Worldwide Automotive Fuel Level Sensor Market — Strategic Imperatives for 2026

Executive snapshot

As OEMs and Tier suppliers prepare their 2026 roadmaps, PW Consulting’s new market study on Worldwide Automotive Fuel Level Sensors offers a timely, decision-grade view of an often-underappreciated component set. The industry is sizable and steady: the global market reached an estimated USD 950.0 Million in 2025 (base year) and is forecast to expand at a compound annual growth rate (CAGR) of 3.2% through the 2026–2032 forecast window, reaching roughly USD 1.18 billion by 2032 under the central scenario. This growth masks important technology, regulatory and demand-side shifts that will re-shape supplier economics and product priorities over the next 24 months.

Worldwide Automotive Fuel Level Sensor Market

Why this matters for 2026 decisions

- Component-level leverage: Fuel level sensors sit at the intersection of hardware, calibration software and fuel-system integration. Small design or sourcing moves can yield outsized margin and reliability benefits when adopted across a vehicle platform.

- Regulatory pressure as a forcing function: New emissions and safety standards are making fuel monitoring more than a convenience feature — it is now a required element in combustion optimization, diagnostics and crashworthiness strategies.

- Transition management: Electrification is changing demand geometry rather than eliminating it overnight. Suppliers that sequence product portfolios — balancing legacy ICE requirements with new, hybrid and alternative-fuel architectures — will protect revenue while funding next-generation R&D.

- Concentration and competition: The fuel level sensor market is moderately consolidated (top-three companies account for a near-majority share; top-five approach clear dominance), so strategic partnerships, platform wins and selective M&A will determine who captures the higher-margin opportunities.

What the report delivers — practical, operable insights

PW Consulting’s report is structured to move beyond descriptive market figures to provide executives with tools they can act on in 2026:

Worldwide Automotive Fuel Level Sensor Market

- Executive dashboards: scenario-based revenue projections and sensitivity analyses tied to OEM platform ramp schedules and regional powertrain mixes.

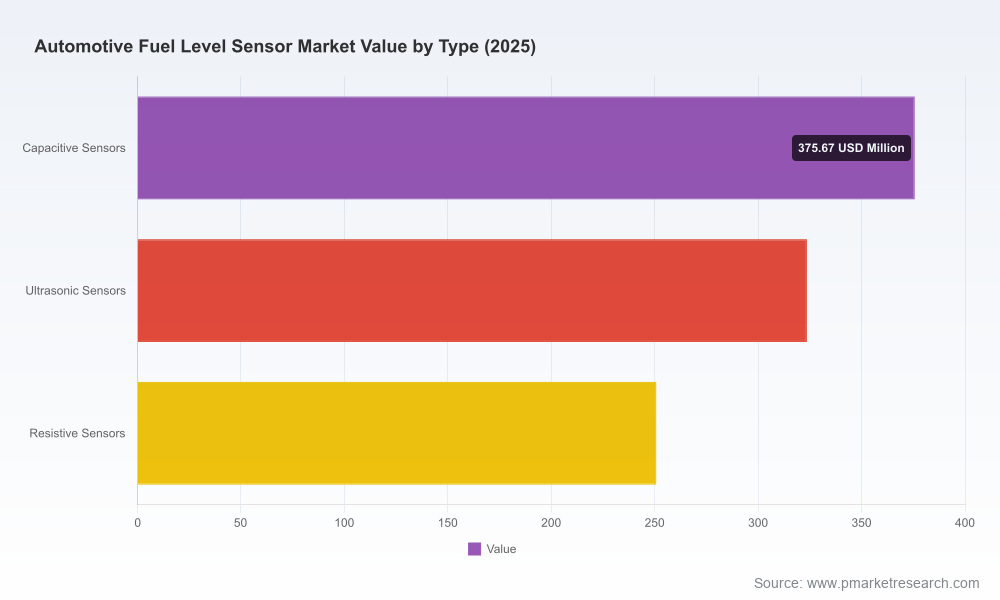

- Technology roadmaps: side-by-side evaluation of capacitive, ultrasonic, resistive and Hall-effect approaches with failure-mode profiles, calibration corridors and integration complexity metrics.

- Supply-chain heatmaps: critical single-source dependencies, semiconductor and passive components vulnerability assessments, and tiered mitigation strategies (dual-sourcing, consigned inventory, local content playbooks).

- OEM sourcing playbooks: negotiation levers, technical validation checklists, and total-cost-of-ownership models tailored to large and small vehicle programs.

- Go-to-market and aftermarket strategies: channel economics for OE vs. aftermarket, retrofit opportunities in regional fleets, and service/diagnostics monetization scenarios.

- M&A and investment screening: deal scorecards, synergies analysis, and integration risk matrices for targets across sensing, signal processing and fuel-system submodules.

Competitive landscape — who to watch and why

Our competitive analysis profiles global incumbents and agile challengers. The field blends traditional automotive component houses with specialist sensor firms and electronic systems players. Key strategic profiles include:

Worldwide Automotive Fuel Level Sensor Market

- Robert Bosch GmbH (Gerlingen, Germany) — Deep OEM integration experience and a broad portfolio covering capacitive, float-based and ultrasonic technologies. Bosch’s strength is platform-level module integration and global toolkits for fuel tank assemblies.

- Continental AG (Hanover, Germany) — Focused on sender units with integrated temperature sensing and close relationships with major European and North American OEMs; strong program capture capability on high-volume architectures.

- Denso Corporation (Kariya, Japan) — Longstanding supplier to Asian OEMs; specialized in reed switch and capacitive solutions that are optimized for regional fuel-system designs and hybrid vehicle programs.

- BorgWarner Inc. (Auburn Hills, MI, USA) — Through legacy Delphi Technologies assets, BorgWarner emphasizes multi-fuel compatibility and North American/European program focus.

- Visteon Corporation (Van Buren Township, MI, USA) — Differentiates by integrating fuel-level sensing into cockpit clusters and HMI systems, opening data monetization and predictive diagnostics pathways.

- Sensata Technologies (Attleboro, MA, USA) — Expanding into fluid-property sensing; recent product launches indicate a move toward converged fuel-property + level solutions for heavy-duty markets.

- CTS Corporation, TE Connectivity, Gill Sensors & Controls, Methode Electronics — These firms provide specialized electronic sensing, ruggedized form factors, motorsport/commercial niches and pump-module integrations, respectively.

Market concentration metrics underline the competitive dynamic: the top three suppliers capture a substantial share of industry revenue, and the top five consolidate an even larger portion of the market, amplifying the importance of program wins and supplier consolidation plays.

Recent industry developments to factor into 2026 plans

- Sensata’s late-2024 launch of next-generation fluid-property sensors expands the addressable use-cases beyond simple level measurement and should accelerate adoption in heavy-duty and fleet telematics applications.

- Continental’s supplier nomination for a major OEM platform earlier in 2024 demonstrates the strategic value of platform-specific validation cycles — winning early design-in for a generation of vehicles creates long-tail aftermarket advantages.

- Validation and JDA activity among established suppliers and OEMs (notably Denso and CTS engagement timelines) signal an ongoing shift toward capacitive and electronic approaches for hybrid powertrains.

Supply-chain and technology headwinds

Three structural headwinds deserve active mitigation planning in 2026:

- Semiconductor & component bottlenecks: Recent multi-quarter disruptions in automotive-grade ICs drove extended lead times and elevated procurement costs. Suppliers need a layered sourcing approach, including contractual protections, localized buffer stocks and validated second-source ICs.

- Calibration and technology trade-offs: While non-contact and capacitive methods deliver accuracy in modern plastic tanks, they introduce calibration complexity in mixed-fuel and foaming conditions. Ultrasonic techniques offer advantages in non-intrusive measurement but can be sensitive to fuel surface dynamics and acoustic noise.

- Regulatory and safety constraints: New emissions regimes and crashworthiness standards are creating stricter requirements for fuel monitoring accuracy and mechanical robustness. Suppliers must certify sensors to withstand both performance and crash-impact mandates to stay platform-eligible.

Strategic playbook for 2026

Based on scenario modeling and supplier intelligence, PW Consulting recommends the following prioritized moves for suppliers, OEMs and investors:

- Defend platform positions with integrated value — Pack sensor hardware, calibration software and diagnostics into a single supplier offering to raise switching costs for OEMs.

- Invest in multi-fuel and hybrid compatibility — Prioritize R&D that ensures sensors function across gasoline, ethanol blends, biodiesel and hybrid tank environments; this protects revenue as fuel mixes evolve.

- Build semiconductor resilience — Establish dual-sourcing agreements, create consignment stock arrangements with OEMs and evaluate captive procurement for critical ICs.

- Leverage aftermarket and telematics — Commercial vehicle fleets present durable demand; bundle sensing hardware with telematics services and predictive maintenance subscriptions.

- Pursue selective M&A and partnerships — Targets that bring software calibration IP, advanced fluid-property sensing or domain-specific ruggedized hardware provide quicker routes to differentiated offerings.

- Comply and document for new standards — Proactively map sensor qualification to emerging emissions and crash-safety requirements; produce compliance-ready validation packages to shorten OEM qualification cycles.

Scenarios and risk matrix included in the report

The full study includes three demand scenarios (baseline, downside, upside) that model variations in ICE vehicle production, EV adoption rates, and regulatory tightness. Each scenario is stress-tested for semiconductor shortages, raw-material cost shocks and supplier consolidation events. The result: actionable contingency plans that indicate break-even thresholds for product investment, recommended inventory buffers, and prioritized OEM targets under each future state.

Conclusion — how to use this intelligence in 2026

For executives making program and capital-allocation decisions in 2026, the fuel level sensor market presents both defensive and opportunistic pathways. Defensive plays include securing platform contracts, hardening supply chains and ensuring regulatory compliance. Opportunistic moves involve integrating sensors with vehicle data services, expanding into fluid-property sensing, and capturing aftermarket monetization. PW Consulting’s report supplies the models, supplier heatmaps and playbooks to convert market signals into executable actions.

Next steps

PW Consulting’s Worldwide Automotive Fuel Level Sensor Market report contains the complete segmentation tables, proprietary unit-volume models, supplier scorecards and downloadable scenario workbooks. We intentionally present high-level findings here to demonstrate the study’s rigor; detailed sub-segment metrics and OEM-level mappings are available exclusively in the full report. Contact our research team or visit the report page to obtain the comprehensive datasets and consultation options that will accelerate your 2026 strategic decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Fuel Level Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com