Worldwide Janus Kinase (JAK) Inhibitors Market: Strategic Outlook for 2026 Decision‑Makers

As JAK inhibitors evolve from a specialized therapeutic class into a mainstream category across immunology and hematology, commercial stakes for 2026 are high and decisions made this year will disproportionately determine market positions through the end of the decade. PW Consulting’s latest market study—anchored on a 2025 base year—projects the global JAK inhibitors market to grow from a 2025 base of USD 16,200.0 Million to USD 40,565.2 Million by 2032, at a compound annual growth rate (CAGR) of 14.01% over the 2026–2032 forecast window. This growth trajectory presents both aggressive upside and structural headwinds; our report is designed to translate that macro view into executable choices for biopharma leadership, corporate development, and market-access teams.

Worldwide Janus Kinase (JAK) Inhibitors Market

Why the 2026 Inflection Matters

- Strong, sustained growth: A double‑digit CAGR signals large addressable opportunity, but also intensifying competition for therapeutic niches and label expansions.

- Concentrated supplier structure: The market is meaningfully concentrated—top three players control the majority share and the top five are dominant—creating asymmetric power dynamics for entrants and partners.

- Regulatory and safety dynamics: A class-level boxed warning introduced in 2021 continues to shape prescribing behavior, payer scrutiny, and post‑market evidence requirements globally.

- Intellectual property and product lifecycle timing: Key patent expiries and label extension activity compress incumbent windows of exclusivity, making 2026 a pivotal planning year for lifecycle defence, generics mitigation, and value capture strategies.

- Supply‑chain fragility: API constraints and supplier concentration observed in recent years mean procurement and manufacturing contingencies are now strategic necessities.

What PW Consulting’s Report Delivers

This report is intentionally tactical—built for leaders who must convert market intelligence into swift, high‑confidence action. It includes:

Worldwide Janus Kinase (JAK) Inhibitors Market

- Top‑down and bottom‑up market sizing and a seven‑year forecast model (USD Million basis) with scenario toggles for safety‑driven demand shocks, generic entry, and accelerated label uptake.

- Concentration analysis and competitive benchmarking that reveal how incumbent and challenger strategies are shifting market structure.

- Regulatory and reimbursement playbooks detailing likely payer responses, contracting levers, and CMS implications for the U.S. market.

- Actionable launch and life‑cycle playbooks focused on pediatric label expansion, formulation diversification, and real‑world evidence (RWE) generation to mitigate safety concerns.

- Supply‑chain risk matrix with mitigation checklists, dual‑sourcing options, and contract templates to secure API continuity.

- Commercial scenarios and an M&A/partnering prioritization framework tuned to valuation sensitivity from 2026 onward.

- Executive dashboards, slide decks, and a customizable financial model for board‑level decision briefings.

Competitive Landscape: Who Matters and Why

The competitive map is dominated by a small number of large global biopharma companies that have already embedded JAK inhibitors into broad therapeutic portfolios. Several patterns merit attention:

Worldwide Janus Kinase (JAK) Inhibitors Market

- Incumbent incumbency through label breadth: Major players have pursued label expansions into pediatric populations, dermatologic indications, and multiple inflammatory diseases—actions that extend commercial life and create barriers to entry for more selective or niche molecules.

- New formulations and administration routes: Companies are diversifying beyond oral small molecules to topical and alternative formulations to capture adjacent patient segments and differentiate on tolerability and convenience.

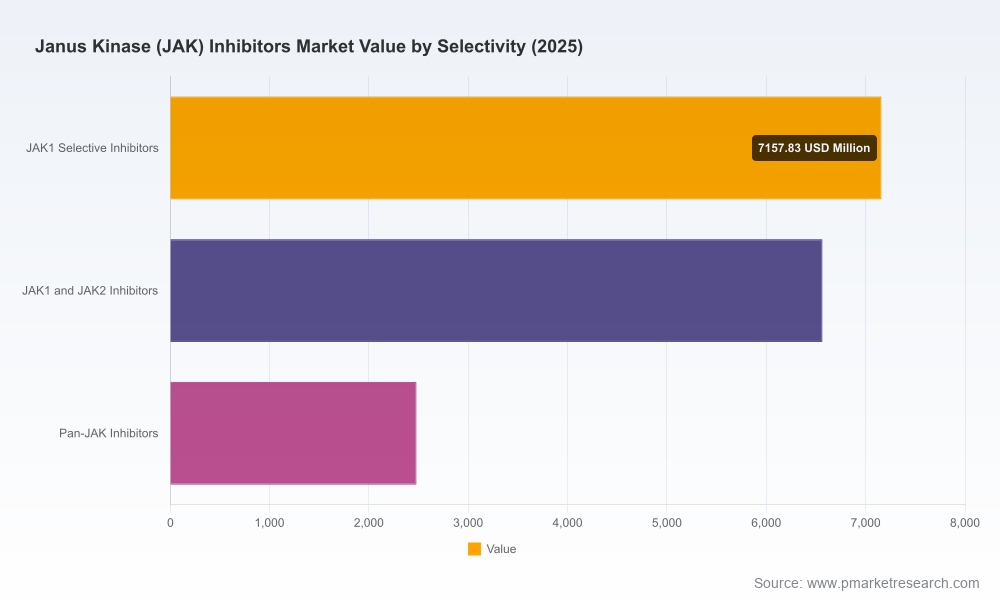

- Pipeline and differentiation: Selectivity—whether JAK1, JAK2, or pan‑JAK—remains a central scientific thesis for differentiation. Late‑stage pipeline activity and novel combinations with other immune targets will define next wave competitive dynamics.

- Partnerships and regional strategies: Strategic alliances, licensing agreements, and regional co‑commercialization remain primary routes to accelerate access in complex markets and to share post‑launch RWE burdens.

Notable company actions in the recent 18–24 months underline these trends: several companies secured label expansions and new approvals in 2024 across pediatric and dermatologic indications; others continue to advance differentiated molecules through clinical development. At the same time, the classwide boxed warning remains a factor that shapes labeling strategy, marketing messages, and payer negotiation tactics.

Regulatory, IP and Access Events That Will Shape 2026

- Class safety communications and boxed warnings have elevated the evidentiary bar for broad use. Expect payers to insist on stratified access and step edits in the near term.

- High‑impact patent expirations on marquee products are approaching, compressing monopoly windows and catalyzing generic and biosimilar planning. Companies must decide now whether to invest in life‑cycle measures or pivot to next‑generation assets.

- Public payers in major markets are clarifying coverage rules for inflammatory indications, creating both access opportunities and price pressure for manufacturers.

- API and raw material sourcing risks observed recently continue to warrant preemptive supply‑chain investments to avoid launch disruptions or shortage‑related revenue impact.

Strategic Imperatives for 2026

To convert market growth into lasting leadership, PW Consulting recommends five priority tracks for 2026:

- Optimize portfolio mix now: Prioritize assets by commercial window, safety profile, and ease of label expansion. For incumbents with imminent patent expiries, allocate budget to life‑cycle strategies that are cost‑efficient and evidence‑heavy (e.g., pediatric studies, formulation switches).

- Differentiate on evidence and positioning: Invest in head‑to‑head and RWE studies that address safety concerns and define patient subsets where benefit:risk is superior. Use this evidence to negotiate favorable formulary positions and value‑based contracts.

- Secure manufacturing and raw materials: Implement dual‑sourcing and long‑term API contracts; consider regional production to lower logistics risk and accelerate supply resilience.

- Design payer‑centric launches: Align early with payers—particularly in systems that influence large shares of volume—to define outcomes metrics, coverage pathways, and co‑payment support structures before launch.

- Prepare for consolidation and partnerships: Use 2026 as a window for opportunistic M&A and licensing to capture near‑term growth opportunities and to access complementary modalities (e.g., topical formulations, combination therapies).

90‑Day Playbook for Executives

For companies that need to move quickly, the report includes a sequenced 90‑day plan designed to translate insight into deliverables:

- Days 1–30: Run rapid scenario simulations using the report’s financial model; conduct a patent‑expiry stress test and supply‑chain vulnerability scan.

- Days 31–60: Finalize go‑to‑market playbook for prioritized indication(s); initiate payer dialogue and map key RWE endpoints to formulary requirements.

- Days 61–90: Close manufacturing contingency agreements and evaluate M&A targets or licensing partners identified by our prioritization framework; present board‑level recommendations backed by our dashboard and risk matrix.

Why PW Consulting’s Analysis Is Different

We combine granular commercial calibration with scenario‑based stress testing: our primary model reconciles historical sales patterns with clinical reads, regulatory events, and payer policy shifts to produce actionable forecasts. The deliverables are not just numbers—but decision tools: contract playbooks, negotiation scripts, RWE study designs, and a prioritized action list for near‑term capital deployment.

Next Steps and Access

This commentary is a strategic preview. The full PW Consulting Worldwide JAK Inhibitors Market report contains proprietary segment detail, regional and indication heatmaps, and a downloadable financial model that underpins our scenarios. Those core segmentation tables and payer‑level intelligence are intentionally reserved for report subscribers and bespoke client engagements.

For leadership teams preparing 2026 budgets, commercial launch plans, M&A diligence, or regulatory strategies, the report is a practical toolkit to accelerate decision timelines and reduce execution risk. Contact PW Consulting to schedule a private briefing, request licensing of the model, or commission a tailored workshop to apply the study’s findings to your portfolio.

For detailed analysis of this topic, please visit the official page:Worldwide Janus Kinase (JAK) Inhibitors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com