Worldwide Narrow Body Aircraft MRO Market — Strategic Preview for 2026 Decision-Making

Executive teaser from PW Consulting

The Worldwide Narrow Body Aircraft MRO Market Report (base year 2025) furnishes the tactical and financial intelligence executive teams need to make high‑conviction decisions in 2026. Our analysis models the market across a six‑year historical window (2020–2025) and provides a seven‑year forecast horizon (2026–2032), projecting the market to expand at a compound annual growth rate (CAGR) of 5.6%—from USD 55,241.42 Million in 2025 to USD 80,893.25 Million by 2032. This briefing highlights why that trajectory matters, where boardrooms should focus scarce capital and managerial attention, and how the full report converts those observations into executable initiatives. Note: detailed segment and regional splits are intentionally withheld in this preview; the full report contains the granular tables, models and scenario outputs required for transaction‑level decisions.

Worldwide Narrow Body Aircraft MRO Market

Why narrow‑body MRO is the corporate priority in 2026

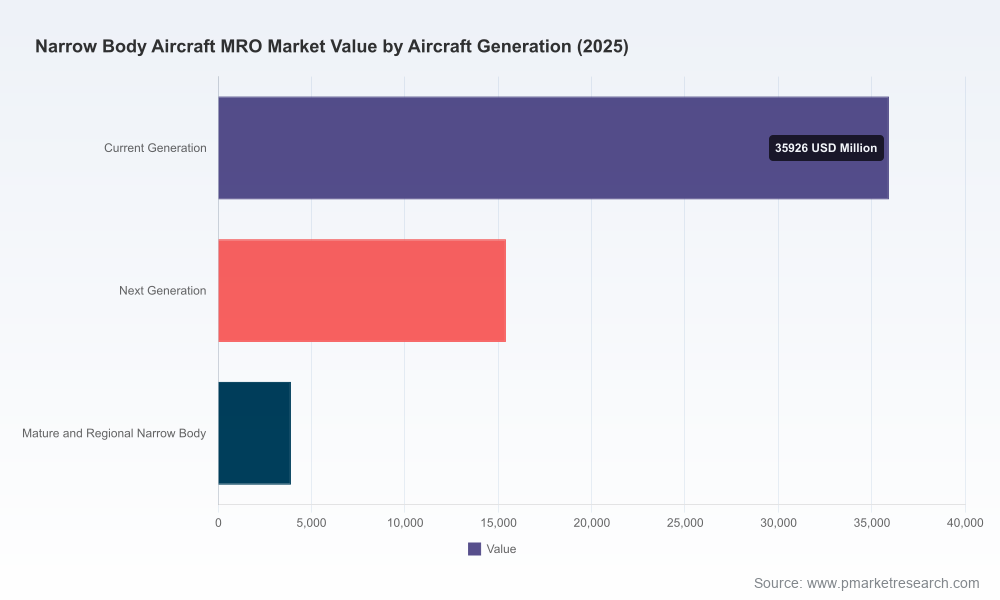

- Operational exposure: Narrow‑body fleets continue to underpin short‑haul networks globally, generating the highest frequency of recurring shop visits and discrete component events. The predictable cadence of these events creates both revenue certainty for MROs and cost volatility for operators—making planning precision essential.

- Fleet transition dynamics: The coexistence of legacy and newer engine/airframe combinations—especially platforms that require specialized certification for next‑generation powerplants—creates differentiated capital requirements for MRO providers and operators. Strategic investment in certified capability is now a binary decision for many players.

- Margin pressure and concentration: While the market is sizable and growing, competitive concentration remains moderate (top‑3 providers account for roughly one‑third of market activity, top‑5 under half). That structural balance sustains pricing pressure in commoditized services while leaving room for premium differentiation in certified and high‑complexity work.

What corporate leaders must decide in 2026

We see five decisions that will determine who captures disproportionate value over the next investment cycle. Each decision links directly to specific deliverables inside our report—financial models, capex templates, break‑even analyses, and contracting playbooks.

Worldwide Narrow Body Aircraft MRO Market

- Capacity versus capability: Should new hangar and shop investments prioritize volume (more narrow‑body bays) or capability (LEAP and other certified engine shop tooling, advanced borescope and repair equipment)? The right mix varies by portfolio, but the wrong choice locks in subscale returns or stranded specialized assets.

- Vertical integration vs. network partnerships: Operators and independents must choose between building in‑house capacity for high‑value shop visits (engines, landing gear) and outsourcing to certified partners. Our scenario models quantify total cost of ownership across partnership types for multi‑year horizons.

- Supply chain resiliency investments: Material cost inflation and parts lead‑time volatility materially affect turnaround times and utilization. Decisions on safety stock, local warehousing, and multi‑source contracts should be informed by supplier risk heatmaps provided in the full report.

- Workforce strategy and productivity uplift: With certified labor shortages persisting and wage inflation elevated, companies must choose between talent investments (upskilling, apprentice pipelines) and productivity spend (digital tooling, predictive maintenance) to protect margins.

- M&A and footprint optimization: Given moderate market concentration and the geographic dispersion of demand, targeted acquisitions or joint ventures remain among the fastest routes to scale. Our M&A playbook helps acquirers evaluate accretion and integration risk at the asset and contract level.

Competitive dynamics: what we analyzed and why it matters

PW Consulting’s competitive chapter synthesizes public disclosures, facility footprints, and recent strategic moves by incumbents to identify capability maps and competitive gaps. The report analyzes leading providers—airline‑affiliated and independents—across three dimensions: certified engine capability, narrow‑body airframe capacity, and global service footprint. A few illustrative observations:

Worldwide Narrow Body Aircraft MRO Market

- Lufthansa Technik: A broad offering spanning base and line maintenance, engine overhaul for both legacy and next‑gen engines, and modification work. Their multi‑facility strategy provides operational flexibility; however, investments in certification and readjusted slot allocation will determine their ability to sustain premium pricing on next‑gen work.

- ST Engineering Aerospace: World‑leading scale in independent airframe man‑hours and a deliberate capacity expansion program for engine shop visits. Their recent facility openings signal a strategy geared to capture higher shop‑visit volumes in Asia‑Pacific and beyond.

- AAR Corp. and Delta TechOps: Two North American players that illustrate different routes to market—AAR via independent expansion across dedicated narrow‑body facilities, Delta via airline‑backed scale and, recently, full licensed capability for both LEAP variants—altering competitive dynamics for operators seeking single‑vendor solutions.

- SR Technics, HAECO, Turkish Technic, Iberia Maintenance, TAP: Each brings differentiated strengths—engine heavy shop experience, airport‑centric line maintenance, or regional hangar scale. Recent contract wins and capability certifications show an industry actively reallocating workloads to optimize turnaround and cost.

Recent industry signals that change the playbook

- Capability certification arms race: Announcements of licensed LEAP overhaul capability and new engine shop openings in 2025–2026 have shifted barometers for long‑term service agreements. Firms without certified pathways face material opportunity loss in next‑gen engine work.

- Long‑term service agreements (LTSAs): MoUs and LTSAs for fleets and engines are accelerating, compressing the window to secure feedstock for shops. These contracts have immediate implications for inventory planning and working capital.

- Supply and cost pressure: Elevated material inflation and persistent parts bottlenecks are extending turnaround times and increasing the total cost per event. Providers that invest in analytics‑driven inventory optimization unlock service reliability advantages.

The operational playbook inside the full report

PW Consulting’s report is structured to move practitioners from insight to action. Key operational deliverables include:

- Integrated demand-supply models that map anticipated shop visits to facility capacity under multiple fleet growth and disruption scenarios (2026–2032).

- CapEx decision tools with IRR, payback and sensitivity analysis tailored for hangar expansions, engine cell buildouts, and tooling investment.

- Labor force planning templates that reconcile certification pipelines, wage inflation forecasts, and productivity uplift from digital tooling.

- Supplier risk matrices and inventory policy optimizers that trade off stocking costs against guaranteed turn times for high‑impact part groups.

- M&A playbook and valuation checklists for independents and airline affiliates seeking inorganic growth or strategic alliances.

Risk scenarios and stress tests

Our scenario engine tests the market against upside and downside shocks: accelerated fleet modernization, a steeper‑than‑expected material‑price inflation, or a sudden tightening of certified labor supply. Outputs include demand elasticity curves, capacity utilization thresholds where pricing power flips, and covenant stress tests for lenders and lessees. For CFOs and strategy teams contemplating capital deployment in 2026, these stress tests are the difference between a strategically timed acquisition and a capital misstep.

How strategic buyers and operators should use this report in 2026

- Prioritize capability certifications required for next‑gen engines before contracting windows close. Our certification timeline estimator indicates typical lead times and critical path milestones.

- Lock in strategic feedstock through multi‑year agreements or joint venture arrangements to stabilize utilization for new cells—use our contracting templates to negotiate protections for volume and price volatility.

- Rebalance capital toward digital maintenance systems that reduce shop dwell times and extend component life—our ROI frameworks quantify payback periods under realistic labor‑cost trajectories.

- Embed supply‑chain resilience as a quantifiable line item in maintenance budgets rather than an ad hoc contingency—our inventory models show where working capital buys uptime.

Conclusion — the strategic edge for 2026

Between USD 55.2 Billion (2025) and a projected USD 80.9 Billion (2032), the narrow‑body MRO market presents both steady growth and concentrated strategic inflection points. The next 12–18 months will define who captures the more attractive, higher‑margin portion of that growth. PW Consulting’s Worldwide Narrow Body Aircraft MRO Market Report provides not only the market sizing and forecast (CAGR 5.6%) but also the operational blueprints, financial decision tools, and competitive playbooks decision‑makers need to act confidently in 2026.

Next steps

This preview highlights themes and decision levers. For the granular models, proprietary segment and regional breakdowns, provider benchmarking matrices, and transaction‑level financials that underpin 2026 action plans, consult the full report. PW Consulting clients receive direct access to our interactive scenario tool and advisory workshops tailored to board and investment committee timelines.

For detailed analysis of this topic, please visit the official page:Worldwide Narrow Body Aircraft MRO Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com