Automotive Sound Insulation NVH Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

As the automotive industry enters a decisive phase of electrification, regulatory tightening, and material innovation, noise, vibration and harshness (NVH) management has moved from a cost center to a strategic enabler of product differentiation, regulatory compliance and total-cost-of-ownership optimization. PW Consulting’s latest Automotive Sound Insulation NVH Market study — built on a 2020–2025 historical baseline and a 2026–2032 forecast horizon — provides a practical, decision-oriented framework for OEMs, tier‑1 suppliers, material makers and private equity sponsors planning for 2026 investment cycles.

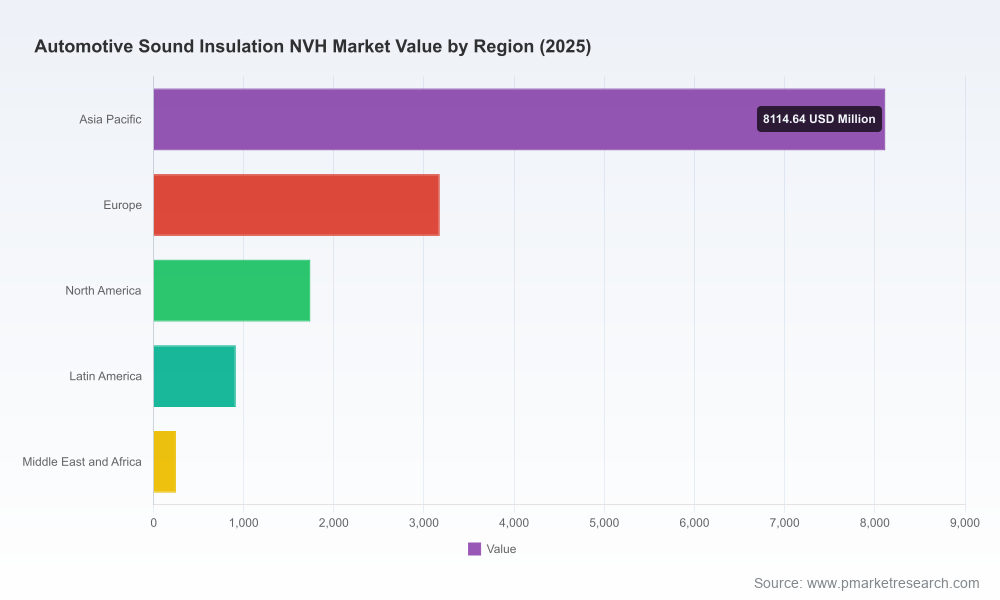

Automotive Sound Insulation NVH Market

Macro view: growth trajectory and market structure

The global market for automotive sound insulation is on a steady upward path. After rising through the early 2020s, the market reached an assessed base in 2025 and is forecast to expand at a compounded annual growth rate (CAGR) of approximately 5.85% through the forecast window. Under PW Consulting’s scenario modelling, the market advances noticeably from the 2025 base into the late-2020s and early-2030s, reflecting a combination of regulatory push, EV-related NVH challenges, and material substitution dynamics.

Automotive Sound Insulation NVH Market

Equally important for strategy: market concentration has meaningful implications for partner selection and M&A. Our proprietary concentration metrics show a mid-market consolidation profile — the top three firms account for a significant but not dominant share, with the top five widening that footprint. This structure creates space for both scale plays and focused specialist challengers.

Automotive Sound Insulation NVH Market

Why this matters for 2026 decisions

- Compliance-driven procurement: With region-level noise standards phased in through 2026 and beyond (including tightened EU noise limits and the mandatory rollout of updated UN regulations from mid‑2026), OEM product teams must reconcile NVH targets with bill-of-materials (BOM) and assembly constraints. The incremental cost of meeting stricter dB(A) limits is increasingly front-loaded in design cycles; delaying material choices will increase program risk.

- EV platform NVH strategy: Electric powertrains shift acoustic profiles — reducing engine masking while elevating tonal sources, road and aerodynamic noise, and new structure-borne pathways. For vehicle acoustics leaders, this requires rebalancing investments across absorption, damping and insulation approaches to preserve perceived quality without inflating weight or cost.

- Supplier and technology roadmaps: Mid-decade sourcing decisions will determine access to lightweight fiber systems, high-performance foams, and engineered elastomers. Given measured industry consolidation, companies with targeted access to scale or unique IP will be advantaged in long-term supply agreements.

- M&A and partnership timing: The market’s consolidation profile invites selective transactions — both tuck-ins for capability and bolt‑on deals to secure mono-material or high-recycled-content manufacturing platforms that simplify end‑of‑life recycling and meet sustainability mandates.

What the PW Consulting report delivers

This report is explicitly designed to inform 2026-capex and sourcing choices by translating market dynamics into executable options rather than simply presenting numbers. Key deliverables include:

- Actionable scenario analyses that map regulatory timelines and EV adoption rates to NVH material demand under multiple macroeconomic assumptions.

- Decision trees for OEMs and tier‑1s that prioritize interventions by program phase (early concept, validation, production ramp), showing where NVH investments deliver the highest value in quality perception, warranty exposure, and compliance.

- Supplier selection matrices built on capability, scalability, sustainability credentials and price-to-performance bands — designed to support RFP development and bilateral negotiation strategies.

- Material substitution playbooks that assess lifecycle trade-offs across fiber‑based solutions, microcellular foams, elastomers and adhesive‑based dampers — with processing, weight and end‑of‑life implications highlighted for program managers.

- A granular innovation tracker profiling recent product launches, material science breakthroughs and manufacturing process advances that are likely to influence procurement specifications during 2026 program windows.

- Risk registers and mitigation protocols oriented to supply chain continuity, raw material volatility, and compliance deadlines to integrate into program governance.

Competitive landscape — who to watch (and why)

The report’s competitive analysis synthesizes company positioning, technology portfolios and go‑to‑market moves to help buyers and investors prioritize counterparties. A few strategic observations:

- Autoneum: As a leader in lightweight fiber‑based NVH components and mono‑material carpet systems, Autoneum is positioning sustainability as a differentiation axis. Recent participation at industry conferences and trade shows has emphasized mono-material integration and high recycled-content solutions — developments that matter for OEMs targeting circularity without sacrificing acoustic performance.

- BASF & Dow: Chemical majors continue to influence the market by enabling advanced microcellular elastomers and tailored polyurethanes. Their material platforms are critical where cavity filling, chassis attachments and engine‑mount analogues demand tunable foam responses and long-term durability.

- 3M: Specialty materials firms remain key when innovation needs to reconcile thin-form insulation with high absorptive performance. Their proprietary textile and adhesive systems lower integration complexity for vehicle interiors while meeting tight packaging constraints.

- Vibracoustic & Sumitomo Riko: System-oriented suppliers focus on mounts, bushings and decoupling systems optimized for EV powertrain NVH. Their recent wins in premium EV segments underscore OEM preference for integrated system solutions over point-product procurement.

- Henkel & ElringKlinger: These players bring capability in adhesive damping, sealing and composite reinforcement — critical for sealing systems and body-in-white acoustic management where structural paths dominate perceived noise.

Notably, recent industry activity reflects an interplay of product innovation and application wins: Autoneum’s showcase of sustainable NVH materials and Vibracoustic’s supply to a premium EV pickup illustrate how material and system innovation are already translating into program-level adoption.

Regulatory dynamics and their operational impact

Two forces are especially relevant for 2026 planning. First, tighter EU noise limits — phased through the mid‑2020s — change compliance envelopes and force earlier NVH intervention in program calendars. Second, the upcoming mandatory phase of UN R51.03 introduces new urban-weighting and high-load test protocols, which have material implications for cavity design and damping strategies. Failure to align product validation plans with these regimes could create rework costs and delayed certifications in 2026 production ramps.

Material-tech trends to prioritize in 2026

- Lightweight fiber systems: Offer broad weight-performance trade-offs and simplify mono-material recycling when designed into carpets and pads. Prioritize partners with demonstrated scale and validated indoor-air quality (IAQ) performance.

- Microcellular and engineered foams: Deliver localized damping and cavity filling with controlled stiffness characteristics; critical for balancing tactile NVH and ride comfort in EV platforms.

- Adhesive and composite dampers: Increase design freedom for complex body geometries and can reduce component count if selected early in the program.

- Integrated mount systems: For powertrain and suspension interfaces, integrated systems reduce NVH paths and can be tuned at module level — an increasingly common choice for EV applications.

How to use this preview when planning 2026 initiatives

Decision-makers should treat NVH not as a late-stage checkbox but as an input to program architecture and supplier strategy. From a practical standpoint, our recommendations for 2026 planning are:

- Lock in NVH targets and candidate material classes by the end of concept freeze. Late material swaps create outsized weight, cost and certification risks.

- Prioritize supplier pilots that can demonstrate both acoustic metrics and manufacturing yield on representative assemblies; require environmental and recyclability evidence to align with sustainability goals.

- Layer regulatory scenario stress-testing into validation plans to capture edge-case loads introduced by UN R51.03 test regimes.

- Consider selective M&A or exclusive supply relationships for mono-material or closed-loop recycling capabilities that reduce end‑of‑life risk while simplifying assembly logistics.

Next steps — where to find the full intelligence

This executive preview highlights the strategic contours that will shape NVH decisions in 2026. PW Consulting’s full Automotive Sound Insulation NVH Market report contains the comprehensive datasets, granular segmentation analyses, supplier scorecards and the scenario models that underpin the recommendations summarized here. To translate the macro trajectory and competitive insights above into program-level actions — including supplier shortlists, price-sensitivity bands and regulated-test compliance maps — access the full report and the accompanying interactive tools on PW Consulting’s market portal.

For program leaders, procurement chiefs, product planners and investors planning allocations or interventions in 2026, the combination of a clear growth trajectory, non-trivial market concentration and near-term regulatory inflection points means there is both urgency and opportunity. PW Consulting’s research equips you to act with clarity — identifying where to invest, whom to partner with, and how to de‑risk certification and ramp activities in the critical mid‑decade window.

Contact

For further inquiries and bespoke briefings tailored to your program timeline, PW Consulting’s Automotive Practice is available to provide targeted workshops and supplier-engagement playbooks that convert market insight into executable procurement and engineering plans.

For detailed analysis of this topic, please visit the official page:Automotive Sound Insulation NVH Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com