How Is Mobile CRM Transforming Customer Engagement and Sales Performance?

Networking |

2026-06-23 09:38:02

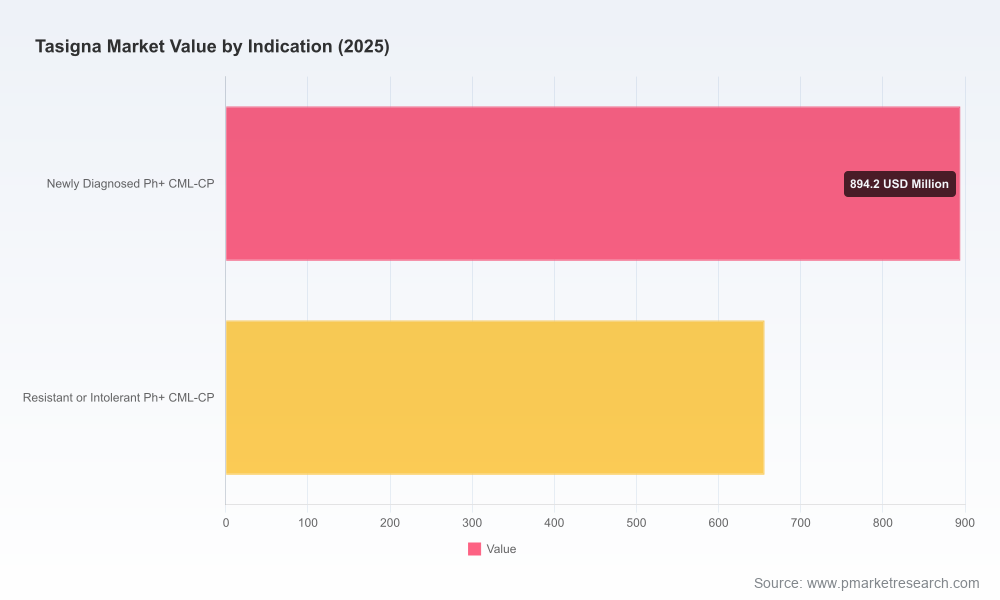

PW Consulting’s latest Worldwide Tasigna Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides a strategic playbook for life‑science executives, payers, investors, and clinical leaders facing a sharply contracting branded market. The report captures the market’s trajectory from its 2020 peak through the post‑patent era and models outcomes across regulatory, reimbursement, and competitive scenarios. In headline terms, the global Tasigna market — measured in USD millions — has declined from the 2020 level and stood at approximately USD 1,550 million in the base year (2025). PW Consulting projects a continuing contraction across the 2026–2032 forecast window, yielding a negative compound annual growth rate (CAGR) of approximately -11.45% across that period, with the market approaching multi‑hundred‑million levels by 2032 under our base case. These dynamics, combined with a highly concentrated supplier landscape, create a narrow strategic runway for incumbents and new entrants alike.

Worldwide Tasigna Market

2026 will be a decisive year for stakeholders who must translate the post‑patent market structure into operational decisions. Strategic questions we help answer include:

Worldwide Tasigna Market

Our analysis supplies actionable answers grounded in modeled scenarios, competitive intelligence, and practical implementation checklists intended for Q1–Q2 2026 board and commercial planning cycles.

Worldwide Tasigna Market

The Tasigna market’s decline is a structural reality of loss of exclusivity and accelerated generic entry. PW Consulting documents the downward shift in absolute market value from 2020 through 2025 (base year USD 1,550 million) and models the continuation of that trend across 2026–2032. Under our central scenario, the market contracts with a -11.45% CAGR during the forecast interval, resulting in a materially smaller global market by 2032. While downside outcomes exist under aggressive generic penetration and lower reimbursement regimes, upside scenarios — where branded share is buoyed by specialty contracting or label extensions — remain possible and are modeled in detail within the report.

One of the report’s most consequential findings is the degree of market concentration post‑patent expiry. A small number of manufacturers continue to account for the lion’s share of remaining branded volumes and revenues, producing a highly concentrated market structure that changes the calculus for pricing and supply strategy. Our concentration metrics indicate an environment where the top three and top five suppliers capture a dominant proportion of branded revenues — a configuration that favors incumbents with established supply chains and robust patient support capabilities while simultaneously pressuring smaller players and new entrants to pursue niche strategies.

Concurrently, the generics market has matured quickly in certain jurisdictions. The first authorized generic launches and regulatory milestones have already reshaped prescribing patterns in major markets, and our scenario work models the next waves of generic introductions and their typical pricing trajectories. Notably, real‑world reimbursement mechanics — such as average sales price‑based Medicare Part D payments in the United States — amplify the speed and magnitude of branded revenue declines after patent expiration.

Beyond pure economics, regulatory and safety constraints materially influence commercial strategy. Tasigna’s safety profile — including boxed warnings for specific cardiac risks — imposes ongoing clinical monitoring needs that affect prescribing patterns and product positioning. The report synthesizes the latest regulatory timeline events, including patent expirations that catalyzed generic competition, and maps likely regulatory touchpoints that could alter market access and utilization over the next 18–36 months. These risk levers create both obstacles and opportunities: while safety warnings limit some expansion strategies, they also sustain a segment of differentiated branded demand among physicians and patients who prioritize continuity of care and comprehensive support programs.

Novartis AG remains the principal branded manufacturer and global marketer of Tasigna, retaining a central role in market dynamics. Our profile of the incumbent assesses operational strengths (global manufacturing footprint, patient support infrastructure, regulatory know‑how) and strategic vulnerabilities (revenue pressure from generics, cost‑to‑serve for shrinking volumes). The report documents recent commercial snapshots, including reported branded sales outcomes in 2023 and the impact of first‑to‑market generics that began to shift prescriber and payer behavior in late 2022.

Generic manufacturers have already made material moves to capture tender and retail channels in major markets. The strategic playbook for generics varies by market: aggressive price competition and formulary placement in high‑volume markets; targeted hospital tenders and niche dosing programs in others. PW Consulting models the competitive interactions between branded and generic suppliers across the full set of commercial levers — rebates, contracting, patient access programs, and litigation strategies.

Designed as a decision support tool rather than a descriptive survey, the report provides a suite of tactical deliverables for 2026 operations:

Based on our analysis, PW Consulting recommends a four‑track strategic posture for decision‑makers entering 2026:

PW Consulting’s assessment synthesizes proprietary primary research, regulatory filings, aggregated sales intelligence, and payer interviews. Our modeling techniques combine top‑down market sizing with bottom‑up channel economics and clinical adoption curves. Where empirical disclosure is limited, we apply conservative assumptions and stress‑test outcomes across plausible future states. The work is peer‑reviewed by our oncology and market access specialists and updated with the latest post‑patent developments through Q4 2025.

In keeping with the “trailer” principle, this press release emphasizes strategic findings and actionable direction while deliberately withholding granular segmented tables and line‑item forecasts. The full report contains detailed segmentations by region, dosage strength, and indication; downloadable forecast tables (USD millions) for each year from 2020 through 2032; and primary‑source citations. Those datasets and the underlying model are available exclusively via the PW Consulting report portal. For teams that require the detailed segmentation and modeled outputs to run their internal analyses, access instructions and licensing options are provided on the report landing page.

As firms finalize FY‑2026 strategies, PW Consulting offers the following services to convert insight into action:

For access to the full Worldwide Tasigna Market report, granular forecasts, and licensing details please visit the PW Consulting report portal. The complete package includes the forecast datasets, competitor scorecards, scenario model files, and the step‑by‑step implementation templates necessary to operationalize the strategic recommendations described above.

PW Consulting remains available to support rapid strategic alignment as 2026 unfolds. Our objective research and pragmatic commercial playbooks are designed to turn a shrinking market into a controlled, value‑preserving transition for those who act early and decisively.

For detailed analysis of this topic, please visit the official page:Worldwide Tasigna Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com