Why Digital PTW Systems Are Redefining Safety and Efficiency in High-Risk Industries

Other |

2026-04-15 09:38:02

PW Consulting’s latest Worldwide Subsea Flowlines Market report, anchored on a 2025 base year and projecting through 2032, puts the industry on a steady recovery and modernization path. We benchmark the market at approximately USD 4.80 billion in 2025 and model growth to roughly USD 6.98 billion by 2032, reflecting a 5.5% compound annual growth rate (CAGR) over the forecast window. These headline dynamics disguise a much more nuanced competitive and technology-driven landscape—one where procurement timing, materials strategy, and SURF execution models will determine winners and laggards in 2026.

Worldwide Subsea Flowlines Market

Timing matters: capital allocation and contracting windows for major offshore projects are moving from planning into award phases in 2026. Our forward-looking scenarios quantify near-term tender pipelines and identify where supply-chain congestion and fabrication capacity constraints will impact project economics and schedule risk.

Worldwide Subsea Flowlines Market

Material and thermal strategy is strategic, not tactical: operators face trade-offs between upfront CAPEX, operational flow assurance, and long-term integrity management. The report synthesizes technology roadmaps—electrically heat-traced flowlines (EHTF), pipe-in-pipe (PiP), and clad/CRA solutions—into supplier selection and cost-to-ownership frameworks tailored for 2026 procurement cycles.

Worldwide Subsea Flowlines Market

Integrated SURF and deepwater capability are premium assets: businesses that can offer standardized modular solutions and integrated execution (EPCI + long-lead manufacturing) capture outsized value in high-barrier deepwater and pre-salt pockets. Our supplier scorecards and capability heatmaps enable operators and financiers to differentiate execution risk across bids.

Offshore investment momentum and tie-back economics: renewed E&P investments and a strategic push to develop satellite/tie-back opportunities are lengthening average project life and pushing for longer, higher-spec flowlines to reach remote reservoirs while preserving host-facility constraints.

Thermal management and flow assurance technology adoption: EHTF and advanced PiP solutions are enabling longer tie-backs and reducing operating risk for wax/ hydrate-prone fluids. A notable industry initiative introduced a next-generation subsea flowline heating approach in late 2025 that lowers installation complexity by permitting post-lay cable installation—materially reducing mobilization time and emissions.

Standards and compliance: the EN ISO 13628-1:2025 update refocuses design and operational requirements for subsea production systems and will be a procurement checkpoint for 2026 tenders. Our compliance matrix translates the standard into procurement clauses, test regimes, and surveillance strategies that clients can incorporate immediately.

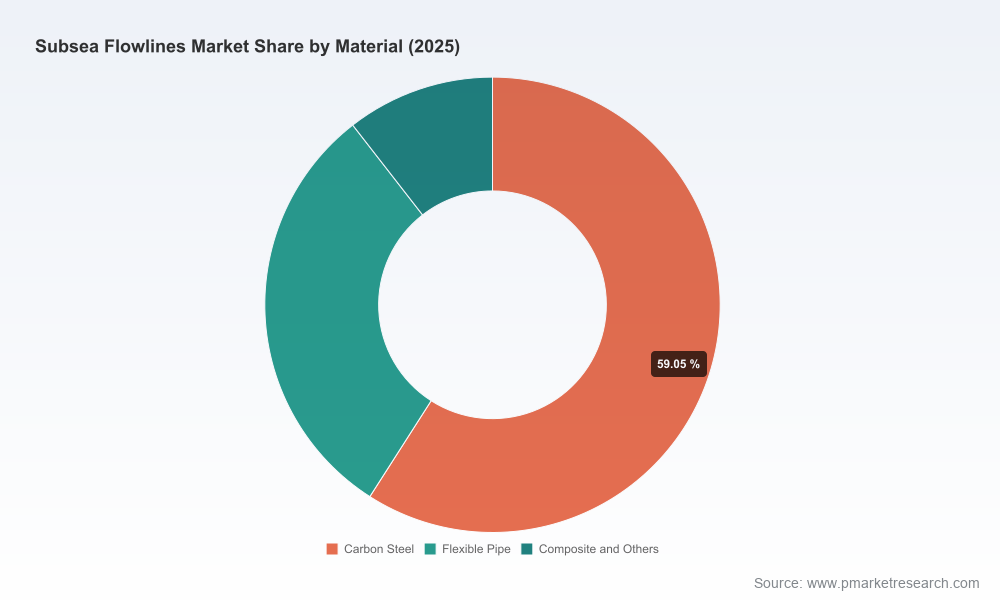

Materials evolution: the industry is moving beyond generic carbon steels toward clad pipes and corrosion-resistant architectures where CO₂, H₂S and chlorides are present. The broader clad pipe market itself was valued at roughly USD 4.2 billion in 2025—an indicator of material premiumization that will affect L1 bids and spare parts strategies.

Market sizing and scenario modelling: end-to-end forecasting (2026–2032) with upside and downside scenarios tied to oil-price trajectories, regional sanctioning timetables, and tie-back economics—designed to inform 2026 CAPEX re-prioritization.

Comprehensive supplier capability assessment: granular profiles, technical strengths, fabrication footprint, mobilization readiness, and financial resilience ratings for all major SURF and flowline vendors, wrapped into decision matrices for single-source vs. multi-vendor strategies.

Procurement toolkit: bid evaluation templates, a tender checklist aligned to EN ISO 13628-1:2025, and standardized commercial language for long-lead items, warranty regimes, and performance bonds—specially tailored for 2026 drilling and SURF schedules.

Technologies and materials playbook: comparative total-cost-of-ownership (TCO) models for carbon steel, clad/CRA, flexible pipe, PiP and EHTF approaches, including sensitivity to distance, temperature loss, and hydrate mitigation strategies.

Risk and mitigation frameworks: installation, integrity management, supply-chain and geopolitical risk matrices with recommended contractual levers—insurance structures, milestone-based payments, and shared contingent working capital approaches for long cycle projects.

Commercial scenarios for financiers: cashflow phasing models and break-even thresholds for tie-back versus standalone FPSO solutions designed to accelerate investment committee approvals in 2026.

The subsea flowlines sector is concentrated among a handful of integrated SURF and specialist suppliers—our CR3 and CR5 analysis indicates that the top three and top five suppliers capture a dominant share of global activity, underscoring the strategic importance of partnerships and alliance models in 2026 tenders.

TechnipFMC — Integrated EPCI capability, strong manufacturing and design muscle for both flexible and rigid systems. Position: favored in large, technically complex deepwater packages where turnkey SURF is prioritized.

Subsea 7 — Market leader in subsea engineering and installation with a track record across tie-backs and pre-salt developments. Recent award activity in Brazil reinforces its playbook for large-scale SURF execution and vessel mobilization strategies.

Saipem — Strong EPCI footprint with an emphasis on rigid pipeline installations and recent major project wins in South American waters. Their integrated project delivery model makes them a competitive counterparty for risk-averse operators.

Aker Solutions — Focuses on standardized, modular flowline systems and alliance-based deliveries that reduce engineering customization and accelerate schedule—an attractive option for repeatable field developments in harsh environments.

Baker Hughes / OneSubsea — Deep strength in flexible pipes and subsea production systems; recent flexible-pipe contracts for Brazilian pre-salt assets demonstrate market momentum in high-spec flexible applications.

Oceaneering, Tenaris, Vallourec, Prysmian, Nexans, Dril-Quip, ITP Interpipe — Each plays a critical role in the SURF ecosystem: connectors and tie-in systems, line pipe production, premium connections, umbilicals and subsea power, subsea trees/wellheads, and specialized PiP insulation technology respectively. Successful bids increasingly rely on consortiums that combine these niche strengths under integrated project governance.

Large SURF awards in Brazil and Guyana/Suriname basins have concentrated near-term demand for flexible pipe, umbilicals, and long production flowlines—putting pressure on fabrication slots and accelerating supply-chain agreements for long-lead items.

Joint industry projects and technology consortia introduced in 2025 are converging on post-lay heating approaches and lower-emission installation methods. Early adopters of these methods will gain bid advantage in 2026 by offering lower installed-cost and carbon-footprint solutions.

Material premiumization (clad/CRA) is compressing supplier pools for high-corrosion applications. Buyers who finalize supply arrangements and qualify secondary suppliers in 2026 will insulate projects against price volatility and delivery slippage.

Operators: prioritize early engagement with qualified SURF consortia, include EN ISO 13628-1:2025 compliance checkpoints in all RFQs, and model TCO for thermal management options before final investment decisions.

EPCIs / Integrators: lock fabrication capacity and long-lead material agreements; invest in modular flowline designs and digital twin capabilities to shorten commissioning cycles and reduce change orders.

Materials & specialist suppliers: fast-track qualification programs and redundancy planning for clad and CRA supply lines; demonstrate integration capability with EHTF and PiP manufacturers to access bundled SURF opportunities.

Financiers and insurers: require robust installation and integrity management covenants, and consider staged funding tied to installation milestones to de-risk exposure in long-flowline projects.

The PW Consulting report is a decision-enabler for 2026. It translates macro forecasts into executable procurement strategies, vendor shortlists, and risk-mitigated contracts. For executives preparing budgets, negotiating supplier terms, or prioritizing technology pilots, the granular tools in the report will compress timelines and improve expected project returns.

PW Consulting has packaged the full dataset, supplier scorecards, and procurement templates behind our report portal to preserve commercial sensitivity while providing clients with immediately actionable insights. For organizations that require bespoke briefings—portfolio prioritization, tender readiness assessment, or a supplier negotiation playbook—our industry practice stands ready to deliver tailored engagement commencing in Q1 2026.

Access to the full report, detailed segmentation tables, and the downloadable procurement toolkit is available via our report page. PW Consulting’s senior analysts are also scheduling a limited number of executive briefings in January–February 2026 to walk clients through scenario outputs and bespoke implications for upcoming bid cycles.

For detailed analysis of this topic, please visit the official page:Worldwide Subsea Flowlines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com