Key Growth Drivers in the Immunodiagnostics Market: Insights & Industry Forecast

Health |

2026-02-23 08:23:40

As governments, energy companies and industrial operators pivot from legacy hydrocarbons to low‑carbon fuels, reformer units remain a critical technological and commercial hinge point. PW Consulting’s latest Worldwide Reformer Unit Market report—based on a 2025 base year and a 2026–2032 forecast horizon—tracks the evolution of this market and translates it into concrete decision triggers for executives planning capital allocation, technology selection and supply‑chain strategies in 2026.

Worldwide Reformer Unit Market

Market scale and trajectory: The global reformer unit market reached a USD 864.5 Million base in 2025 and is forecast to approach roughly USD 1.38 Billion by 2032, reflecting a compound annual growth rate of 6.95% across the 2026–2032 forecast period. The 2026 year‑one forecast in the report provides a practical near‑term anchor for budgeting and project pipelines.

Worldwide Reformer Unit Market

Competitive structure: The market exhibits moderate concentration, with the top three and top five suppliers accounting for material shares that favour scale and integrated technology providers. Our CR3 and CR5 analysis highlights the competitive advantage enjoyed by firms that combine proprietary process technology, catalyst or metallurgy expertise and global EPC capabilities.

Worldwide Reformer Unit Market

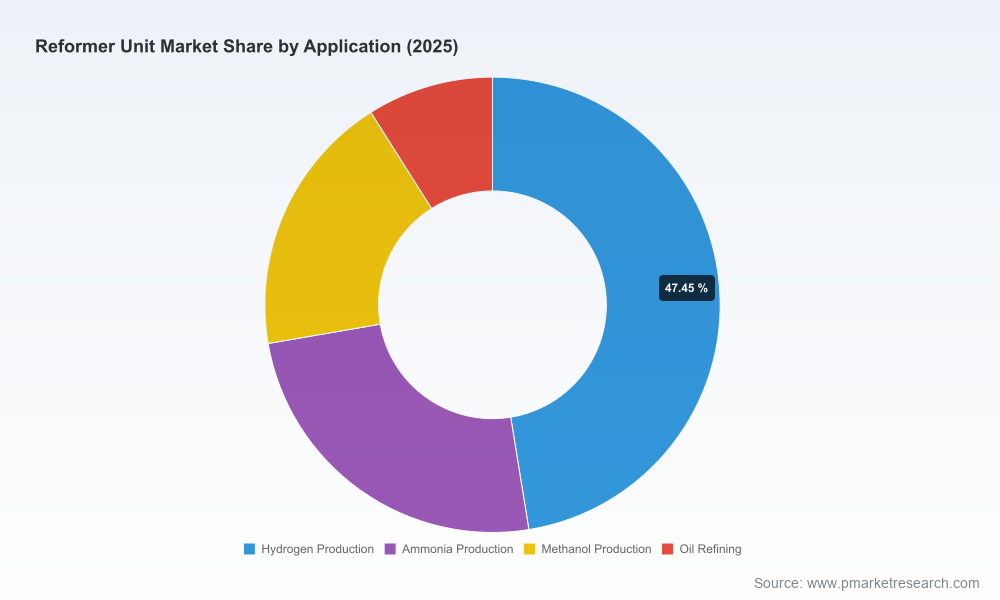

Strategic inflection points: Electrification of reforming, integration with carbon capture, modular on‑site solutions, and tighter emissions regulation are the near‑term themes that will re‑shape procurement choices and project economics across refining, ammonia, methanol and hydrogen projects.

Capital allocation under tighter constraints: The growth trajectory and year‑one forecast provide an empirical basis for capital prioritization. For asset owners evaluating retrofit versus replacement in 2026, the report translates market momentum and technology trends into payback windows, sensitivity to carbon pricing and likely vendor timelines.

Vendor selection and risk management: Our competitive analysis maps supplier capabilities across process licensing, catalysts, high‑temperature metallurgy and modular plant delivery. Procurement teams can use this to pre‑qualify suppliers not just on price, but on decarbonization roadmaps, aftersales service coverage and spare‑parts lead times.

Technology tradeoffs: The report frames SMR, ATR and catalytic reforming not as binary choices but as a technology stack influenced by feedstock, end use, decarbonization constraints and local regulation. For many buyers in 2026, decisions will hinge on compatibility with electrification, CCS readiness and lifecycle OPEX under carbon pricing scenarios.

Timing of projects: Because the market is growing yet concentrated, the report helps predict vendor capacity windows and delivery‐lead‑time premium points—key inputs for timing EPC contracts, tender cycles and long‑lead‑item procurement such as reformer tubes.

Robust market sizing and forecast methodology—transparent assumptions and scenario modelling for 2026–2032, including base case and downside stress tests tied to carbon pricing and feedstock volatility.

Demand driver analysis—detailed treatment of hydrogen economy initiatives, low‑carbon ammonia projects and refinery conversion dynamics that create near‑term project pipelines.

Technology deep dives—comparative performance, retrofit pathways, electrification potential (e‑reformer scenarios), and implications for thermal efficiency and direct CO2 emissions.

Supply‑chain mapping—vendor capability matrices for process licensors, catalyst suppliers, metallurgy specialists and EPC contractors; procurement checklists for long‑lead items and spares.

CapEx & OpEx benchmarking—typical project profiles, sensitivity to steel and alloy prices, and maintenance cycles influencing total cost of ownership.

Regulatory and policy playbook—how energy efficiency mandates, emissions standards and carbon pricing alter project economics in major jurisdictions.

Commercial intelligence—project tracker, recent developments, M&A vectors and strategic partnership opportunities for 2026 entrants and incumbents.

The reformer market is shaped by a mix of technology licensors, catalyst specialist, metallurgy providers and full‑service EPC firms. Each class brings a different risk/return profile for buyers:

Technology licensors and large industrial gas firms (examples include established European licensors and multinational industrial gas engineering arms) remain the focal point for world‑scale hydrogen, ammonia and methanol projects where integration, performance guarantees and vendor financing matter.

Catalyst suppliers and process innovators—firms with advanced catalyst ranges and pre‑reforming solutions—are pivotal where unit performance, selectivity and runtime drive margin, particularly in methanol and specialty hydrogen applications.

Metallurgy and component manufacturers—producers of cast and alloy reformer tubes and high‑temperature components—define maintenance intervals and life‑cycle cost. Buyers should explicitly evaluate alloy specs and historical tube life as part of LSTK tender evaluations.

EPC and fabrication contractors are critical when project timelines and local content requirements make modular skid delivery or on‑site engineering the deciding factor. The ability to combine modular small‑scale solutions with fast commissioning is now a competitive differentiator.

Recent market moves reinforce these dynamics: leading engineering groups recorded a wave of small on‑site project wins linked to decarbonization in 2025, while long‑term supply agreements for low‑carbon ammonia projects signalled industrial buyers’ willingness to lock capacity with integrated gas suppliers. Conference presentations in late 2025 showcased electrified reforming as an actionable pathway for emissions reduction—an idea moving quickly from pilot to bid tables.

Electrified reformers (e‑REFORMER): The report evaluates realistic efficiency and emissions outcomes for electrified retrofit and greenfield options. Peer‑reviewed field studies indicate potential direct flue‑gas CO2 reductions of up to approximately 91% in specific ammonia plant retrofits, along with modest thermal efficiency improvements at the plant level—metrics that materially shift lifecycle emissions under many carbon pricing regimes.

Carbon capture integration: For brownfield projects with existing SMR or ATR footprints, CCS compatibility is now a procurement table stake. The report offers decision trees that show break‑points where CCS plus fuel switching becomes preferable to full electrification, depending on electricity source and carbon price.

Regulatory push: Energy efficiency mandates and tightening GHG targets will continue to elevate the value of vendors that can provide measurable, auditable efficiency uplift and retrofit pathways.

Two supply‑side facts deserve immediate attention for 2026 planning:

Raw materials: Steel remains the primary input for reformer pressure parts and tubes. Price cycles matter for both CapEx and spare parts inventories; early‑2026 market conditions show steel at or near the bottom of its cycle with recovery expected to gain traction from 2027. Procurement teams should balance near‑term contract captures against anticipated steel inflation in later phases.

Component life and maintenance: Advances in creep‑resistant alloys and centrifugally cast tube technologies have extended safe operating intervals. These metallurgy improvements translate into fewer unplanned shutdowns and can materially affect life‑cycle cost; however, they also increase upfront component cost and may shift warranty and service terms.

Short‑cycle risk: Projects that assume immediate, low‑cost electricity or slow carbon pricing may face stranded asset risk if regulation or grid decarbonization lags. Our scenario modelling quantifies break‑even carbon prices for common retrofit paths and informs contracting strategies (e.g., indexed PPA vs fixed PPA).

Vendor concentration risk: With a mid‑to‑high level of market concentration, overreliance on a single vendor can expose projects to delivery bottlenecks. The report provides a supplier diversification matrix to guide dual‑source strategies and long‑term maintenance contracts.

Technology obsolescence: Rapid advances (electrified reformers, modular packaged units, hybrid CCS hybrids) mean that multi‑decade asset decisions should include upgradeability clauses and modular interfaces in EPC contracts.

Reassess procurement windows: Use the 2026 baseline and vendor capacity signals to lock long‑lead orders early where price and delivery windows matter; delay discretionary CapEx where modular retrofits that accommodate e‑reformers or CCS are feasible.

Negotiate value‑based contracts: Push for performance guarantees tied to thermal efficiency and emissions intensity rather than pure equipment supply. Include lifecycle spare‑parts and alloy‑spec commitments to limit maintenance cost volatility.

Adopt staged decarbonization roadmaps: Build decision points into project plans that allow switching between fuel decarbonization (hydrogen blending, electrification) and capture pathways depending on grid and policy developments.

Prioritize supplier ecosystem resilience: Vet metallurgy and catalyst suppliers not only for technical fit but for financial health, geographic redundancy and spare‑parts inventory strategies.

This brief highlights the structural trends, vendor dynamics and decision levers that will define successful reformer projects in 2026. PW Consulting’s full Worldwide Reformer Unit Market report contains the detailed segmentations, vendor scorecards, project pipelines and data tables that procurement, strategy and investment teams will need to operationalize these insights. In line with our “preview” approach, detailed sub‑segment figures and geographic/application split data are reserved for the comprehensive report available through our distribution channels.

For teams preparing budgets, tenders or investment memos in 2026, the report offers a pragmatic toolkit: validated market sizing, scenario templates, vendor negotiation checklists and a project tracker calibrated to current tender and EPC cycles. Contact PW Consulting for licensing or to arrange a briefing with our reformer‑unit practice leads.

For detailed analysis of this topic, please visit the official page:Worldwide Reformer Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com