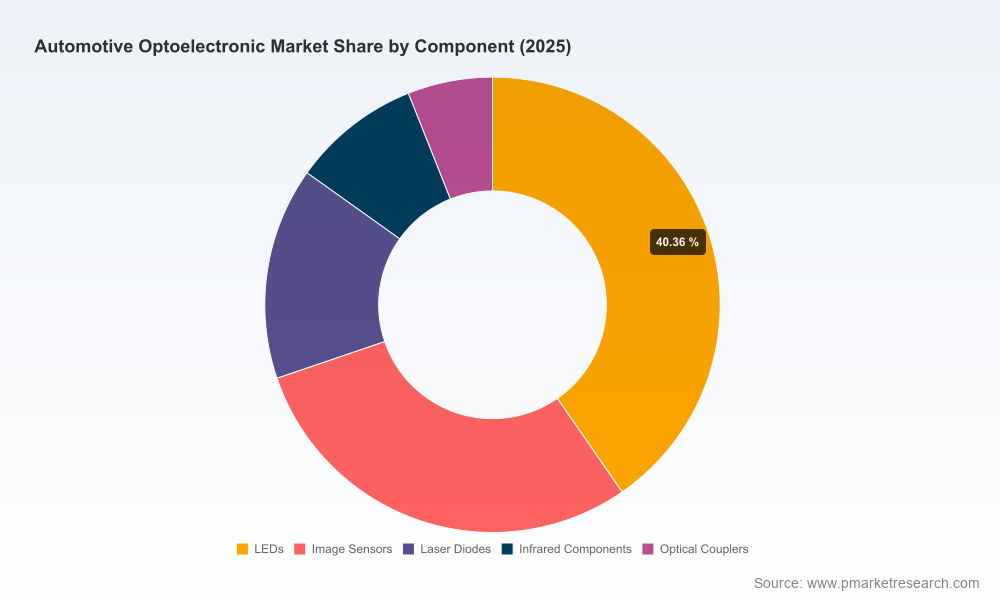

Technology roadmaps for core optoelectronic families (LEDs, laser diodes, image sensors, infrared components and optical interconnects), including maturity curves, qualification timelines and unit-cost breakpoints that drive OEM adoption decisions.

Supply-chain scorecards and template RFPs — vendor evaluation matrices that combine technical, quality and geopolitical risk factors (e.g., foundry exposure, OSAT dependence, rare-raw-material sourcing).

Commercial playbooks for OEMs, Tier-1s and component vendors covering go-to-market, bundling strategies, and licensing models for software-enabled lighting and perception subsystems.

M&A screening framework and prioritized candidate profiles: practical diligence checklists tuned to IP, silicon capacity, automotive qualification pedigree and aftermarket potential.

Regulatory impact assessment: actionable steps to align product development to safety standards and region-specific mandates, and a supplier certification timeline that links to vehicle program milestones.

The report synthesizes four converging dynamics that will define strategic choices in 2026:

Rapid demand for perception and active lighting. Adoption of camera-based ADAS and advanced lighting architectures continues to broaden across vehicle segments. Suppliers that can couple lighting function with sensing capabilities (e.g., VCSELs co-packaged with detectors, matrix laser modules) will command premium positions.

Regulatory acceleration. Mandates such as camera-based emergency braking and speed assistance have moved perception from optional to baseline in many markets. At the same time, ISO 26262-like functional safety expectations raise the bar for qualification — firms must embed ASIL-compliant design and evidence generation early in product roadmaps.

Supply-chain and geopolitical pressures. National incentives for semiconductor manufacturing and episodic disruptions to foundry capacity create both risk and opportunity. Programs that localize critical wafer capacity or secure multi-sourced supply for key epiwafers and image sensor dies will enjoy program-level resilience.

Technology bifurcation. Short- and mid-range LiDAR, CMOS image sensors with stacked architectures, and high-power LED/laser light sources are moving from lab demos to vehicle integration. Design wins in 2026 will favor suppliers that demonstrate repeatable manufacturability and low-latency qualification paths.

The market is neither a fragmented scramble nor a closed oligopoly; it is a competitive arena with a clear top tier and a dynamic middle. The concentration measures indicate that the leading firms together hold a significant slice of industry revenues, but there remains ample room for specialized challengers and regional champions.

ams‑OSRAM and Lumileds are doubling down on high-performance illumination and laser-matrix solutions, moving toward integrated light-sensing modules for adaptive beams and new HMI concepts.

Nichia and Seoul Semiconductor continue to push emitters — higher lumen densities and platform approaches for modular headlamp assemblies are differentiators they exploit.

Sensor leaders (Sony, OmniVision, onsemi, STMicroelectronics) are racing on stacked CMOS and global-shutter architectures to reduce size, lower power, and meet automotive image fidelity requirements under low-light conditions.

Semiconductor incumbents such as Infineon and ROHM are leveraging power and analog expertise to deliver integrated driver and sensing solutions that simplify Tier‑1 integration.

Interconnect and connector specialists (TE Connectivity) and diversified optoelectronics vendors (Everlight) remain critical as systems-level enablers for data transmission and mechanical robustness.

Recent commercial and product moves (from multi-pixel laser modules and adaptive headlamp platforms to new automotive global-shutter sensors) validate the trend toward more complex, software-driven optoelectronic systems. However, product demonstrations are only the first step — automotive qualification, supply continuity and cost-of-integration determine commercial success.

Safety mandates (camera/ADAS requirements) are accelerating baseline demand for image sensors and related optoelectronics. Companies that lack automotive-grade functional safety processes will face longer time-to-market and increased warranty exposure.

Public policy and incentives for semiconductor manufacturing are reshaping capital flows. Players that can tap national funding programs or structure joint ventures to localize capacity can realize both cost and timing advantages.

Supply disruptions (historic examples include seismic events that affected wafer fab throughput) underscore the need for dual-sourcing strategies and regional buffer capacity for critical dies and epiwafers.

Raw-material and substrate pricing (e.g., GaN-on-Si dynamics) affects cost curves. While price volatility has moderated recently due to capacity additions, procurement teams must build pricing pass-through and hedging into multi-year supply contracts.

Prioritize qualification pipelines. Treat ISO/ASIL evidence creation and OEM qualification slots as scarce resources — schedule them early, and allocate headcount and test-facility CAPEX accordingly.

Adopt a tiered sourcing framework. For critical components (imagers, VCSELs, high-power lasers), secure at least dual sources across different geographic clusters to mitigate single-point-of-failure disruptions.

Monetize systems integration. LED and sensor providers should explore software-enabled feature monetization (OTA-upgradable light functions, perception feature enablement) and tiered licensing with OEM partners.

Assess M&A for speed-to-market. For companies lacking automotive-grade IP or capacity, small-to-medium acquisitions of foundry-backed design houses or specialized module integrators can cut time-to-first-production materially.

Design for serviceability and spare-part economics. With more vehicles shipping richer optoelectronic stacks, aftermarket support and diagnostics will become non-trivial revenue and cost levers.

In keeping with the “trailer” principle, this briefing highlights the strategic contours and major implications of the optoelectronic market for 2026 decision-making. The full report contains granular, segment-level forecasts, regional demand matrices, supplier-specific revenue estimates, and downloadable model workbooks that support scenario planning and investment committees. These detailed datasets and company scorecards are intentionally withheld here to preserve the value of the primary research delivered to subscribers.

For strategy teams, supply-chain leaders and corporate development groups preparing 2026 plans, our recommendation is straightforward: leverage this horizon to lock in qualification timelines, secure diversified capacity for critical optoelectronics, and evaluate bolt-on acquisitions that accelerate systems integration capabilities. PW Consulting’s full report provides downloadable datasets, supplier scorecards and a prioritized action checklist to convert market opportunity into reliable program wins.

To access the full Worldwide Automotive Optoelectronic Market report, including the complete forecasts, segment-level analysis and tactical toolkits, please visit our report page or contact your PW Consulting account representative.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Optoelectronic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com