Biopharmaceuticals Market Forecast and Size Expansion Driven by Innovation and Personalized Medicine

Other |

2026-02-19 07:42:25

As organizations accelerate cloud-first transformations, intrusion detection and prevention systems (IDS/IPS) that are cloud-native or cloud-integrated have moved from “nice-to-have” to strategic imperative. PW Consulting’s newest market study, with a 2025 base year and a 2026–2032 forecast horizon, projects the worldwide Cloud IDS/IPS market to continue growing at a compound annual growth rate (CAGR) of 15.2%. From an industry that reached USD 2,850 Million in 2025, our model anticipates robust expansion through the forecast window driven by workload migration, zero-trust adoption, and platform consolidation by cloud providers and security vendors.

Worldwide Cloud IDS IPS Market

Timing and buy-in: 2026 will be a make-or-break year for security architecture choices made in 2023–2025. Vendors and customers alike will be executing integration roadmaps—selecting between embedded cloud provider controls, third‑party cloud‑native offerings, and managed hybrid approaches. Our report arms CISOs, CIOs, and procurement leads with the evidence and decision frameworks needed to validate investments against growth, risk, and operational cost trajectories.

Worldwide Cloud IDS IPS Market

Budget planning under uncertainty: With strong market expansion expected, finance and procurement teams must balance immediate risk mitigation with total cost of ownership (TCO) for multi-year contracts. The report quantifies macro market sizing and supply-side concentration, helping organizations assess negotiation leverage and market liquidity when structuring 2026–2028 purchasing strategies.

Worldwide Cloud IDS IPS Market

Regulatory and energy pressures: New regulatory developments and rising energy demands for data centres change the calculus for where and how to deploy cloud IDS/IPS solutions. Our analysis links these macro forces to vendor roadmaps and recommended deployment patterns.

Market momentum: After accelerating through the early 2020s, the global Cloud IDS/IPS market remains on a strong growth trajectory. The market expanded meaningfully from 2020 through 2025 and is forecast to nearly triple over the 2020–2032 period under current adoption and threat assumptions.

Moderate concentration: The marketplace shows a mid-level concentration among leading vendors—enough to indicate established platform leaders, but with ample room for specialized innovators and cloud provider offerings to capture niche and high-growth segments.

Consolidation vectors: Buyers are increasingly favoring suites that integrate IDS/IPS with broader cloud workload protection, firewalling, and managed detection services. This has created two parallel trends: deep integration by a handful of incumbents and modular, API-first offerings from nimble competitors.

Energy and hosting economics: Significant increases in data‑centre electricity use—exacerbated by AI workloads—are driving higher operational costs for inline and telemetry-heavy IDS/IPS deployments. Customers evaluating inline prevention versus agent-based or telemetry-driven detection should factor in energy consumption as part of long-term TCO modeling.

Regulatory shifts and certification pathways: Changes in government testing and approval programs are altering product validation roadmaps, particularly for vendors pursuing public sector and defense contracts. Simultaneously, evolving data sovereignty rules are pushing more deployments toward localized or hybrid architectures.

Platform vs. partner trade-offs: Leading cloud providers continue to embed IDPS capabilities in platform services, while security vendors compete on advanced detection, policy orchestration, and managed services. Buyers should model both short-term integration benefits and long-term vendor lock-in risks.

Our vendor analysis evaluates technical coverage, go-to-market motion, integration breadth, and strategic posture. We profile global leaders, cloud natives, and specialized security players—highlighting where each class of vendor is likely to win in 2026 procurement decisions.

Cisco Systems — A broad portfolio player integrating cloud IDS/IPS into firewall and cloud security stacks. Cisco’s strength is in enterprise-grade integration, channel reach, and hybrid networking footprints that appeal to large-scale, multi-site customers.

Fortinet — Competes on scalable, cloud-delivered IPS capabilities and AI-driven threat intelligence. Fortinet’s value proposition centers on performance and cost-efficiency for high-throughput cloud networking.

Trend Micro — Focuses on cloud workload protection with managed rule automation and tight marketplace integrations. Recent partnerships that enable one-click managed rule groups demonstrate an emphasis on operational simplicity for cloud-native customers.

Palo Alto Networks — Positions IDS/IPS within a holistic cloud security platform that spans workload, network, and policy controls. Strengths include integration with cloud governance and DevSecOps toolchains.

Check Point, CrowdStrike, Zscaler — Each brings differentiated strengths: Check Point in multicloud policy consistency, CrowdStrike in behavior-driven detection extended to cloud workloads, and Zscaler in zero-trust inline prevention at scale.

Cloud provider offerings — Microsoft Defender for Cloud, AWS partner and native capabilities, Google Cloud IDS: platform-native services are increasingly attractive for teams standardizing on a primary public cloud. These services trade advanced feature parity for deeper platform integration and simplified procurement.

Other notable vendors — IBM, Juniper, Sophos and others are competing on managed offerings, SD‑WAN integrations, and mid-market managed detection. Their differentiated routes-to-market are essential for customers prioritizing managed services or telco-led cloud platforms.

Trend Micro’s partnership enabling managed rule groups in cloud marketplaces simplifies rule management and reduces operational overhead for cloud IDS/IPS. For many organizations, this reduces the barrier to deploying effective prevention capabilities.

Telco and cloud platform launches that bundle firewall with integrated IDS/IPS demonstrate service providers’ move to offer differentiated managed security for enterprise customers—especially for localized and regulated deployments.

Policy and energy headwinds—such as shifts in certification programs and rapidly rising data‑centre energy demand—are practical constraints that must be modeled into vendor selection and deployment architecture plans.

Market model and scenario forecasts (2026–2032) with sensitivity testing across adoption rates, energy cost trajectories, and regulatory outcomes.

Vendor scorecards and shortlists tailored to buyer archetypes (enterprise, cloud-first, telco customers, public sector), with recommended procurement levers and negotiation talking points.

Deployment decision frameworks comparing inline prevention, agent-based HIPS, telemetry-only detection, and managed IDS/IPS services—each mapped to risk appetite, latency tolerance, and cost profile.

TCO and energy impact calculators that translate differences in detection architectures into multi-year cost projections—crucial where energy and compute materially affect hosting economics.

Integration checklists for DevSecOps pipelines, cloud-native networking, SIEM/SOAR handoff patterns, and data sovereignty controls.

Competitive moves and M&A watchlist—where consolidation risk is material for long-term roadmap commitments.

Adopt a two-track procurement posture: secure tactical, platform-native defenses to meet immediate compliance and integration needs, while progressing strategic pilots with third-party vendors to retain flexibility and advanced detection capability.

Quantify energy and operational impacts in all TCO comparisons. Where telemetry volume is high (e.g., AI-heavy workloads), prefer architectures that offload preprocessing or adopt selective inline prevention to limit energy-driven cost escalation.

Prioritize interoperability and API-first vendors to avoid vendor lock-in as regulatory and platform decisions evolve; insist on transparent migration paths in RFPs.

Embed certification and data‑sovereignty gating criteria into sourcing documents for regulated sectors; track changes in government testing programs that may alter required attestations.

Leverage managed rule groups and marketplace integrations to reduce operational overhead where internal security operations capacity is constrained.

Map current and planned workloads to detection architecture options—include latency, throughput, and telemetry budget.

Run vendor scorecards against your primary constraints (regulatory, operational headcount, multi-cloud strategy).

Simulate three-year TCO under high-energy and high-telemetry scenarios to ensure procurement resilience.

Negotiate phased SLAs and exit clauses tied to feature parity and data egress terms to reduce long-term lock-in risk.

For 2026, cloud IDS/IPS decisions are both tactical and strategic: they shape immediate security posture and set the foundation for multi-year cloud platform economics, compliance posture, and operational maturity. PW Consulting’s report provides the macro sizing—rooted in reliable growth forecasts—and the vendor- and deployment-level playbooks that decision-makers need to make defensible, cost-effective choices.

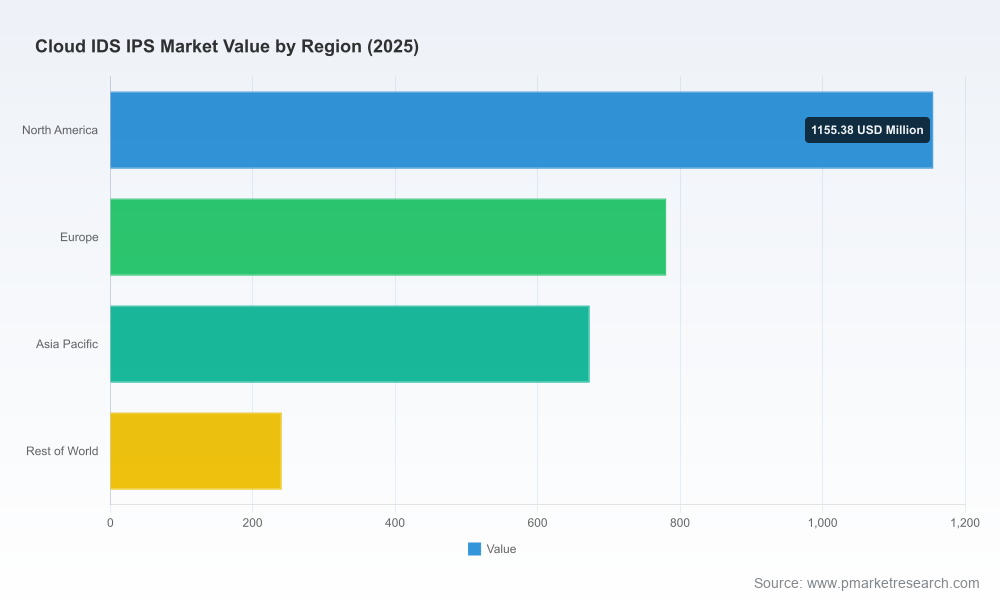

To preserve the value of this executive preview and ensure actionable confidentiality, detailed regional and deployment splits, vendor financials, and scenario tables are intentionally excluded here. For the complete dataset, granular segmentation, vendor scorecards, and the downloadable TCO models, access the full report on our website or contact PW Consulting’s advisory team for a tailored briefing.

Discover the full Worldwide Cloud IDS/IPS Market report and schedule a strategic briefing at PW Consulting’s report portal.

For detailed analysis of this topic, please visit the official page:Worldwide Cloud IDS IPS Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com