Construyendo la Experiencia de Juego Perfecta: El Futuro de los Casinos Cripto en España

Sports |

2026-05-02 11:21:45

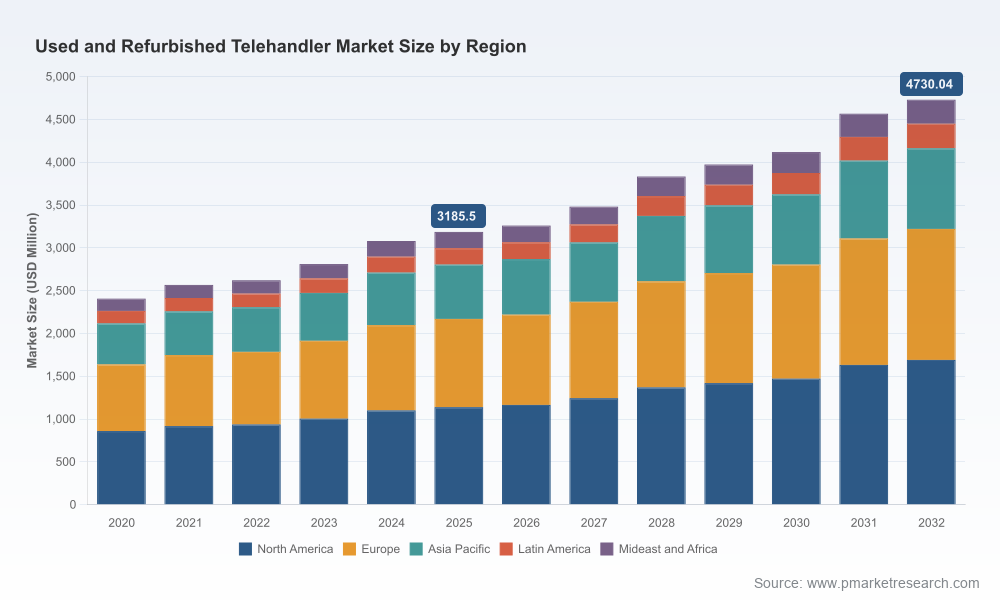

As capital discipline, sustainability mandates and rental economics converge, the used and refurbished telehandler sector has emerged as a decisive leverage point for construction, agriculture and industrial operators. PW Consulting’s new market study frames this segment as a maturing, risk‑adjusted growth opportunity: the global used and refurbished telehandler market expanded from roughly USD 2.4 billion in 2020 to about USD 3.19 billion in 2025 and is projected to reach approximately USD 4.73 billion by 2032, representing a compound annual growth rate (CAGR) of 5.81% across the 2026–2032 forecast horizon. For 2026 corporate planning cycles, the report translates these macro dynamics into executable options for OEMs, rental houses, dealer groups and secondary‑market investors.

Worldwide Used and Refurbished Telehandler Market

Operational resilience: Used and refurbished telehandlers reduce capex burden for owners while preserving operational throughput—critical where new‑unit lead times remain volatile and project schedules are aggressive.

Worldwide Used and Refurbished Telehandler Market

Margin optimization: Certified refurbishment programs can create a differentiated high‑margin revenue stream for OEMs and dealers when coupled with warranty, telematics and funding packages.

Worldwide Used and Refurbished Telehandler Market

Portfolio rationalization: For rental businesses, an optimized lifecycle (acquisition → rental → refurbishment → resale) reduces fleet total cost of ownership (TCO) and improves asset turnover.

Regulatory and ESG alignment: Refurbishment pathways support circularity claims and reduce embodied carbon compared with full new‑build replacement—becoming an increasingly important factor in public and private procurement.

Demand elasticity in capex‑constrained markets — As project owners prioritize cash flow, the rental and used segments capture demand that would otherwise be postponed or converted to lower‑specification equipment.

Raw material and input cost pressures — Steel price trends and tariff shifts materially influence refurbishment economics. Stabilized mid‑2025 hot‑rolled coil prices and expanded U.S. tariff exposure are already altering inbound parts costs and repair margins for 2026 planning.

Safety and compliance upgrades — 2025 OSHA updates elevating operator certification and digital inspection records increase the value of refurbished units that can be delivered with compliant documentation and certified retrofits.

Product and service innovations — Recent trade‑show rollouts demonstrate advances in stability control, smarter operator interfaces and telematics that can be retrofitted into used fleets, enabling product refresh strategies without full unit replacement.

Rental model expansion — Contractors and large scale infrastructure programs increasingly favor flexible, short‑cycle rentals, creating a replenishment pipeline for certified used equipment at predictable intervals.

Market architecture and sizing: A defensible top‑down and bottom‑up valuation of the worldwide used and refurbished telehandler market with scenario pathways to 2032 (base year 2025) and sensitivity to steel pricing, regulatory change and rental penetration.

Value chain diagnostic: Line‑by‑line mapping of vendor, dealer, rental, refurbishment center and end‑user economics, including standard operating margins, spare parts friction points and logistics bottlenecks.

Refurbishment playbook: Step‑by‑step protocols for inspection, priority upgrades (safety, stability and telematics), cost benchmarking and service‑level warranties that maximize resale value while containing repair cycles.

Commercial models: Pricing ladders, lease‑to‑own frameworks, certified pre‑owned certification criteria and digital asset‑tracking templates suitable for immediate deployment by dealers and rental firms.

Due‑diligence toolkit for investors: Standardized checklists for fleet acquisition, expected CAPEX to certification, projected resale curves and tax/ accounting considerations across major jurisdictions.

Scenario planning suite: Four discrete market scenarios (Baseline, Upcycle, Tariff Shock and Rapid Rental Adoption) with strategic implications and contingency playbooks for each player archetype.

Competitive benchmarking and strategic moves: Qualitative and quantitative assessments of leading OEMs, aftermarket specialists and rental consolidators, with recommended partnership and M&A archetypes.

The secondary telehandler market is shaped by legacy OEMs that operate certified used/refurbished programs via dealer and rental channels, plus a growing number of specialist refurbishers and platform intermediaries. Leading OEMs maintain strategic advantages through proprietary parts, dealer networks and brand trust—assets that materially influence end‑user willingness to pay for certified units. Key industry participants examined in this study include:

JCB (Rocester, Staffordshire, UK) — Strong global dealer footprint and brand recognition support certified resale programs focused on construction and agriculture.

Caterpillar Inc. (Irving, Texas, USA) — Cat Used certifies inspected units with warranty bundles; a preferred option where heavy‑duty performance and uptime assurances are critical.

Manitou Group (Ancenis, France) — Deep product range and regional dealer integration provide a foundation for targeted refurbishment offers across construction and industrial applications.

JLG Industries / Oshkosh Corporation (McConnellsburg, Pennsylvania, USA) — Rental fleet rotation and compact model prevalence underpin high‑velocity used channels in North America and beyond.

Merlo, Dieci, Terex (Genie), Bobcat (Doosan), Liebherr, CNH (New Holland), Wacker Neuson, Haulotte and Claas — A mix of niche specialists and broadline OEMs that adopt varying approaches to certified refurbishing, ranging from in‑house programs to dealer‑led reman efforts.

Our analysis highlights distinct strategic postures: brands that invest in certification and telematics integration capture premium resale pricing; dealers with streamlined logistics and refurbishment capacity accelerate unit turnover; rental consolidators benefit from scale arbitrage but must balance utilization with refurbishment throughput.

Input cost volatility — Steel price movements and trade policy (including recent tariff shifts) can compress refurbishment margins or change the economics of parts substitution. Robust procurement hedging and local sourcing strategies are recommended.

Regulatory tightening — Enhanced operator certification and inspection documentation raise the bar for resale readiness; firms that can offer certified compliance packages gain competitive advantage.

Technological obsolescence — New control systems and telematics reduce the relative value of older platforms unless retrofit pathways are viable; investment in modular retrofits is a critical decision point for 2026.

Capital cycles and rental penetration — A faster shift toward rental models can increase short‑term supply of used units while creating long‑term demand for certified, lower‑age refurbished assets.

Market concentration dynamics — While the market retains meaningful participation from a wide set of OEMs and service providers, scale advantages in parts, logistics and brand certification can drive local concentration in key channels.

OEMs: Formalize certified refurbished programs tied to telematics, extended warranties and parts subscriptions. Pilot modular retrofit kits that address safety and telematics modernization.

Dealers: Invest in centralized refurbishment hubs or strategic partnerships to capture aftermarket margin and shorten time‑to‑certification. Standardize inspection and digital certification to streamline resale across regions.

Rental operators: Optimize lifecycle models to balance utilization and resale timing—use data to identify ideal hold periods and refurbishment trigger points to maximize margin per asset.

Private investors and resellers: Use the provided due‑diligence toolkit to evaluate acquisition pipelines, and stress‑test portfolios against tariff and material‑price scenarios.

Policy and procurement teams: Recognize certified refurbished units as compliant, lower‑carbon options in procurement specifications where lifecycle emissions and budget constraints align.

Our Worldwide Used and Refurbished Telehandler Market study is designed as a practical playbook for executives who must convert market trends into executable plans in 2026. By combining a defensible market forecast (2025 baseline and multi‑scenario projections to 2032), a refurbishment operational guidebook, commercial models and a competitive intelligence matrix, the report helps stakeholders prioritize investments, structure partnerships and mitigate regulatory and input‑cost risk.

This briefing intentionally outlines strategy and actionable frameworks while preserving the full granularity of segmentation and pricing analyses for licensed report access. For the detailed breakdowns, regional and application‑level dynamics, and downloadable toolkit templates, please consult the full PW Consulting report on our website.

For detailed analysis of this topic, please visit the official page:Worldwide Used and Refurbished Telehandler Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com