Worldwide Oil Hose Market 2026 Outlook: Strategic Imperatives for Resilient Growth

Executive summary

As PW Consulting’s senior strategic advisor and chief industry analyst, I present a forward-looking synthesis drawn from our latest Worldwide Oil Hose Market report (base year 2025). The sector is at an inflection point: entrenched industrial demand and offshore activity underpin mid-term growth, yet material cost volatility, evolving standards, and a fragmented supplier landscape require decisive managerial action in 2026. Our report quantifies the market and models realistic scenarios; headline metrics show the industry rising from approximately USD 3.1 billion in 2020 to USD 3.93 billion in 2025, with a compound annual growth rate of 4.8% projected through 2032, reaching roughly USD 5.45 billion. Notably, a near-term softening is visible in 2026 before the market reaccelerates—an inflection that should shape corporate budgets, procurement strategies, and product roadmaps for the year ahead.

Worldwide Oil Hose Market

Why this matters for 2026 decision-makers

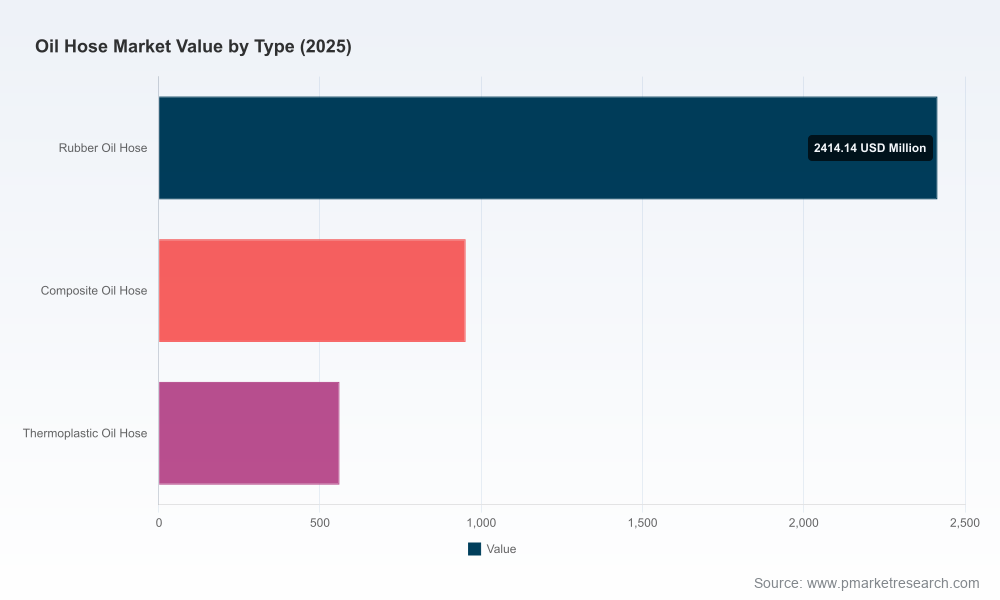

- Capital allocation and product strategy: The projected steady expansion (CAGR ~4.8%) validates continued investment in differentiated hose technologies (composite and thermoplastic solutions, lightweight reinforced systems). However, the transient 2026 dip introduces a need to sequence capex and prioritize initiatives with shorter payback and higher margin resilience.

- Procurement and cost management: Raw material cost shocks—most prominently synthetic rubber and nitrile compounds—have materially altered input cost curves. Procurement teams must combine tactical spot coverage with strategic sourcing, hedging and supplier partnership models to protect margins.

- Regulatory & specification compliance: Offshore and fuel-transfer applications demand adherence to stringent standards (EN series, API, OCIMF, and sector-specific fuel delivery norms). Compliance is now a competitive differentiator that affects contract eligibility and total cost of ownership.

- Commercial & route-to-market choices: With market concentration remaining limited (top-three players account for roughly one-fifth of market share and top-five for about one-third), there is room for scale-up through focused consolidation or by winning niche OEM and aftermarket channels.

Market dynamics shaping strategies in 2026

Three forces will dominate the strategic landscape next year:

Worldwide Oil Hose Market

- Input price volatility: Recent data show sharp increases in synthetic rubber benchmarks and notable upticks in nitrile rubber pricing in major markets. These trends compress margins for unprotected manufacturers and accelerate substitution considerations (materials science, polymer blends, and alternative reinforcements).

- Standards and safety-driven demand: End-users—particularly in offshore, marine bunkering, and industrial transfer systems—are increasingly prioritizing hoses that meet rigorous chemical, abrasion and fire-resistance standards. Certification timelines, testing capacity, and traceability will be central commercial gating items.

- Service and lifecycle economics: Buyers are more frequently evaluating total lifecycle cost over purchase price. Predictive maintenance services, certification bundles, and warranty-backed replacement programs unlock premium pricing and recurring revenue.

What the report provides — a practical toolkit, not a rehash

Our Worldwide Oil Hose Market report delivers actionable intelligence designed for executives, procurement leads, and business development teams considering near-term moves in 2026. Key deliverables include:

Worldwide Oil Hose Market

- Demand-supply scenarios and stress-tested forecasts calibrated to 2026 budget cycles, including upside and downside cases tied to commodity oscillations and offshore project timing.

- Supplier scorecards and capability matrices that grade manufacturers on technical breadth, quality systems, production footprint resilience, and aftermarket capability.

- Commercial playbooks for pricing strategy under input-cost inflation, with recommended contract clauses, indexation mechanisms, and channel incentives to stabilize margins.

- Procurement and inventory stress tests, including recommended hedge ratios, dual-sourcing frameworks, and nearshoring assessments to reduce exposure to single-source shocks.

- Regulatory compliance checklists and a roadmap for achieving and marketing certifications relevant to fuel, mineral oil, and offshore transfer applications.

- Acquisition screening criteria and valuation models tailored to both strategic buyers seeking technology or geographic fill and financial sponsors aiming for roll-up plays.

Competitive landscape — strategic implications for suppliers and buyers

The oil hose industry remains fragmented with a mix of multinational OEMs and specialized regional manufacturers. Our competitive analysis highlights several archetypes and the strategic moves most likely to win in 2026:

- Global diversified industrial players (e.g., Parker Hannifin, Eaton, Gates): These incumbents leverage broad channel networks, integrated engineering services, and established OEM relationships. Their advantage lies in system-level selling and the ability to absorb short-term cost pressure through scale. For them, the strategic play in 2026 is to accelerate aftermarket service bundling and to push higher-margin engineered solutions into oil & gas accounts.

- Specialist hose manufacturers (e.g., Manuli Hydraulics, Alfagomma, Transfer Oil): Specialists win on technical depth and standard-compliant product lines. Their opportunity is to monetize certification expertise and customized assemblies for offshore and refineries. Priorities should include capacity flexibility and closer raw-material partnerships to buffer price swings.

- Advanced material and composite players (e.g., Trelleborg, Continental/ContiTech): These firms differentiate through material science and bespoke marine/offshore solutions. In 2026, investing in R&D to reduce dependence on price-volatile rubbers, and in testing to accelerate time-to-certification, will be decisive.

- Regional champions and niche producers (e.g., RYCO, NRP Jones, Cavmac, select Chinese manufacturers): Their strengths are proximity to local demand, short lead times, and competitive pricing. To scale, they must formalize quality systems, seek international approvals, and explore partnership models that export their manufacturing cost advantage without compromising standards.

Risks, mitigants and strategic options for 2026

Our risk assessment and recommended mitigants for 2026 focus on three domains:

- Cost and supply risk: Mitigants include multi-year supply contracts with indexation, strategic inventory buffers for critical polymer inputs, joint procurement consortia across non-competing buyers, and early testing of polymer alternatives to diversify dependence.

- Regulatory and certification risk: Actions include accelerating third-party testing, pre-qualifying manufacturing lines under key standards, and embedding certification deliverables into sales contracts to reduce time-to-deal.

- Commercial and market risk: Firms should rebalance revenue mixes toward aftermarket services and long-term maintenance contracts, develop flexible pricing models for large OEMs, and pursue selective M&A to acquire certification, distribution, or material science capabilities.

Recommendations for executive teams

- Recalibrate 2026 CAPEX: prioritize projects with payback under 36 months and those that de-risk supply continuity (e.g., secondary manufacturing lines, facility certifications).

- Lock in a portion of polymer spend via multi-year arrangements while maintaining tactical spot exposure to capture downcycles; evaluate financing structures that smooth procurement cost swings.

- Double down on lifecycle offerings: warranty-enhanced sales, predictive replacement services, and digital traceability tied to certification data to capture recurring revenue.

- For acquirers: target bolt-on specialists that add certification capability, expand proven offshore product portfolios, or provide manufacturing flexibility in lower-cost geographies.

- Institute an early-warning dashboard (commodity indices, order-book velocity, standards revision trackers) to inform rolling forecasts and trigger prescriptive playbooks.

What we did — and what we did not disclose

Our analysis synthesizes company disclosures, standards documentation, proprietary supply-chain mapping and primary interviews. To preserve the report’s commercial value and to adhere to our "trailer" principle, this release intentionally omits the granular regional and end-use splits, detailed price elasticity models, and the full ranked supplier scorecards. These are included in the full PW Consulting report and are essential for transaction diligence, bid-pricing, and procurement tender design.

Next steps

For executive teams planning 2026 strategies, the immediate actions are clear: stress-test 2026 budgets against the material-price scenarios we outline, lock in critical polymer supply, and prioritize certification-led product initiatives that enable premium positioning. PW Consulting’s full report contains the operational playbooks, supplier matrices, and scenario models necessary to execute these moves with confidence.

To engage our team for a tailored briefing—where we can walk your leadership through the forecast sensitivities, supplier opportunities, and a 90-day implementation roadmap—visit the PW Consulting Worldwide Oil Hose Market report page or contact our industry practice lead. The window to convert 2026 volatility into competitive advantage is limited; timely, informed action will separate winners from the rest.

For detailed analysis of this topic, please visit the official page:Worldwide Oil Hose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com