Worldwide Atmospheric Water Generator Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I am pleased to present an executive briefing accompanying our latest market research: Worldwide Atmospheric Water Generator (AWG) Market — 2026 Outlook and Strategic Playbook. This report translates a fast‑evolving technology opportunity into concrete, executable guidance for corporate decision‑makers preparing strategies, investments, and field deployments in 2026 and beyond.

Worldwide Atmospheric Water Generator Market

Macro view: A market maturing at scale

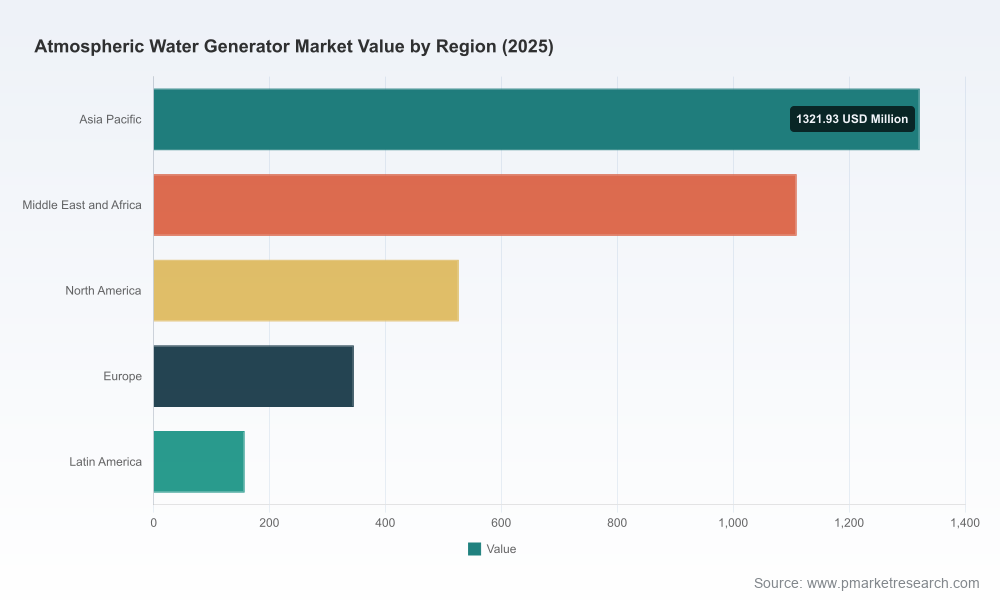

Between 2020 and 2025 the AWG market transitioned from an emerging niche to a commercially validated category. Our base‑year analysis shows the industry expanding from just over USD 1.5 billion in 2020 to roughly USD 3.46 billion in 2025. Under our central forecast, the market is expected to sustain robust expansion through the 2026–2032 forecast horizon, rising to an estimated USD 10.48 billion by 2032 at a compound annual growth rate (CAGR) of approximately 17.15%.

Worldwide Atmospheric Water Generator Market

For executives, those topline dynamics matter: they signal a window in which first mover advantages, supply‑chain positioning, and scale economies can meaningfully influence profitability and market share. The pace of growth also means that 2026 is not merely another planning year — it is a strategic inflection point for firms targeting water security, off‑grid solutions, or sustainable utilities provisioning.

Worldwide Atmospheric Water Generator Market

Why this report matters to 2026 decision cycles

- Investment prioritization. With a high‑growth trajectory established, capital allocation choices made in 2026 will determine whether organizations capture premium margins or become price takers as capacity scales. Our report models multiple investment scenarios (conservative, base, aggressive) that translate forecast trajectories into NPV and IRR sensitivities for factory expansion, R&D programs, and channel development.

- Go‑to‑market and channel design. AWG solutions span residential point‑of‑use units to multi‑kiloliter/day industrial systems. We provide decision frameworks that align product archetypes with go‑to‑market channels (OEM, distributor, project EPC, direct to end user), pricing architectures, and service models — enabling faster route‑to‑revenue with reduced customer acquisition cost.

- Operational readiness. Procurement, manufacturing localization and aftermarket services are critical in a market where reliability and certification determine adoption. The report includes practical checklists for supplier due diligence, manufacturing footprint tradeoffs, and spare‑parts logistics to minimize downtime in deployed assets.

- Regulatory and risk management. AWG adoption is tightly coupled to water quality standards and local potable water certifications. We translate the regulatory backdrop and recent policy moves into a compliance playbook that helps product teams pre‑qualify markets and avoid costly rework or market access delays.

What the report contains — practical, actionable deliverables

- Integrated market sizing and scenario models (2020–2032) with transparent assumptions and sensitivity analyses to stress‑test strategic choices under different climate, energy, and cost curves.

- Commercial deployment playbooks: procurement checklists, installation best practices, maintenance and SLA design templates, and financing/leasing structures tailored to municipal, commercial and industrial buyers.

- Technology evaluation frameworks to compare condensation, desiccant, and solar‑hydropanel approaches across efficiency, capex/O&M profiles, and climate suitability — plus a vendor scorecard methodology you can apply to tenders.

- Case studies and pilot templates: how to design and scale pilots, measure performance (kL/day, energy per litre, water quality), and move from demonstration to commercial roll‑out.

- Commercial due diligence materials: competitor benchmarking, supplier risk matrices, and M&A screening criteria for rapid transaction execution.

Competitive landscape — leaders, challengers, and the structure of competition

The AWG market exhibits moderate concentration. Our concentration metrics show that the top three players account for a meaningful share of the market, and the top five consolidate more than half of industry capacity. That structure creates opportunities for both incumbents to leverage scale and for agile challengers to differentiate through vertical integration, specialized technology, or service excellence.

Key companies profiled in our analysis include global and regional players across multiple value propositions:

- Watergen Ltd. (Israel) — A technology pioneer that has demonstrated diversified applications from residential to vehicle‑integrated systems; notable for its patented GENius platform and expanding partnerships that move AWG into mobility and institutional use. (https://www.watergen.com/)

- GENAQ Technologies S.L. (Spain) — Focused on high‑efficiency industrial and commercial solutions with HVAC‑derived engineering and certifications for off‑grid deployments. (https://genaq.com/)

- SOURCE Global (formerly Zero Mass Water) (United States) — Specializes in solar hydropanel approaches for decentralized potable water, an important reference design for sunny, off‑grid contexts.

- ACCair / FUJIAN WANJUAN TECHNOLOGY CO.,LTD (China) — Commercial and industrial provider with emphasis on large‑scale outputs. (https://www.accairwater.com/)

- Quench Innovations (United States) — Integrates AWG with point‑of‑use systems and consumer channels. (https://www.quenchinnovations.com/)

- Other notable players include regionally focused manufacturers and integrators — from high‑efficiency industrial OEMs to solar‑integrated residential suppliers and community‑scale social enterprises.

Our competitive assessment evaluates companies on technology maturity, manufacturing scale, service network, certification footprint, and route‑to‑market sophistication. The full vendor matrix in the report provides procurement teams with a rapid shortlisting tool calibrated for technical KPIs and commercial constraints.

Recent developments shaping 2026 strategy

- Academic and field testing continues to validate system resilience: a January 2026 installation at the University of North Florida is supporting performance testing tied to water‑infrastructure resilience initiatives.

- Product innovation is accelerating: 2024–2025 witnessed several launches of compact consumer units and higher‑capacity Series‑scale models with IoT monitoring, thermodynamic upgrades, and intelligent mineralization; a March 2025 Series 2.0 launch demonstrated scalable outputs up to multiple thousands of litres per day with advanced monitoring.

- Policy and partnership dynamics are shaping adoption: national incentives and subsidy frameworks (for example, policy announcements supporting rural decentralized AWG installations) are lowering economic barriers and are prime signals for prioritizing market entry or expansion.

- Corporate partnerships continue to broaden use cases: integrations into electric vehicle ecosystems and industrial sustainability programs are creating adjacent demand channels beyond traditional municipal procurement.

Strategic recommendations for 2026

- Prioritize hybrid commercialization pilots. Move beyond lab demos. Combine product pilots with financing trials, bundled energy solutions (solar + AWG), and local maintenance partnerships to prove total cost of ownership and user acceptance in target micro‑markets.

- Invest in certification and water quality validation up front. Given regulatory gatekeeping, early investment in potable water certifications and third‑party testing shortens sales cycles and reduces retrofit costs.

- Design for serviceability. Product design choices that optimize modularity, remote diagnostics, and spare part commonality reduce long‑term O&M burdens — a decisive advantage in large tenders and public‑sector contracts.

- Use procurement scorecards and scenario pricing. Our models show that small shifts in energy efficiency or service pricing materially change ROI under realistic climate and electricity price trajectories. Implement vendor scorecards tied to life‑cycle cost metrics, not just capex.

- Consider localized manufacturing or assembly. Tariffs, logistics, and the need for rapid service response make local assembly hubs attractive in many markets; the exact footprint depends on volume forecasts and duty regimes which the full report helps to model.

- Build partnerships across energy, mobility, and humanitarian channels. AWG adoption is often catalytic when bundled — e.g., integrated into vehicles, paired with solar microgrids, or deployed as emergency water generation in humanitarian relief — creating diversified revenue streams.

What we deliberately withhold here — and why you should download the full report

In keeping with a “trailer” approach, this brief demonstrates the analytical depth and strategic utility of our work while withholding detailed segmentation tables, country‑level forecasts, vendor scorecards, and full financial models. These assets are included in the complete report and are designed for immediate operational use by business development, procurement, and corporate strategy teams planning 2026 initiatives.

Specifically, the full deliverable contains: interactive forecast spreadsheets, prioritized market entry matrices, full vendor benchmarking with KPI weights, sample tender documents, and executable pilot‑to‑scale playbooks. If you are preparing capital allocations, R&D roadmaps, or market entry plans for 2026, those materials will materially shorten decision cycles and reduce execution risk.

Concluding perspective

The AWG market in 2026 is no longer a speculative frontier; it is a strategic terrain where product architecture, service models, and route‑to‑market discipline determine winners. With a market expanding at roughly a mid‑teen CAGR and a multi‑billion dollar ceiling within this decade, companies that combine technological differentiation with disciplined commercial execution will capture disproportionate value.

PW Consulting’s Worldwide Atmospheric Water Generator Market report is built to be immediately actionable: to map scenarios into budget cycles, to reduce procurement friction, and to convert pilots into repeatable revenue streams. For teams preparing decisions in 2026, the choice is between informed, model‑driven bets and reactive posture. We recommend the former.

To access the full report, vendor matrices, and downloadable forecast models, visit PW Consulting’s research portal or contact our industry practice team for a private briefing tailored to your organization’s priorities.

For detailed analysis of this topic, please visit the official page:Worldwide Atmospheric Water Generator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com