Worldwide Luxury Car Coachbuilding Market — Strategic Preview for 2026 Decision‑Makers

PW Consulting is pleased to release a strategic preview of our forthcoming Worldwide Luxury Car Coachbuilding Market report. Built on a 2025 base and a detailed 2026–2032 forecasting horizon, the study synthesizes primary interviews, supplier cost-models, and competitive intelligence to translate market movements into boardroom-ready decisions. At a macro level, the coachbuilding market has recorded robust expansion and is projected to continue on a double-digit-adjusted growth trajectory, with a compound annual growth rate of 9.15% driving the industry from roughly USD 1.15 billion in 2025 toward a multi‑billion dollar market by 2032. This briefing highlights the report’s strategic value for executives planning resource allocation, partnerships, and product strategies in 2026, while preserving the granular datasets and proprietary scenario outputs for subscribers.

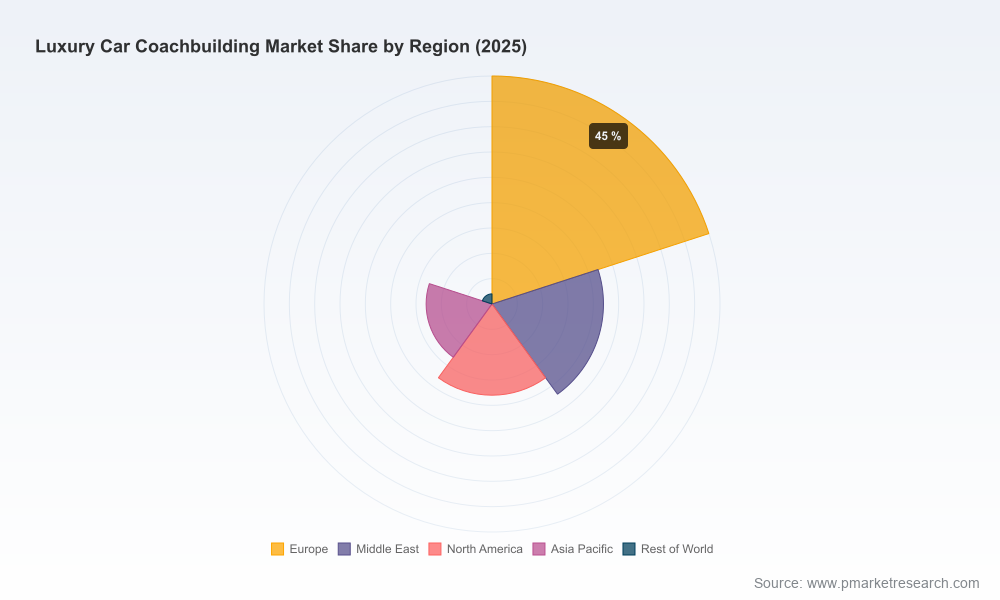

Worldwide Luxury Car Coachbuilding Market

Why 2026 Is a Strategic Inflection Point

Several coincident forces are reshaping luxury coachbuilding in ways that make 2026 a year for bold strategic moves rather than incrementalism. First, electrification of ultra‑luxury and hypercars is no longer theoretical — leading coachbuilders and OEM special‑projects teams are moving from prototype to limited production coachbuilt EVs, integrating bespoke bodywork with electrified platforms. Second, client expectations have expanded beyond one‑off coachbuilt bodies to multi‑year, experience-centric relationships: invitation-only programs and curated post‑delivery services are becoming part of the product offering. Third, raw material dynamics — notably a significant decline in aerospace‑grade carbon fiber costs over the past decade — together with ongoing aluminum expertise in classic coachbuilding are altering the design-to-cost calculus for bespoke projects.

Worldwide Luxury Car Coachbuilding Market

Market Dynamics and Structural Characteristics

- Sustained premium demand: The market’s growth reflects both traditional one‑off commissions and a growing pipeline of limited‑series coachbuilt runs tied to collector markets and brand halo strategies.

- Hybrid business models: Coachbuilding today sits at the intersection of heritage ateliers, OEM special‑projects divisions, and specialist tuners — each pursuing different margins, capacity models, and IP postures.

- Concentration with room for specialist playbooks: Market concentration is notable among the top incumbents, which creates high entry barriers for volume play but opens attractive niches for highly differentiated artisanal and technology‑led propositions.

- Material & regulatory pressures: Global emissions and sustainability expectations are accelerating adoption of lightweight composites and aluminum solutions; concurrently, falling costs of advanced composites are enabling their broader use in bespoke applications.

Competitive Landscape — Who’s Shaping the Industry

Our competitive analysis maps over a dozen core players that are shaping strategy across segments. These range from heritage coachbuilders and OEM in‑house divisions to specialist re‑body and tuning houses. Notable strategic postures include:

Worldwide Luxury Car Coachbuilding Market

- Rolls‑Royce Motor Cars (Goodwood, UK): The March 2026 launch of a curated Coachbuild Collection and the unveiling of Project Nightingale — a limited‑run electric coachbuilt model developed with bespoke client collaboration — signal an OEM-led premiumization strategy that couples product rarity with multi‑year client engagement programs.

- Bentley Mulliner (Crewe, UK): Continues to leverage craft heritage and deep OEM integration to offer ultra‑luxury customizations that balance exclusivity with brand continuity.

- Pininfarina, Touring Superleggera, Zagato and other Italian ateliers: These firms trade on design pedigree and lightweight body expertise, increasingly blending hand‑formed aluminum and advanced composite manufacturing to serve both OEM collaborations and independent patrons.

- High‑performance specialists (Pagani, Koenigsegg, Pagani‑adjacent operations): Emphasize proprietary composite technologies and structural innovations, creating product differentiation at the extreme performance and price points.

- Tuners and conversion houses (Mansory, Brabus): Focus on high‑visibility rebody and widebody conversions with a business model centered on rapid turnarounds and strong aftermarket margins.

- Design & engineering studios (Italdesign, Ares, Niels van Roij): Provide end‑to‑end concept-to‑completion services that appeal to private clients and smaller marques seeking a turnkey coachbuilding partner.

The competitive map shows that strategic success in 2026 will depend less on size alone and more on a firm’s ability to combine production discipline, design distinctiveness, materials mastery, and customer experience orchestration.

What the PW Consulting Report Delivers — Practical Tools for Executives

Our full report is designed as an operational toolkit for 2026 planning cycles. It does not merely catalogue vendors or describe trends; it converts those trends into executable options and quantified tradeoffs. Key deliverables include:

- Scenario‑based market sizing and demand curves across the 2026–2032 forecast window, embedding alternative electrification and luxury demand pathways.

- Profitability and pricing frameworks for one‑off coachbuilt projects, limited‑series runs, and retrofit services, with unit economics sensitivities to materials, labor intensity, and certification costs.

- Supplier and materials playbook — supplier concentration maps, sourcing risk profiles, and cost‑curve models for aluminum and advanced composites informed by recent reductions in carbon‑fiber pricing.

- Manufacturing and capacity blueprints: recommended CAPEX phasing, cell structures for low‑volume high‑mix production, and automation levers that preserve artisanal quality while improving throughput.

- Client segmentation and go‑to‑market templates that align product cadence with collector cohorts, brand partners, and experiential service bundles.

- M&A and partnership screens with prioritized target archetypes, integration checklists, and post‑deal value capture roadmaps.

- Regulatory & sustainability matrix that quantifies likely compliance pathways and outlines low‑regret material and powertrain investments to mitigate policy risk.

- Five prioritized, actionable strategic choices tailored for 2026 planning (summarized below).

Five Strategic Choices for 2026

- Commit to an electrified coachbuild platform roadmap: Firms that lock technology partnerships and demonstrator programs now will gain pricing power as collectors reward EV coachbuilt rarities.

- Partner selectively with composites suppliers: Secure preferred access and pricing mechanisms to mitigate supply risk and capture margin uplift as composite adoption rises.

- Design client experiences as part of the product: Integrate multi‑year servicing, collection management, and bespoke commissioning journeys into commercial propositions to deepen lifetime value.

- Rationalize capacity through modular manufacturing: Invest in low‑volume, high‑flex cells that allow quick retooling between one‑offs and short production runs while keeping unit economics intact.

- Protect and leverage IP selectively: Balance openness for co‑creation with clients and partners against protecting proprietary structural and material know‑how that underpins premium pricing.

How Boards Should Use This Intelligence in 2026

Executives should use the report to stress‑test capital allocation, commercial partnerships, and product roadmaps under three alternative macro trajectories (conservative, base, and accelerated demand scenarios). Practical next steps we recommend for 2026 include:

- Run a 12‑month pilot program to validate an EV coachbuilt sub‑line with a controlled series volume and an integrated client experience, using a two‑phase investment approach to contain downside.

- Negotiate multi‑year agreements with composite suppliers to secure progressive price breaks tied to volume thresholds and joint IP development clauses.

- Develop a modular pricing architecture that translates bespoke design inputs into predictable margin buckets, enabling transparent client conversations and better working capital management.

- Create a governance forum that aligns product, legal, and CRM teams to manage bespoke commissioning, liability, and post‑delivery warranties in a standardized manner.

Closing: What You Get by Diving Deeper

PW Consulting’s full market report offers the quantitative underpinnings and proprietary scenario models that validate these recommendations. Subscribers receive the detailed market tables, region‑level demand scenarios, supplier cost models, and competitive market share analysis that support capital allocation and M&A decisions in 2026. This preview is intended to help senior teams decide which strategic plays merit immediate funding and which require staged validation.

For access to the complete datasets, the step‑by‑step operational playbooks, and bespoke advisory engagements that translate these insights into a 2026 execution plan, please visit the report landing page or contact PW Consulting’s Luxury Automotive practice. The full intelligence package includes the confidential annexes and client‑level interview transcripts that underpin our recommendations.

For detailed analysis of this topic, please visit the official page:Worldwide Luxury Car Coachbuilding Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com