Worldwide Glaucoma Diagnostics Market: Strategic Imperatives for 2026 — PW Consulting Insight Brief

As glaucoma diagnostics enters a phase of methodical, technology-led expansion, executive teams face a dual challenge: capture growth driven by imaging and AI while navigating tightening regulatory and reimbursement landscapes. PW Consulting’s latest Worldwide Glaucoma Diagnostics Market report (base year 2025) synthesizes five years of historical performance, scenario-based forecasts to 2032, and a high-resolution competitive and regulatory map designed for boardroom decision-making in 2026.

Worldwide Glaucoma Diagnostics Market

Why this report matters for 2026 strategy

Our analysis projects continued expansion from the 2025 baseline, underpinned by a steady compound annual growth rate (CAGR) of approximately 5.0% across the 2026–2032 forecast window. The market’s persistent growth reflects three structural forces: (1) broader adoption of advanced imaging modalities in routine ophthalmic workflows; (2) the migration of diagnostics into ambulatory and home settings; and (3) incremental value capture from software-enabled analytics and AI. For leaders planning M&A, portfolio prioritization, or commercialization strategies in 2026, the report translates these structural drivers into concrete investment priorities and risk mitigations.

Worldwide Glaucoma Diagnostics Market

Top-line health check

- Post-pandemic recovery consolidated through 2024–2025 has set a new baseline for capital and service investments in glaucoma diagnostics.

- Forecast confidence is reinforced by a multi-scenario approach that stress-tests uptake under divergent regulatory and reimbursement regimes.

- Market concentration is meaningful: the top three companies account for a substantial share of industry revenues, and the top five approach two-thirds of the market — a dynamic that shapes pricing power, partnership opportunities and acquisition targets.

Actionable strategic themes for 2026

- Shift from device-only to data-enabled value propositions. Manufacturers that pair hardware with validated analytics and clear clinical outcomes unlock differential pricing and recurring revenue streams from software subscriptions and cloud services.

- Design for regulatory predictability. With non-contact tonometers classified as Class II devices in the U.S. and more jurisdictions tightening AI transparency requirements, companies need integrated regulatory roadmaps early in product development to avoid delayed market access.

- Reimbursement-first commercialization. Payer acceptance varies by procedure and code — in 2025 several CPT codes relevant to glaucoma diagnostics continue to determine clinical economics at the practice level. Sales strategies that explicitly address reimbursement data and coding support win faster adoption among hospitals and large clinic groups.

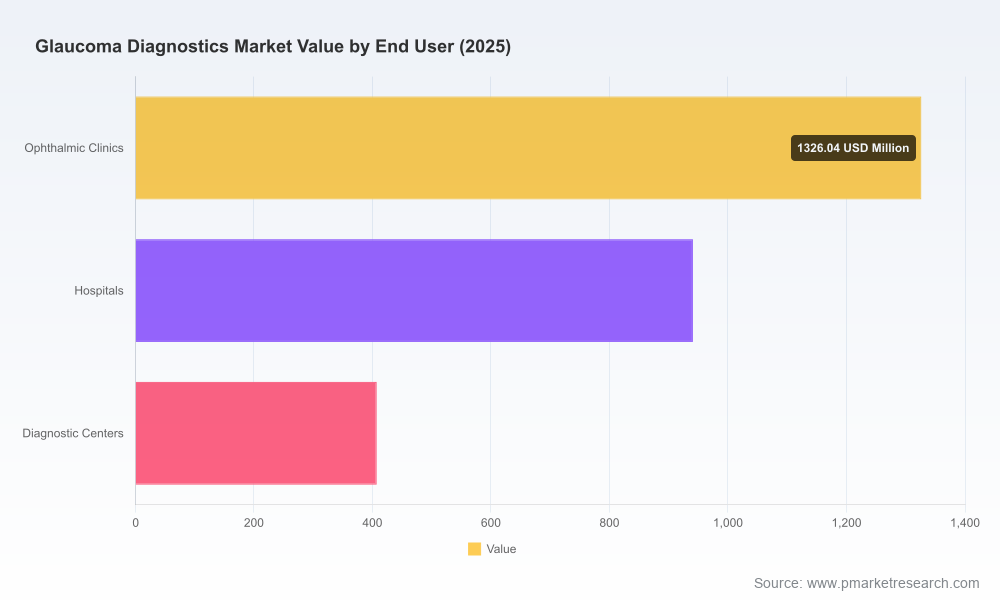

- Segment commercialization by endpoint and setting. Opportunities differ materially between high-acuity hospital deployments, specialist ophthalmic clinics, and the expanding home-monitoring market. Go-to-market models must reflect these operational differences rather than applying a one-size-fits-all sales playbook.

- M&A and partnership playbooks. Given the concentration profile and the high value placed on AI-enabled analytics, mid-market acquisitions that fill capability gaps (e.g., cloud analytics, home-monitoring devices, or focused software modules) are likely to deliver greater strategic ROI than incremental hardware extensions.

What the report contains — practical, executable modules

PW Consulting’s report is structured as a practitioner’s toolkit for 2026 decisions, not an academic exercise. Key inclusions:

Worldwide Glaucoma Diagnostics Market

- Market sizing and forecast models (historical 2020–2025 and forecast 2026–2032) with downloadable, scenario-ready spreadsheets that allow users to test assumptions on pricing, adoption rates and unit economics.

- Technology and clinical landscape analyses that compare optical coherence tomography, tonometry, perimetry, fundus imaging and emerging home-monitoring approaches — emphasizing clinical differentiators, integration risk, and total cost of ownership.

- Regulatory and reimbursement playbooks: country-by-country checkpoints, device classification impacts, typical submission timelines, and payer evidence requirements with tactical recommendations for dossier development.

- Commercial playbooks for hospitals, specialty clinics and diagnostic centers — including channel strategies, sales force sizing heuristics, and sample contracts that align with 2026 buying behaviors.

- Competitive profiling and M&A screening: strategic SWOTs for the major incumbents, recent product and corporate moves, plus an annotated list of sensible acquisition targets and partnership archetypes.

- Operational checklists for rolling out AI-enabled diagnostics securely and in compliance with clinical governance standards.

Competitive landscape — what incumbents are doing and why it matters

The market is populated by well-capitalized medical device leaders and a growing set of specialist entrants. Our competitive section profiles leading players across imaging, tonometry, perimetry and portable diagnostics, examining product roadmaps, channel strength, and R&D focus. Highlights include:

- Zeiss (Germany): Continues to invest in integrated OCT platforms and has recently expanded glaucoma analytics in its flagship OCT systems. Its focus on workflow integration positions it strongly where large clinic chains demand interoperability and longitudinal progression tools.

- Heidelberg Engineering (Germany): Strong in high-resolution OCT with dedicated glaucoma analysis modules and recent software releases that emphasize AI-based progression detection — a capability that increases the clinical stickiness of its installed base.

- Topcon (Japan): Moving aggressively on swept-source OCT and AI-enabled visual field analyzers, and its regulatory wins in 2025 demonstrate how clearance strategies can accelerate clinical adoption in major markets.

- Nidek and Reichert Technologies (Japan and USA): Both are strengthening tonometry and corneal biomechanical assessment offerings with connectivity and remote monitoring features that cater to outpatient and hybrid-care models.

- Haag-Streit, Canon Medical Systems and Kowa: Maintain durable positions across perimetry, tonometry and fundus imaging, with incremental innovation in usability and image quality rather than radical platform shifts.

- Carelon Medical Technologies and iCare: Representative of the agile innovators pushing into portable fundus imaging and home tonometry, respectively — segments that are catalyzing new care pathways and creating potential channel disruption.

Recent releases and regulatory milestones are illustrative. Notable corporate events over 2024–2025 include new OCT software releases incorporating AI-based progression detection, FDA 510(k) clearances for AI-enabled visual field analyzers, and clinical validation studies establishing home tonometry performance. These moves highlight an industry reorientation toward software-defined clinical value and patient-centric modalities.

Regulatory and reimbursement dynamics to watch in 2026

Regulatory classification and coding policies materially influence time-to-market and the economics of deployment. For example, in the U.S. non-contact tonometers fall under Class II with 510(k) requirements, and reimbursement is influenced by specific CPT codes that determine per-procedure reimbursement levels in clinical practice. Internationally, device labelling, software-as-a-medical-device (SaMD) regulations, and national reimbursement frameworks present divergent pathways that must be planned for in product and partnership strategies.

Risk and mitigation framework

- Regulatory headwinds: Mitigate by investing in early regulatory intelligence and modular clinical evidence packages that can be adapted to multiple jurisdictions.

- Reimbursement uncertainty: Build health-economic dossiers demonstrating improved diagnostic accuracy, downstream cost-savings, or avoided vision loss to accelerate payer acceptance.

- Channel disruption from low-cost entrants: Differentiate on workflow integration, longitudinal analytics and service contracts — not just on device specs.

- Data governance and cybersecurity: Implement HIPAA/GDPR-aligned architectures and transparent AI explainability to reduce deployment friction with health systems.

How PW Consulting’s methodologies add value

Our forecasting blends market transaction data with clinic-level adoption kinetics and device life-cycle analysis. We stress-test scenarios — conservative, base, and upside — and provide sensitivity models to help executives quantify returns on R&D and commercial investments in 2026. Importantly, while this preview shares high-level directional findings, the full report contains the granular worksheets, appendices, and validated vendor models necessary to operationalize decisions.

Next steps for executives

- Use our interactive forecast tools to prioritize the top two product/market combinations that should receive capital allocation in 2026.

- Align regulatory, clinical evidence and reimbursement strategies before committing to large-scale manufacturing or distribution agreements.

- Consider bolt-on acquisitions or partnerships for analytics capabilities if your current roadmap lacks AI-enabled progression detection or cloud-based longitudinal reporting.

- Deploy pilot programs in a mix of hospital and clinic settings to validate unit economics and collect real-world evidence for payer discussions.

PW Consulting’s Worldwide Glaucoma Diagnostics Market report gives C-suite and strategy teams the evidence-packed foundation they need to set 2026 priorities: where to invest, partner, and divest. For access to proprietary segmentation tables, scenario spreadsheets, company scorecards and the full competitive database — including the annexes that map regulatory pathways and CPT-code economics — please consult the complete report.

For detailed analysis of this topic, please visit the official page:Worldwide Glaucoma Diagnostics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com