SOC Services: Why Technology & SaaS Companies Need 24/7 Cybersecurity Protection

Cyber Security |

2026-07-01 12:36:24

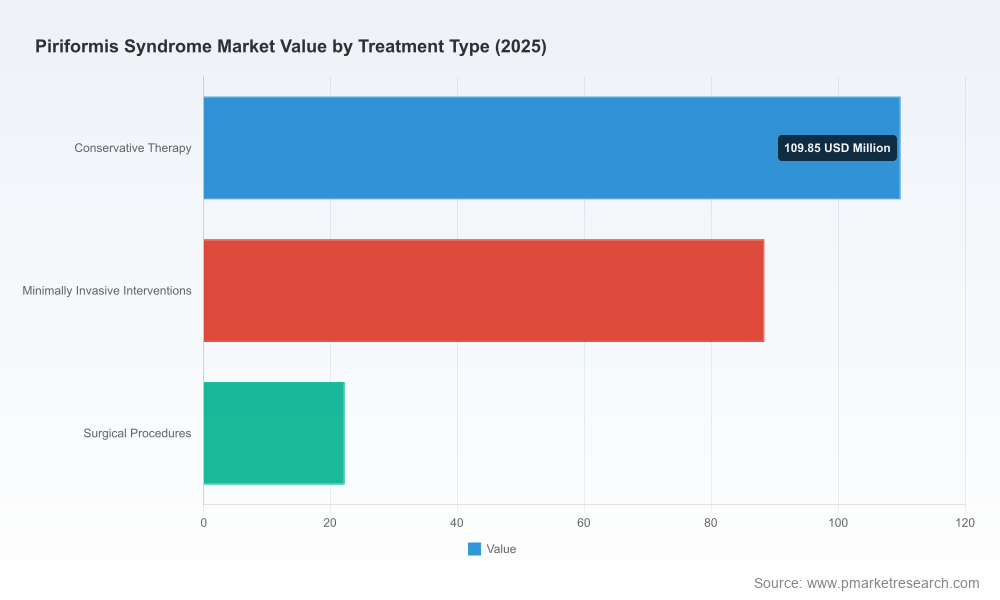

PW Consulting’s new Worldwide Piriformis Syndrome Market report (base year 2025; historical window 2020–2025; forecast 2026–2032) positions this niche but fast-maturing therapeutic area as a clear strategic frontier for device manufacturers, specialty pharma, clinic networks, and payers. At the macro level the market reached approximately USD 220.5 million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 5.51% through 2032, reaching just over USD 320 million by the end of the projection period. That trajectory signals persistent clinical demand, improving diagnostic clarity, and a multi-modal treatment evolution that creates differentiated value pools across conservative therapy, minimally invasive interventions, and surgical solutions.

Worldwide Piriformis Syndrome Market

Decision speed matters: modest absolute market size combined with steady growth rewards early movers that can prove differentiated clinical outcomes, establish reimbursement pathways, and lock in referral networks.

Worldwide Piriformis Syndrome Market

Cross-category convergence: non-pharmacologic modalities (TENS, shockwave, wearable therapeutics), targeted injections (botulinum toxin-based protocols), and focused minimally invasive procedures are converging in care pathways — creating opportunities for bundled-service models and hybrid reimbursement approaches.

Worldwide Piriformis Syndrome Market

Evidence is the gatekeeper: randomized controlled trials and registries published in 2026 are already reshaping payer criteria and clinical guidelines, increasing the value of rigorous real-world evidence programs for market access.

The market’s mid-single-digit CAGR reflects a balance between rising incidence/recognition of piriformis syndrome and conservative clinical management preferences. Key demand drivers include heightened clinician awareness, broader adoption of image-guided or landmark-based injection techniques, growth in outpatient procedural capacity, and increased patient willingness to seek targeted interventions earlier in the care pathway. Supply-side innovation — from minimally invasive outpatient procedures to wearable neuromodulation devices and improved rehabilitation protocols — is turning episodic symptom management into repeatable care pathways that payers can evaluate for cost-effectiveness.

Recent guidance from the Centers for Medicare & Medicaid Services and related LCDs has two immediate implications for commercialization and market-access planning. First, reimbursement teams must align evidence-generation strategies with payer expectations for off-label interventional uses (for example, botulinum toxin applications), documenting clear refractory-case criteria and measurable functional endpoints. Second, procedural coding conversations are being shaped by CMS clarifications regarding guidance methods (MRI/CT/EMG versus landmark techniques) for needle placement, which can materially affect procedural time and cost modeling for outpatient settings. Practically, companies should factor billing, coding, and documentation workflows into pilot deployment to avoid downstream access friction.

The competitive field blends specialty clinics and procedure innovators with broad-based pharmaceutical and device manufacturers. Market concentration is moderate: the three largest players control roughly one-third of market activity, and the top five players fall just under half — leaving ample room for focused entrants and regional leaders to capture share.

Deuk Spine Institute (United States) — clinical novelty and channel access: The Deuk Piriformis Release®, a patented, minimally invasive outpatient surgical approach using a very small incision, represents a potential structural shift for refractory cases. Its safety-first narrative and early case series without reported complications give surgical adopters a compelling value proposition. For incumbent surgical device suppliers and referral-based clinic groups, this underscores the importance of building procedural training, outcomes registries, and surgeon-friendly service models.

Allergan (AbbVie) — established injectables playbook: OnabotulinumtoxinA continues to be a central adjunct therapy for clinicians managing spasm-driven sciatic compression. AbbVie’s established commercial and medical affairs reach means continued influence over adoption patterns; strategic partners should expect rigorous outcome-oriented label-extension programs and payer discussions tied to documented functional benefit.

Device and adjunct providers (King Brand Healthcare Products, Omron Healthcare, Hinge Health entrants) — symptomatic and non-invasive modalities: Specialized wraps, TENS, and wearable neuromodulation devices are positioning as first-line or adjunctive solutions that reduce acute care utilization. The proliferation of lower-cost, patient-managed devices creates an avenue for larger firms to develop bundled home-care programs linked to physical therapy networks.

Pharmaceutical majors and generics (Bayer, Novartis, Sanofi, Teva, Endo) — conservative management bedrock: Broad-spectrum analgesics, NSAIDs, and muscle relaxants remain necessary elements of standard care. Their role is strategic rather than disruptive: protecting formulary access, supporting multimodal protocols, and enabling partnerships with clinic networks for stepped-care algorithms.

April 2026 randomized clinical data comparing corticosteroid injection versus extracorporeal shockwave therapy, alongside ongoing trial listings evaluating manual-release techniques and shockwave protocols, signal a period of comparative-effectiveness clarity. These studies will increasingly inform payer coverage criteria and triage algorithms defining which patients progress from conservative therapy to interventional or surgical pathways. For market participants, the message is clear: invest now in prospective registries, standardized outcome measures (pain scores, functional assessment, return-to-work) and head-to-head economics to shape clinical guidelines rather than react to them.

The report is designed as an operational playbook for 2026 decision-making. It blends rigorous quantitative forecasting with executable strategic modules, including:

Market sizing and trajectory (historical 2020–2025, base year 2025, forecast 2026–2032) with layered scenario analyses to stress-test entry timing and pricing strategies.

Care-pathway maps and payer-impact models that translate clinical inputs into reimbursement levers and expected revenue curves for outpatient versus inpatient adoption settings.

Competitive profiles and capability matrices for the leading clinical innovators, device suppliers, and pharma players — highlighting go-to-market strengths, clinical evidence gaps, and partnership opportunities without disclosing proprietary client data.

Regulatory and coding playbooks tailored to the U.S. landscape and guidance notes for major international markets — including model language for claims, documentation, and value dossiers tied to botulinum toxin and procedural interventions.

Commercialization toolkits: pricing sensitivity, channel strategy for hospitals vs. clinics vs. retail/home modalities, and digital engagement frameworks for patient activation and adherence.

M&A and partnership screening templates to identify tuck-in targets, capability gaps, and regional leaders that accelerate route-to-market.

Prioritize evidence partnerships: fund targeted RCTs or registry partnerships that align with payer endpoints and functional outcomes rather than surrogate endpoints alone.

Design hybrid commercial models: combine device distribution with value-based post-procedural rehab programs to capture downstream revenue and produce measurable cost offsets for payers.

Optimize coding and documentation at launch: align clinical protocols with CMS guidance on injection techniques and LCD criteria for off-label therapeutics to reduce denials and speed reimbursement.

Build surgeon and therapist training programs: for any manufacturer of minimally invasive solutions, practical adoption will hinge on training, proctoring, and local procedure champions who can demonstrate reproducible outcomes.

Monitor comparative-effectiveness publications closely: upcoming trial results will be inflection points for formulary and procedure adoption — integrate real-time literature surveillance into commercial planning cycles.

Device manufacturers: use the report’s operational forecasts and outpatient adoption scenarios to size pilot markets and design modular delivery bundles that include training, OR logistics, and outcomes reporting.

Pharma/generics: prioritize label-agnostic value dossiers demonstrating functional benefit in refractory populations and seek strategic partnerships with clinics to embed products into step-up protocols.

Clinical networks and hospital systems: evaluate the economics of establishing dedicated piriformis pathways that triage early to non-invasive options and escalate to minimally invasive procedures based on standardized failure criteria.

Private equity and strategics: use the report’s M&A templates and regional overlays to identify targets that offer scalable outpatient delivery or proprietary procedural IP with defensible outcomes data.

Piriformis syndrome is transitioning from an under-recognized soft-tissue complaint into a managed therapeutic area with defined care pathways, growing outpatient procedural options, and an evidence base that will rapidly inform payer decisions. For 2026, the competitive advantage will accrue to organizations that integrate evidence generation, payer-aligned economics, and scalable clinical training into their market-entry playbooks. PW Consulting’s report equips executives with the forecast, the playbooks, and the scenario tools needed to convert the market’s modest size and steady growth into durable strategic positions.

For the full dataset, segmented forecasts, proprietary scenario tables, and the complete go-to-market toolkits referenced in this preview, visit our report page to access the comprehensive Worldwide Piriformis Syndrome Market study and download the executive briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Piriformis Syndrome Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com