Essential DevOps Skills to Build a Successful IT Career

Other |

2026-07-14 07:28:00

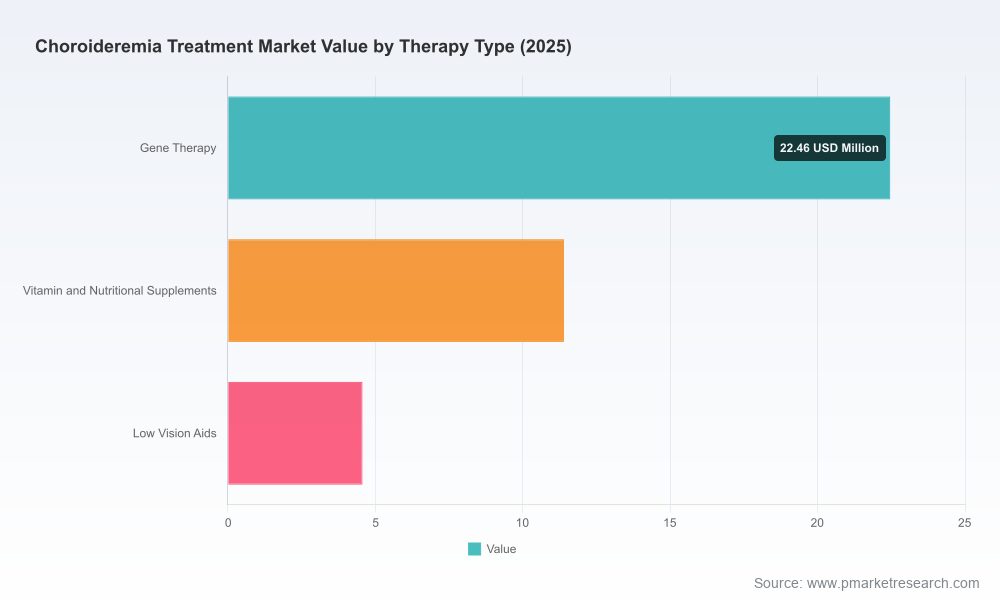

The Worldwide Choroideremia Treatment Market is entering an inflection point. Our new PW Consulting report — grounded in a 2020–2025 historical baseline and a detailed 2026–2032 forecast — shows a rapid expansion driven by novel gene-replacement, optogenetic, and non-gene therapeutic approaches. The market, measured in USD million, expands from a base-year (2025) value to multi-fold levels through 2032, reflecting a compound annual growth rate (CAGR) of 32.65% across the 2026–2032 forecast horizon. That growth trajectory signals both opportunity and complexity: sizeable upside for well-positioned developers and investors, and meaningful technical, regulatory and commercial hurdles for newcomers and incumbents alike.

Worldwide Choroideremia Treatment Market

Timing-sensitive investments — 2026 is a pivotal year for portfolio allocation. Several early-stage and mid-stage programs are advancing into dose-expansion or pivotal-enabling studies and regulatory engagement. Our analysis isolates the decision points that convert clinical readouts into corporate value inflection points.

Worldwide Choroideremia Treatment Market

Regulatory framing — the disparity in acceptable clinical endpoints across jurisdictions (for example, differences in visual acuity thresholds used by major regulators) materially changes development programming and market access strategies. The report maps regulatory permutations and their likely commercial consequences.

Worldwide Choroideremia Treatment Market

Manufacturing and cost-model realism — AAV vector and advanced modality manufacturing dynamics are central to both feasibility and pricing strategies. We quantify manufacturability risk, cost drivers and scale-up breakpoints that will determine which programs can be viably commercialized.

Concentration matters — the market remains meaningfully concentrated among a small set of active developers and research institutions. Our competitive concentration metrics demonstrate that a limited number of programs and custodians of data/IP will disproportionately shape commercialization outcomes.

Using a rigorously vetted base year and validated market model, the report projects an accelerating revenue path through the forecast period. From the 2025 baseline, the market grows substantially in 2026 and expands several-fold by 2032. This steep growth path (CAGR of 32.65% from 2026–2032) is underpinned by successful transitions of clinical-stage candidates, broadened labeling or platform-enabled optogenetic/photopharmacology launches, and improved clinical endpoint strategies that capture clinically meaningful improvements in patient functional vision.

For executives and investors, these macro figures should be read as directional: they highlight where capital and capabilities must be concentrated to capture value — clinical development, regulatory affairs expertise, scaled GMP manufacturing, and patient-focused outcomes research.

The competitive field combines small biotechs pursuing differentiated modality approaches, academic and non-profit custodians of clinical datasets, and historical program owners whose assets have been re-homed. Key profiles and strategic implications are summarized below.

Kiora Pharmaceuticals — advancing a small-molecule photoswitch approach with active Phase 2 programs and validated functional vision endpoints. Kiora’s platform offers a potentially lower-cost, repeat-dosing, minimally invasive pathway compared with AAV-based replacements. For strategists, Kiora embodies the trade-off between modality novelty and near-term manufacturability/payer acceptance.

Ray Therapeutics — pursuing an optogenetic channelrhodopsin-based gene therapy delivered intravitreally. Ray’s regulatory recognition in the form of expedited-designation pathways underscores the agency appetite for novel optogenetic modalities. Intravitreal delivery could materially ease surgical burden relative to subretinal approaches, altering clinical adoption patterns if safety and functional efficacy are demonstrated.

Choroideremia Research Foundation (CRF) — a non-profit actor that recently consolidated legacy program assets and natural history data. CRF’s acquisition of prior company assets and long-term datasets creates a unique repository that could accelerate endpoint definition, historical-control modeling, and potentially de-risk follow-on development programs. For partners and acquirers, CRF represents a strategic node for data-led regulatory strategies.

Legacy programs — several higher-profile corporate programs were halted or deprioritized in prior cycles following mixed Phase 2/3 outcomes. Those program discontinuations, and the subsequent transfer of assets and data to other custodians, have reshaped the developable opportunity set and created niches for platform innovators and non-profit stewards to influence future pathways.

Endpoint heterogeneity: Historically, high bars for primary endpoints — notably stringent visual-acuity thresholds in some regulatory jurisdictions — have been a material barrier to approval. Regional differences in acceptable improvement thresholds can yield divergent approval paths and market sizes. Our scenario models quantify the commercial impact of alternative endpoint acceptance, offering evidence-based go/no-go criteria for 2026 development plans.

Orphan and ATMP frameworks: Expedited pathways and orphan designations are enablers, but they do not eliminate the need for robust functional outcome data and durable safety signals. Sponsors should anticipate a dual-track strategy — early regulatory engagement coupled with long-term natural history and patient-reported outcome programs.

Payer realism: The high cost-to-manufacture of AAV-based and other single-administration therapies will trigger tough payer negotiations. Manufacturers must prepare for outcomes-based contracting, annuity-style payment pilots, and stringent real-world evidence commitments. Our reimbursement playbook in the report delineates negotiation levers and risk-sharing architectures that are commercially viable.

AAV vector production, reproducible GMP processes, and scalable fill/finish capacity remain primary gating factors. The combination of limited supplier capacity and high batch cost elevates manufacturing risk for smaller firms. Our operational assessment lays out capacity planning benchmarks, cost-of-goods sensitivity analyses, and preferred outsourcing vs. in-house scenarios — actionable guidance for 2026-capacity and capex decisions.

Choroideremia’s ultra-rare prevalence demands precision in trial design. The report synthesizes emerging consensus on clinically meaningful endpoints, leverages newly available long-term datasets, and provides optimized patient-identification frameworks to reduce screening burden and accelerate enrollment. Sponsors designing 2026 trials can use these templates to minimize regulatory uncertainty and maximize signal detection power in small cohorts.

Validated market sizing and revenue forecasting model (2020–2032) with scenario sensitivity and breakpoints for regulatory and reimbursement outcomes;

Pipeline landscaping and program-level risk matrices for active and legacy assets, including modality-differentiated competitive positioning;

Regulatory engagement playbook and endpoint scenario analysis tailored to major jurisdictions;

Manufacturing and supply-chain risk assessment with cost-of-goods models and outsourcing decision trees;

Commercialization pathways, pricing and reimbursement scenarios, and payer engagement templates;

Investor and M&A decision support tools: value-mapping of clinical inflection points, earn-out modeling, and partnership structuring options;

Appendices with curated regulatory precedent, trial-design templates, and data sources that underpin the market model.

Prioritize catalytic assets: allocate capital to programs with clear pathway advantages — differentiated delivery, validated functional endpoints, or lower manufacturing complexity.

Engage early with regulators and payers: use adaptive evidence-generation plans that combine randomized data, natural history comparators and robust patient-reported outcomes.

Secure manufacturing flexibility: mitigate supply risk through dual-sourcing, capacity options with CMOs, or partnership models that defer capital while preserving scale-up optionality.

Leverage data custodianship: partnerships or data-sharing agreements with foundations and academic consortia can accelerate endpoint validation and reduce development risk.

Design commercial access pilots now: negotiate outcomes-based frameworks and pilot annuity payments to pre-empt payer resistance at launch.

The choroideremia treatment landscape in 2026 is at once promising and exacting. Growth forecasts point to significant market expansion if clinical, regulatory, manufacturing and payer conditions align — but those same forces will punish misaligned programs. Organizations that combine modality-informed clinical design, realistic manufacturing strategy, and early payer engagement will be best positioned to capture the upside shown in our market scenarios.

PW Consulting’s full Worldwide Choroideremia Treatment Market report contains the detailed models, company-level analyses, and actionable tools referenced here. For teams crafting 2026 budgets, portfolio decisions, or M&A strategies, the report offers the operational blueprints and financial scenarios required to convert clinical progress into sustainable commercial value. Visit our report page to access the full findings, interactive models, and bespoke advisory options.

For detailed analysis of this topic, please visit the official page:Worldwide Choroideremia Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com