Asia-Pacific Solid Phase Extraction Market Size, Share, Current Trends, and Forecast by 2033

Other |

2026-06-25 13:15:24

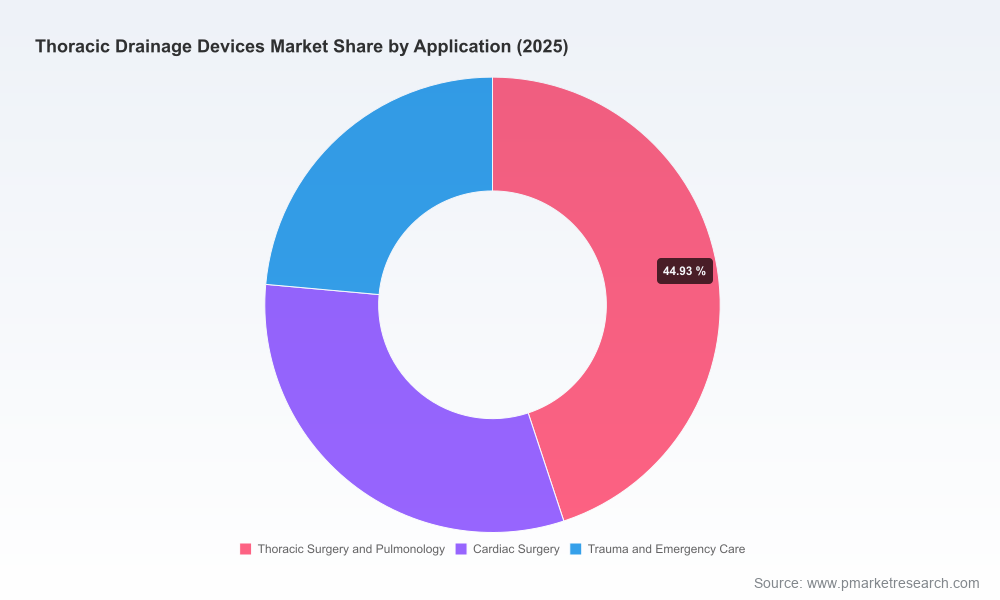

As healthcare systems recalibrate after the pandemic-era surge in procedural volumes and technology adoption, thoracic drainage devices are re-emerging as a focused area of clinical and commercial competition. PW Consulting’s latest market study — anchored on a 2025 base year and a 2026–2032 forecast horizon — quantifies a clear growth trajectory: the global thoracic drainage devices market is projected to continue expanding at a compound annual growth rate (CAGR) of 6.48% through 2032. This brief synthesizes the report’s strategic implications for executive teams preparing 2026 plans, while intentionally withholding proprietary breakdowns to encourage full-report engagement.

Worldwide Thoracic Drainage Devices Market

Predictable macro growth: A stable mid-single-digit CAGR provides a reliable backdrop for capital allocation, portfolio prioritization, and long-range revenue modeling. For manufacturers and medical device investors, the forecast supports measured expansion rather than speculative, high-risk bets.

Worldwide Thoracic Drainage Devices Market

Structural change points: The market is at the intersection of product innovation (digital drainage and intelligent monitoring), procurement consolidation in hospital systems, and tightening regulatory and reimbursement expectations. Each of these vectors materially affects product development roadmaps, go-to-market tactics, and partnership strategies for 2026.

Worldwide Thoracic Drainage Devices Market

Clinical and operational drivers: Shorter lengths of stay, emphasis on enhanced recovery after surgery (ERAS), and the drive for ambulatory and wearable solutions are reshaping demand profiles. Devices that demonstrably reduce hospital resource use while supporting mobility and objective leak measurement are positioned to capture premium pricing and adoption.

Actionable market model: A transparent, audit-ready revenue model covering historical 2020–2025 dynamics and bottom‑up forecasts for 2026–2032. The model supports sensitivity testing across adoption scenarios, reimbursement shifts, and pricing changes.

Go-to-market playbooks: Tailored playbooks for incumbent OEMs, new entrants, and contract manufacturers — including channel mix options, hospital procurement tactics, and value-based selling scripts that reflect current HCP priorities.

Regulatory & reimbursement roadmaps: Practical guidance on navigating the dominant Class II 510(k) pathway in the U.S., electrical safety and performance expectations for digital systems, and implications of procedure coding (e.g., CPT references) for hospital reimbursement strategies.

Technology and clinical evidence matrix: Evaluation of digital drainage systems, monitoring capabilities (objective air-leak quantification), and wearable/mobile formats — plus a prioritized list of clinical endpoint evidence needed to accelerate adoption in cardiothoracic and thoracic surgical pathways.

Competitive and M&A decision tools: Profiles and strategic positioning of leading players, an M&A filter for target selection (technology, geography, channel synergies), and post‑merger integration blueprints tailored to thoracic drainage portfolios.

Risk & supply chain heatmap: Tactical mitigations for product discontinuations, recalls, single-source components, and manufacturing bottlenecks that can derail 2026 commercialization plans.

The market exhibits moderate concentration — the three largest competitors account for a notable portion of global sales, while the top five capture a clear majority of market revenues. This structure favors scale players for hospital procurement negotiations and distribution reach, but it also creates a fertile opportunity for innovators that can demonstrate distinctive clinical and operational value.

Key strategic forces shaping the competitive landscape:

Incumbent defensive moves: Large healthcare OEMs maintain broad critical‑care portfolios that include chest tubes and drainage systems. Their distribution strength and hospital relationships continue to be a barrier to entry for pure-play newcomers.

Product rationalization and exit risk: Commercial shifts by established suppliers — including announced discontinuations and subsequent regulatory events — materially alter local supply footprints and create openings for competitors and contract manufacturers to fill unmet demand quickly.

Digital disruption: Providers of digital drainage and monitoring platforms that offer objective air-leak quantification and mobility advantages are gaining traction. These systems enable data capture over the perioperative period and support telemonitoring workflows — a differentiator for progressive hospital systems.

Evidence-driven procurement: Hospitals increasingly require outcomes and cost-avoidance data (reduced LOS, fewer complications) to approve premium devices. Firms that invest in pragmatic clinical trials and real-world evidence can command better contracting terms.

Our review of recent company-level activity highlights the interplay of product strategy, regulatory management, and market access:

Portfolio shifts create immediate market consequences: A notable incumbent announced the commercial discontinuation of certain chest drainage product lines in the U.S. and later faced recall activity. These developments illustrate how supplier exits and compliance events can rapidly reallocate hospital demand and force buyers to requalify alternate sources.

Digital entrants gaining regulatory foothold: Smaller, technology‑focused firms secured regulatory clearances for drainage monitoring technologies, signaling that the 510(k) pathway remains the primary route for innovations in this space.

Market visibility for regional innovators: Trade show participation and targeted launches by regional manufacturers are expanding the pool of viable suppliers, particularly for ambulatory and portable drain solutions.

Executives who position their organizations with the following priorities will be best prepared to capture value from the market’s steady growth and structural shifts.

For OEMs and product leaders – prioritize digital differentiation: Fast‑track modular digital drainage platforms that provide objective air-leak measurement and integration with hospital EMRs. Bundle device sales with services (analytics, remote monitoring) to convert discrete transactions into recurring revenue streams.

For supply chain and operations leaders – develop contingency sourcing: Build dual-sourcing strategies for critical disposables, maintain validated alternative suppliers, and model inventory buffers to insulate key hospital customers against abrupt product exits or recalls.

For commercial teams – evolve contracting to outcomes: Create contracts that tie pricing to measurable operational outcomes (e.g., reduced LOS, readmission rates). Prepare reference-case studies that quantify savings in direct hospital costs to support premium positioning.

For R&D and clinical affairs – invest in pragmatic evidence: Deploy lean clinical evaluation frameworks to generate the minimum high-impact evidence that hospital procurement committees require. Prioritize endpoints that matter to both surgeons and perioperative administrators.

For investors and M&A planners – target complementary tech and channel plays: Prioritize acquisitions that add digital monitoring, ambulatory/wearable capability, or direct distribution access to large hospital systems. Use our M&A filters to accelerate target shortlisting.

Thoracic drainage devices remain predominantly regulated as Class II devices in mature markets, with the FDA 510(k) pathway as the typical regulatory route in the United States. Digital and electrically powered systems must also meet applicable electrical safety and performance consensus standards. On the reimbursement front, thoracic procedures that require chest tube insertion continue to be coded under established surgical CPT and DRG frameworks — an important factor when modeling hospital adoption and total cost of care impacts.

Executive planning: Integrate the report’s revenue model and scenario analyses into your FY26 budgeting cycle to stress-test product launch assumptions and channel investments.

Portfolio prioritization: Use the technical and clinical evidence matrix to rank product investments for accelerated development or rationalization.

Commercial sequencing: Leverage the competitive playbooks to map prioritized geographies, hospital cluster targets, and pricing strategies that align with procurement behavior.

M&A and partnerships: Apply the M&A decision tools to identify targets that fill capability gaps (digital monitoring, ambulatory drains) or broaden distribution access following competitor exits.

The thoracic drainage devices market presents a steady and investment-worthy growth profile through 2032, underpinned by technology-enabled clinical improvements and shifting care pathways. However, the path to market leadership will depend less on market size alone and more on disciplined execution: product differentiation through digital capabilities, rigorous clinical value demonstration, resilient supply chains, and strategies that translate clinical benefit into hospital-level cost savings.

PW Consulting’s full Worldwide Thoracic Drainage Devices Market report provides the detailed models, competitive profiles, regulatory playbooks, and executable commercial strategies that will inform confident 2026 decision-making. For decision-makers who need the granular inputs and scenario-specific recommendations, the full report and downloadable model are available on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Worldwide Thoracic Drainage Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com