Emerging Markets for Carboxy Therapy 2031

Health |

2026-06-22 14:04:25

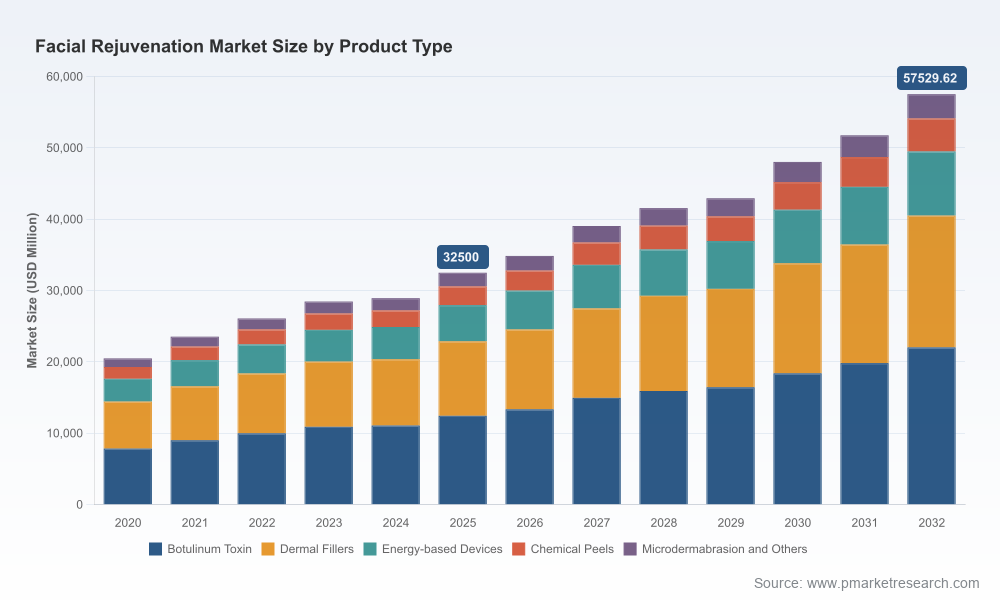

As global demand for non- and minimally invasive aesthetic procedures accelerates, our new PW Consulting report delivers a tightly focused, operational roadmap for executives seeking to position their businesses for sustained growth through 2026 and beyond. The facial rejuvenation market — valued at approximately USD 32.5 billion in 2025 — is on a structurally positive trajectory, sustaining an 8.5% compound annual growth rate across the 2026–2032 forecast window and reaching material scale by the end of the period. This press release highlights the report’s strategic value for corporate decision-making while deliberately withholding granular subsegment tables to incentivize access to the full intelligence package.

Worldwide Facial Rejuvenation Market

Facial rejuvenation sits at the intersection of powerful demographic tailwinds, accelerating technology deployment, and shifting consumer expectations for minimally invasive care. The combination of proven revenue resilience, above-market growth rates, and a moderate-to-high degree of market concentration makes this sector an attractive arena for platforms and specialists alike. Our analysis shows that a relatively compact group of incumbent and scale players account for the majority of commercial value, presenting both barriers and opportunities depending on a company’s go-to-market approach.

Worldwide Facial Rejuvenation Market

At the macro level, the market’s expansion to roughly USD 32.5 billion in 2025 and a projected mid-single-digit to high-single-digit CAGR underscores two practical realities for decision-makers:

Worldwide Facial Rejuvenation Market

These topline indicators should guide portfolio prioritization, capital allocation, and M&A sizing assumptions in 2026 planning cycles.

Regulatory developments over 2025–2026 are non-trivial and require active program-level management. Key dynamics highlighted in the report include heightened safety scrutiny around certain energy-based and combined-modality procedures, with official safety communications that demand upgraded clinical protocols and provider training. Parallel regulatory modernization efforts for cosmetics have raised facility compliance expectations, and several jurisdictions are advancing risk-based licensing for non-surgical cosmetic procedures.

For commercial teams, the practical implications are immediate: go-to-market timelines, labeling, KOL engagement, and training investments must reflect an environment where regulators and payers are more attentive to safety, quality systems, and credentialing. Importantly, most aesthetic procedures remain elective and are not broadly reimbursed, reinforcing the importance of consumer-oriented value propositions and practice-level reimbursement strategies where medically necessary indications exist.

The competitive map is nuanced, comprising large, integrated pharmaceutical-aesthetics players, specialized device innovators, and a long tail of injectables and platform providers. Our report walks through strategic profiles of leading firms, illustrating how different business models compete on clinical evidence, distribution networks, training ecosystems, and brand equity.

Our competitive benchmarking shows that the top three firms capture a majority share of the market, while the top five control a dominant portion — a concentration profile that both raises entry barriers and creates niche arbitrage opportunities for agile innovators.

Designed for senior leaders and investment committees, the report translates market dynamics into executable programs. Core deliverables include:

To preserve the value of actionable intelligence for subscribers, we do not disclose the granular breakdowns of product, regional, or end-user splits here; those detailed tables and proprietary indices are available exclusively in the full report.

Events across 2025–2026 underscore the dual nature of opportunity and risk. Regulatory safety advisories related to certain energy-device uses make provider-credentialing and device-vendor responsibility central to customer retention. At the same time, approvals expanding indications for key injectable products and targeted acquisitions combining novel neuromodulators and resilient fillers point to continued product-led growth.

For executives, these signals translate into concrete actions: accelerate evidence generation for differentiated claims, invest in provider training and accredited centers of excellence, and reassess product mix versus regulatory risk exposure.

Based on scenario modeling and client work across the value chain, PW Consulting recommends the following high-priority moves for 2026:

The facial rejuvenation market presents a compelling growth story in 2026, but opportunity is conditional on disciplined execution across regulatory compliance, clinical evidence, and commercial integration. PW Consulting’s report delivers the strategic scaffolding and operational-level playbooks necessary to convert market momentum into durable enterprise value.

For executives, investors, and innovation leaders who require the complete dataset — including scenario tables, regional and product segment breakouts, company dashboards, and deal screens — please consult the full report via our online portal. The proprietary segment-level intelligence and appendices are intentionally gated to preserve competitive advantage and to provide subscribers with the end-to-end analytics needed to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Facial Rejuvenation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com