PW Consulting: Retail Omni‑Channel Commerce Market Poised to Surge at 18.5% CAGR Through 2032

Other |

2026-07-02 12:19:48

PW Consulting’s latest market study on the Worldwide Adult Ventricular Assist Device (VAD) market provides a targeted, actionable intelligence package designed to inform critical corporate decisions as organizations set priorities for 2026. At the macro level the market has expanded from an estimated USD 1,385.4 Million in 2020 to USD 1,845.5 Million in 2025 and is projected to reach USD 2,742.12 Million by 2032, representing a compound annual growth rate (CAGR) of 5.81% across the 2026–2032 forecast horizon. These headline figures frame a market that is growing steadily but remains highly concentrated — the top three companies account for approximately 88.5% of sales and the top five for about 94.2% — creating distinct strategic dynamics for incumbents and challengers alike.

Worldwide Adult Ventricular Assist Device Market

Investment and portfolio prioritization: With predictable, mid-single-digit growth and high concentration, the VAD market rewards focused investments in clinical differentiation, lifecycle management, and service-led revenue models rather than scattershot new-product launches.

Worldwide Adult Ventricular Assist Device Market

Regulatory and reimbursement timing: Given PMA-class regulatory requirements and evolving payer codes, companies must align development and market access plans to reimbursement windows in 2026 to optimize launch economics.

Worldwide Adult Ventricular Assist Device Market

M&A and partnership readiness: High market concentration increases the strategic value of bolt-on acquisitions and alliances that deliver clinical data, peripheral technologies, or faster market access in priority geographies.

Regulatory inertia and intensity: Adult VADs are regulated as Class III medical devices under 21 CFR 870.02 in the U.S., requiring PMA pathways and sustained post-market surveillance. The EU MDR continues to strengthen Notified Body scrutiny and post-market obligations. These regulatory realities lengthen time-to-revenue and increase the importance of robust clinical and quality systems.

Reimbursement architecture is a tactical lever: In the U.S., CMS’s DRG framework (DRG 003) and the FY2025 payment benchmarks materially shape hospital adoption economics — for example, current CMS payment constructs for destination therapy create a defined revenue envelope that hospitals use to evaluate VAD programs. The 2024 CPT update expanding code 33975 to include percutaneous approaches further changes procedure coding dynamics and may shift hospital decision-making toward less-invasive options.

Product safety and recall risk are strategic inflection points: The HVAD system recall and continued advisory status for new implants since 2021 illustrate how device-specific safety issues can reshape competitive positions rapidly. When a legacy product is curtailed, incumbent rivals can capture share — but only if they can demonstrate superior outcomes and manage supply and service demand.

Concentration and clinical inertia: The market’s elevated CR3/CR5 metrics mean incumbents enjoy entrenched relationships with transplant centers and high-volume hospitals. New entrants must therefore present a compelling clinical-improvement or cost-of-care case to dislodge established suppliers.

Abbott Laboratories (Chicago, IL): HeartMate 3 remains a market reference point. Recent MOMENTUM 3 five-year data (October 2024) demonstrating durability and stroke-reduction outcomes reinforces Abbott’s clinical leadership. For competitors, the Abbott data set raises the evidentiary bar for both new devices and claims of superiority.

Medtronic (Dublin, Ireland): The legacy HeartWare/HVAD centrifugal platform has been constrained by a Class I recall and restricted new implants since late 2021. That continuing advisory environment creates near-term share-shifting opportunities for alternatives, but also exposes market fragility tied to safety events.

LivaNova PLC (London, UK): Regulatory momentum — including recent CE Mark approval for RELINANT — positions LivaNova as a company to watch in Europe where device-level differentiation and post-market evidence will drive uptake.

Berlin Heart GmbH (Berlin, Germany): With its EXCOR Adult VAD and recent controller upgrades, Berlin Heart underscores how incremental improvements in usability and battery life can sustain competitive advantage in niche clinical settings.

Syncardia Systems (Tucson, AZ): The SynCardia Total Artificial Heart remains a specialized alternative for biventricular failure cases not suitable for VAD therapy, and continues to be relevant for centers managing complex transplant pathways.

Taken together, these profiles show a market where clinical data, regulatory status, and device usability — not just price — determine winner-takes-most outcomes. PW Consulting’s analysis highlights which competitive moves are likely to shift shares and which investments are most defensible.

Financial models and scenario planning — multi-year revenue, cost, and cash-flow templates calibrated to realistic launch and reimbursement timelines. These models are parameterized so clients can test pricing, reimbursement mix, and adoption curves under several regulatory and payer scenarios.

Clinical-evidence roadmaps — prioritized trial designs, milestone timelines, and endpoint packages optimized to support PMA filings and payer dossiers in the U.S. and CE/Notified Body submissions in Europe.

Reimbursement playbooks — country-level reimbursement readiness assessments, model hospital economics reflecting DRG and CPT changes, and payer negotiation templates for value-based contracting pilots.

Commercial launch and channel strategies — segmentation of hospital archetypes, center-of-excellence engagement playbooks, service and training programs, and remote-monitoring monetization options.

Supply-chain and manufacturing risk maps — supplier concentration analyses, lead-time sensitivities, and cost-to-serve models to support sourcing and inventory decisions.

M&A and partnership scouting — shortlists of acquisition and alliance candidates, valuation frameworks, and integration risk checklists for technology access, clinical data, or geographic expansion.

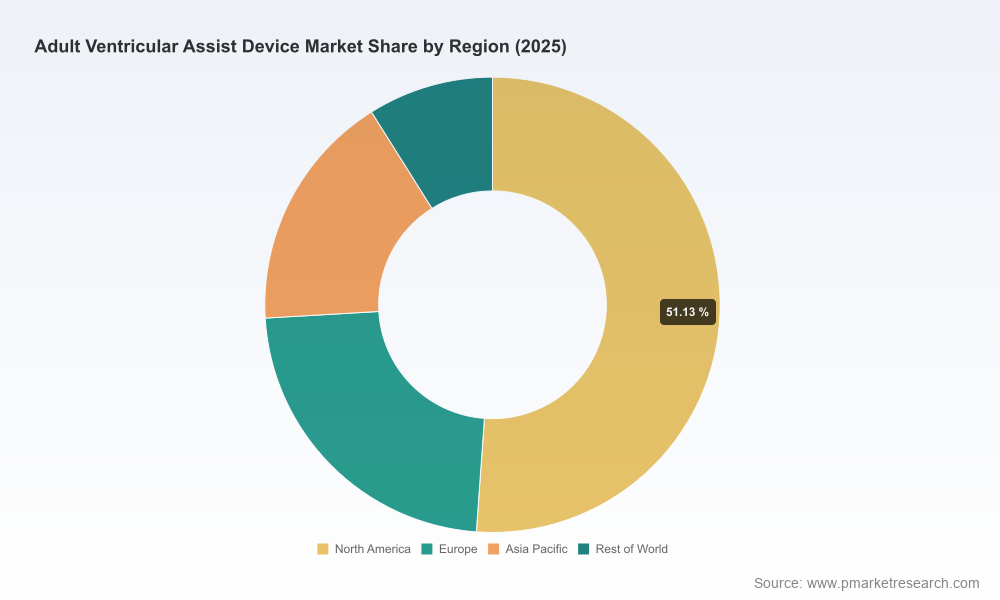

Note: This preview intentionally omits granular regional, type, and application revenue splits to preserve the integrity of the full intelligence package. The full report contains those detailed segmentations and downloadable models for executive use.

For incumbents: invest in lifecycle enhancements (durability, reduced stroke risk), expand service and remote-monitoring offerings to create recurring revenue, and accelerate evidence-generation to defend against rivals seeking share via performance claims.

For challengers: pursue focused clinical niches (e.g., high-risk patient subsets or usability-constrained centers), partner with transplant programs to secure referral pathways, and structure commercial pilots that quantify total cost of care improvements to payers and health systems.

For private equity and corporate M&A teams: target bolt-ons that deliver either clinical data assets, unique peripheral technologies (controllers, batteries, cannulation systems), or immediate access to underpenetrated centers — these assets materially shorten commercialization timelines.

For regulatory and access teams: align pivotal trial timelines with 2026 reimbursement cycles; ensure post-market surveillance infrastructures are in place to meet both FDA PMA conditions and EU MDR obligations without disrupting clinical supply.

New safety signals or expanded recalls that could abruptly change competitive dynamics and hospital purchasing behavior.

Adverse changes in reimbursement policy or DRG adjustments that compress hospital margins for VAD programs.

Disruptive technology entrants (e.g., percutaneous or fully implantable systems) capable of altering procedural coding and adoption curves.

Supply-chain shocks affecting critical components or manufacturing capacity.

PW Consulting’s monitoring dashboard flags these indicators and provides trigger-based response playbooks that clients can operationalize in 2026.

This briefing is crafted as a strategic preview to help leadership teams calibrate 2026 priorities. Executives seeking execution-ready tools — full segmentation tables, downloadable financial models, country-level reimbursement maps, and a prioritized acquisition shortlist — should consult the complete PW Consulting Worldwide Adult VAD Market report and our tailored advisory services. The full study contains the granular regional, type, and application splits, plus client-ready deliverables that translate insight into board-ready decisions.

To discuss how these findings apply to your portfolio, or to request the full report and associated consulting packages, please contact PW Consulting’s Life Sciences practice. Our analysts can prepare a confidential briefing that maps the market-level findings in this preview to your specific commercial, clinical, and regulatory objectives for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Adult Ventricular Assist Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com