Bioburden Testing Market Developments Create New Growth Pathways Across Global Healthcare

Health |

2026-05-27 16:37:37

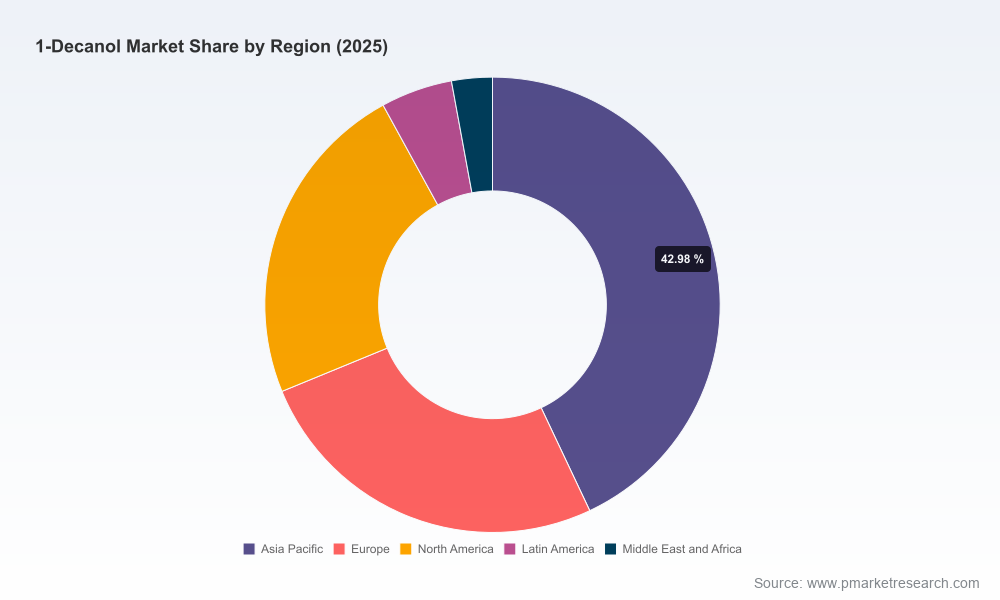

The global 1‑decanol market is entering a phase of measured expansion and selective consolidation that will define supplier strategies, procurement priorities, and product positioning across 2026. Our new Worldwide 1‑Decanol Market study (base year 2025, historical coverage 2020–2025, forecast 2026–2032) finds that the market reached approximately USD 280.8 Million in 2025 and is forecast to expand to roughly USD 436.4 Million by 2032, reflecting a compound annual growth rate (CAGR) of about 6.5% across the forecast horizon.

Worldwide 1-Decanol Market

This brief translates the report’s core strategic implications for corporate leaders who must make capital allocation, sourcing and regulatory compliance choices in 2026. It highlights where the market is predictable enough for confident investment, where volatility requires contingency planning, and which capability-building moves will generate disproportionate returns — while deliberately withholding the granular segmentation tables and raw datasets that reside in the full report to encourage direct access to the source intelligence.

Worldwide 1-Decanol Market

Transition from recovery to growth: The historical trajectory shows steady expansion since 2020, with an acceleration into 2024–2025. 2026 is the first full year in which late‑cycle investments (capacity expansions, product certification, and sustainability upgrades) begin to shift supply balances.

Worldwide 1-Decanol Market

Regulatory inflection points: New compliance requirements and labeling dynamics are phasing in during 2026 — creating compliance costs and reformulation pressure for consumer-facing products.

Feedstock and trade volatility: Raw material price swings and trade barriers that crystallized in late 2025 and early 2026 materially change cost curves and sourcing rationales.

Put simply: the market is large enough to support multiple global suppliers and specialized regional players, and it is growing at an above‑average rate for specialty alcohols. That growth is driven by industrial demand (plasticizers, lubricants, surfactants) and pockets of premiumization (high‑purity grades for pharmaceutical and cosmetic uses). For 2026 decision cycles, the macro picture supports incremental capacity investments where cost and feedstock security can be demonstrably managed, while aggressive greenfield expansion outside existing value pools should be assessed against regulatory and logistics headwinds.

Demand composition: End‑use markets remain diversified across industrial intermediates and consumer products. Demand growth will be strongest in applications that favor higher‑purity or sustainably sourced grades.

Supply response: Producers with integrated oleochemical feedstocks and producers using petrochemical routes will compete on price, quality and sustainability credentials. Mid‑cut fatty alcohol producers are increasingly differentiating through certification and premium product grades.

Price drivers: Two immediate pressure points are raw material availability and regulatory compliance. Recent supply disruptions in key feedstock-producing countries and higher lauric‑acid/coconut‑oil pricing materially influence cost curves for natural grades, while tariffs and compliance costs are reshaping import economics.

European chemical regulations: Producers supplying surfactant and detergent markets must finalize updated exposure scenarios and compliance dossiers in 2026; non‑compliance risks market access restrictions and reputational impact.

North American labeling dynamics: State‑level product listing developments require manufacturers and brand owners to reassess formulation disclosures and marketing claims for consumer products.

Trade measures: Tariff adjustments and trade policy tightening in early 2026 produce immediate sourcing cost impacts and will motivate buyers to re‑route or re‑contract supplies in pursuit of duty mitigation.

The market is characterized by a mix of global chemical majors, regional oleochemical specialists, and a handful of synthetic‑route players who supply high‑purity streams. Key industry participants include:

BASF SE (Ludwigshafen, Germany) — a global chemical integrator offering 1‑decanol within a broader fatty alcohol portfolio, positioned to serve surfactant, lubricant and plasticizer markets through scale and formulation know‑how. (https://www.basf.com)

Evonik Industries AG (Essen, Germany) — focused on higher‑value applications including cosmetics and detergents; recent sustainability certification moves increase its appeal to European formulators. (https://www.evonik.com)

KLK Oleo (Shah Alam, Malaysia) — an oleochemical player expanding capacity to address Asia‑Pacific demand, leveraging palm kernel feedstocks and regional logistics advantages. (https://www.klkoleo.com)

Musim Mas Group (Singapore) — supplying mid‑cut fatty alcohols with an emphasis on surfactants and emulsifiers; product innovation for pharmaceutical excipients is a recent strategic play. (https://www.musimmas.com)

PT Sinar Mas Oleochemical (Jakarta, Indonesia) — export‑oriented producer serving detergent, textile and polymer additive markets out of Southeast Asia. (https://www.sinarmasoleo.com)

Eco Services Operations, LLC (formerly Sasol) (Houston, USA) — a synthetic 1‑decanol supplier using Ziegler chemistry to deliver high‑purity streams for industrial applications. (https://www.ecoservices.com)

Godrej Industries Limited (Mumbai, India) — catering to domestic and export markets with established soap and lubricant customer relationships. (https://www.godrejindustries.com)

Recent strategic moves underscore the competitive themes we expect to see play out in 2026: capacity expansions in Asia to capture regional demand; sustainability certification to secure supply to European formulators; and product‑grade differentiation to access pharmaceutical and personal‑care premiums.

For procurement heads, R&D leaders, and corporate strategists, our report translates market dynamics into concrete actions. The following priorities should be in every 2026 playbook:

Sourcing resilience: Implement dual‑sourcing and regional supplier baskets that explicitly account for tariff exposure and feedstock volatility. Enact rolling 12‑month hedging windows for oleochemical feedstocks where available.

Certification as market access: Fast‑track sustainability certification and mass‑balance chain‑of‑custody options where European and premium buyers are material to your revenue mix.

Product portfolio optimization: Identify which grades merit investment (high‑purity, pharma‑grade, sustainably certified) versus which should be steady‑state commodity offerings. Use targeted pilot lines rather than full‑scale conversion to test premium pathways.

Regulatory readiness: Allocate budget and expert time in 1H‑2026 to complete REACH submissions and state‑level labeling risk assessments; cost of late compliance will exceed planned mitigation spend.

M&A and capacity moves: Prioritize tuck‑ins that add feedstock security or specialty grades. Greenfield projects should pass a scenario hurdle that includes higher feedstock and compliance costs and a slower ramp‑up case.

Commercial terms re‑engineering: Shift toward mix‑based long‑term contracts with flex windows and indexation clauses tied to feedstock benchmarks rather than fixed‑price long‑term agreements in volatile environments.

Feedstock disruption and price spikes — strategic mitigation: diversified feedstock hedging, alternative chemistries evaluation.

Regulatory non‑compliance — strategic mitigation: dedicated regulatory sprints and certified third‑party reviews.

Trade policy shocks — strategic mitigation: tariff‑aware sourcing, local inventory staging and bonded warehousing options.

Quality/specification mismatches for premium markets — strategic mitigation: co‑development with strategic customers and conditional offtake agreements.

Our Worldwide 1‑Decanol Market study is built to be operationally useful for 2026 decisions. Highlights include:

A 7‑year forecast model (2026–2032) with scenario overlays to stress‑test investment cases under different feedstock and regulatory tracks.

Supplier scorecards that assess capacity position, feedstock mix, sustainability credentials, and trade exposure — designed for rapid inclusion in sourcing RFPs.

Regulatory tracker and timeline with actionable milestones and estimated compliance lead times tailored to surfactant, detergent and personal‑care supply chains.

Commercial playbooks for buyers and sellers: negotiating templates, index‑clause recommendations and sample contract language for 12–36 month terms.

An M&A screening matrix highlighting target archetypes and suggested valuation adjustments for feedstock security and certification status.

Price‑impact scenario maps to quantify how input shocks, tariffs and certification costs feed through to landed cost across typical trade lanes.

Immediate (0–3 months): conduct an exposure audit that maps suppliers against tariff, feedstock and regulatory risk; renegotiate critical contracts to include indexation and force majeure clarity.

Near term (3–12 months): deploy targeted investments in certification and pilot production for high‑value grades; execute pilot dual‑sourcing arrangements and inventory buffering where warranted.

Medium term (12–36 months): evaluate strategic M&A or joint‑venture options to secure feedstock integration or regional footprint expansion, subject to the scenarios in the forecast model.

1‑Decanol is a specialty feedstock whose strategic value accrues to firms that combine tight supply‑chain governance with selective product premiumization. In 2026, the winners will not be those who merely react to price moves, but those who translate regulatory foresight, certification advantages and feedstock security into commercial terms that customers value and competitors cannot easily replicate. Our report is designed to shorten that time to value by providing the quantitative backbone and executable playbooks that decision‑makers need now.

This release intentionally presents strategic conclusions and operational frameworks while withholding detailed segmentation tables and granular pricing schedules held in the full study. To obtain the complete dataset, supplier scorecards, scenario model and contract templates, please visit PW Consulting’s report landing page or contact your PW Consulting account director for an executive briefing and data license.

For detailed analysis of this topic, please visit the official page:Worldwide 1-Decanol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com