Worldwide Medical Microscopic Hemostatic Clip Market — 2026 Strategic Preview

PW Consulting’s new market study on the Worldwide Medical Microscopic Hemostatic Clip Market delivers a focused, decision-grade intelligence package designed for executives planning moves in 2026. Built on a 2020–2025 historical analysis (base year 2025) and an independent 2026–2032 forecast run, the study combines rigorous market-sizing, competitor benchmarking, regulatory mapping and scenario modelling to convert growing market momentum into concrete commercial tactics.

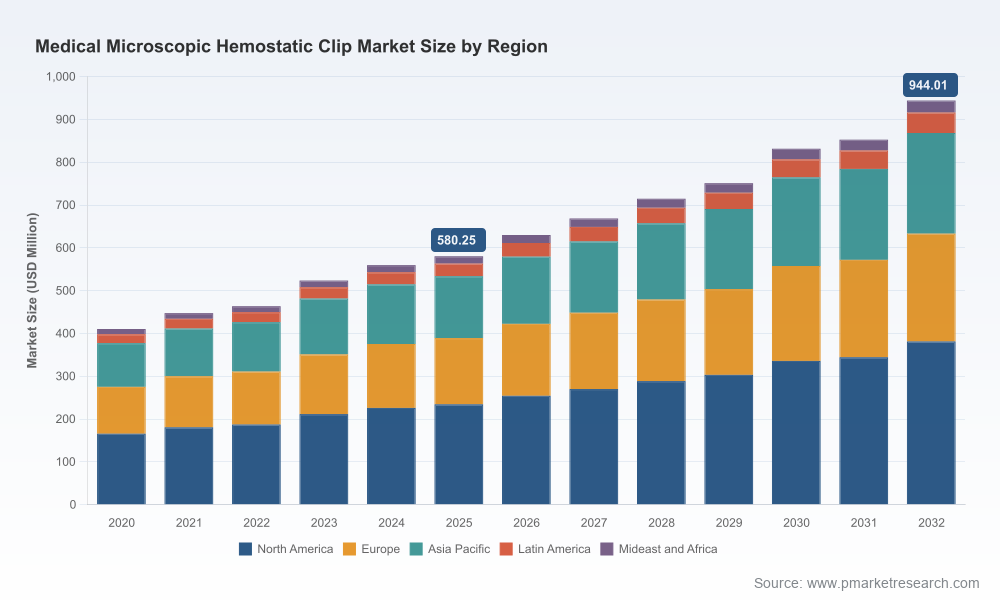

Worldwide Medical Microscopic Hemostatic Clip Market

Market at a glance

After a steady recovery and expansion through the early 2020s, the global microscopic hemostatic clip market reached a meaningful scale in the 2025 base year and is projected to continue expanding at a mid-single-digit-plus compound annual growth rate. Our model projects a robust multi-year growth trajectory through 2032, reflecting sustained procedure volumes, technology-driven device upgrades (rotatable, repositionable and automatic appliers), and expanding use cases across minimally invasive specialties. These macro trends create a predictable envelope for revenue planning, capital allocation and M&A prioritization in 2026.

Worldwide Medical Microscopic Hemostatic Clip Market

Why this report matters for 2026 decision-makers

- Fast, actionable guidance: a compact intelligence deck with an integrated financial model that lets commercial, product and corporate development teams run “what-if” scenarios in hours not weeks.

- Investment prioritization: objective sizing and growth levers that help R&D and portfolio teams choose between incremental feature development (e.g., rotation, one-step deployment) and more transformational bets (automatic appliers, reusable vs single-use economics).

- Commercial playbooks: go-to-market recommendations tailored to varying distributor models, hospital procurement dynamics and outpatient reimbursement changes that will be most relevant to 2026 contract cycles.

- M&A and partnership signals: identification of capability gaps and target archetypes that would meaningfully alter competitive position given current market concentration.

What the report contains — practical, executable outputs

- Top-line and bottom-up market sizing (historical 2020–2025; forecast 2026–2032) with an integrated Excel model that supports bespoke scenario runs, sensitivity testing and deal valuation templates.

- Segment and application architecture — clinical use-case maps, product-technology trees (rotatable, non-rotatable, automatic appliers, repositionable), and a buyer decision matrix that explains adoption thresholds.

- Competitive landscaping and strategic scorecards for incumbent and emerging players, including go-to-market models, pricing archetypes and capability gaps.

- Regulatory and reimbursement playbook — pathway timelines, common FDA/CE data expectations, and coding/reimbursement levers that influence hospital purchasing and outpatient adoption.

- Supply chain and manufacturing risk register — raw material sourcing (including titanium Grade 1 considerations), single-source vulnerabilities and recommended mitigation tactics.

- M&A heatmap and synergy calculators — quantifying accretive target profiles, expected cost and revenue synergies and integration risk factors.

- Commercial execution templates — sample contracting language, clinical evidence plans and KOL engagement blueprints ready to adapt for launch or portfolio expansion.

Note: This release intentionally omits the full regional and application splits and the granular tables contained in the subscriber dataset. That granular intelligence — including the downloadable model and proprietary segmentation matrices — is available via the report portal and is designed for clients who require transaction- and territory-level certainty.

Worldwide Medical Microscopic Hemostatic Clip Market

Competitive landscape — who’s shaping the market and what it means for 2026

The microscopic hemostatic clip market is characterized by a small number of established surgical-instrument and endoscopy platform suppliers, supported by a set of specialized microsurgical instrument makers. Market concentration is meaningful: the leading three players control roughly three-fifths of the market, while the top five approach four-fifths, creating both defensive moats and targeted opportunities for nimble challengers.

- Synovis Micro Companies Alliance (Baxter) — Synovis’s product strategy centers on titanium microclip pedigree and procedural ergonomics. Its GEM MicroClip and SuperFine MicroClip product lines, coupled with the introduction of the GEM ZIPCLIP automatic preloaded applier (cleared via FDA 510(k) in early 2025), signal a push towards integrated clip+applier systems. Strategic implication: competitors must decide whether to match with comparable integrated systems, compete on applier ergonomics, or pivot to differentiated disposables and pricing.

- Olympus — With the 2025 launch of a 360°-rotation, single-use hemostasis clip engineered for GI bleeding control and defect closure, Olympus demonstrates the continued importance of endoscopy platform vendors in defining clinical workflows. Strategic implication: platform suppliers will keep setting interoperability and procurement expectations in GI suites and outpatient endoscopy centers.

- Micro-Tech Endoscopy — The 2026 deal to acquire global distribution rights to a repositionable clip line shows how distribution consolidation can rapidly shift product availability and hospital purchasing patterns. Strategic implication: distribution rights and channel partnerships now have value comparable to product innovation alone.

- Amsel Medical — The SCureClamp (iDOT technology) represents an adjacent tactical play: a mechanical vessel occluder cleared for indications where metal ligation clips are indicated. Strategic implication: device differentiation that shifts a subset of procedures from consumable clips to mechanical occlusion devices will require incumbent vendors to adapt commercial tactics and evidence generation.

- Specialist instrument manufacturers (Peter Lazic, S&T, Scanlan, Kapp, MicroSurgical Technology) — These firms maintain leadership in neurosurgery and microsurgical spaces where precision, instrument feel and clinical trust are paramount. Strategic implication: larger platform players must engage with microsurgical OEMs either via partnerships, OEM supply agreements or targeted acquisition to secure clinical credibility in high-acuity specialties.

Regulatory, reimbursement and materials dynamics — actionable impact items

- Regulatory profile: Titanium hemostatic microclips are treated as Class II implantable clips in the U.S. (21 CFR 878.4300, product code FZP), with traditional 510(k) pathways and an emphasis on labeling, bench testing and biocompatibility. CE and ISO 13485 compliance remain baseline expectations for European and global market access. Practical recommendation: build a regulatory roadmap that front-loads bench validation, sterilization and labeling dossiers to compress time-to-market for next-gen appliers.

- Reimbursement levers: Recent coding developments (notably new outpatient reporting capabilities introduced in 2024) have created commercial upside for devices that demonstrably reduce OR time or enable outpatient defect closure. Practical recommendation: evidence packages should explicitly quantify throughput and setting-of-care benefits to capture incremental reimbursement and hospital contracting gains.

- Material and supply-chain realities: Microclips are largely manufactured from annealed Grade 1 titanium for malleability, biocompatibility and MRI compatibility. This creates concentrated upstream exposures (titanium supply, precision stamping and annealing capacity). Practical recommendation: secure multi-sourced supply agreements, qualify alternate suppliers and consider vertical-insourcing of critical forming steps if unit economics justify capital outlay.

Priority plays for 2026 — where to invest, partner or defend

- Product innovation: Prioritize development of appliers that reduce procedural steps (one-step deployment, preloaded cartridges) and improve orientation control (360° rotation, repositionability). These features materially influence hospital efficiency metrics and clinician preference.

- Clinical evidence: Invest in comparative-effectiveness studies that document OR time savings, reduced complication rates or expanded outpatient eligibility — outcomes that directly translate into purchasing decisions and reimbursement leverage.

- Channel and distribution strategy: Evaluate distribution partnerships and exclusive rights deals as strategic levers to accelerate market penetration. Recent distribution transactions demonstrate how channel control can change competitive dynamics rapidly.

- M&A and bolt-on targets: Use our M&A heatmap to prioritize targets that provide complementary geographies, unique applier IP or established microsurgical OEM credibility. Given market concentration, a single bolt-on can shift relative market position substantially.

- Manufacturing and sourcing: De-risk titanium supply and value-engineer stamping/annealing processes to protect gross margins as unit volumes scale under the forecasted growth curve.

How PW Consulting can support your 2026 agenda

PW Consulting offers a modular engagement suite to translate the market study’s insights into executable programs: tailored scenario modelling workshops, commercial due diligence for transactions, regulatory and reimbursement playbooks, M&A target screening and integration planning, and customized KOL and evidence-generation strategies. Our proprietary Excel model can be licensed standalone or accompanied by a hands-on strategy sprint to embed findings into your 2026 planning cycle.

Because this release is intended as a strategic preview, we have deliberately withheld the full regional, product and application split tables and the downloadable model. Clients who require the precise territory-level forecasts, product-by-application breakouts, CR-level detail and the full competitive financials can access the complete dataset via the report portal or by contacting our advisory team. Access to the Excel model enables immediate scenario runs (pricing, adoption curves, launch timing) and supports valuation work for acquisition targets.

To discuss how these findings apply to your portfolio, M&A pipeline, or commercial planning for 2026, contact PW Consulting’s Healthcare Devices practice. Our analysts will walk you through the model, validate your hypotheses and co-create a prioritized roadmap tailored to your risk appetite and time-to-value expectations.

For detailed analysis of this topic, please visit the official page:Worldwide Medical Microscopic Hemostatic Clip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com