Ritual Privado en Barcelona: Experiencia de Bienestar, Relajación y Equilibrio Interior

Other |

2026-06-24 07:26:07

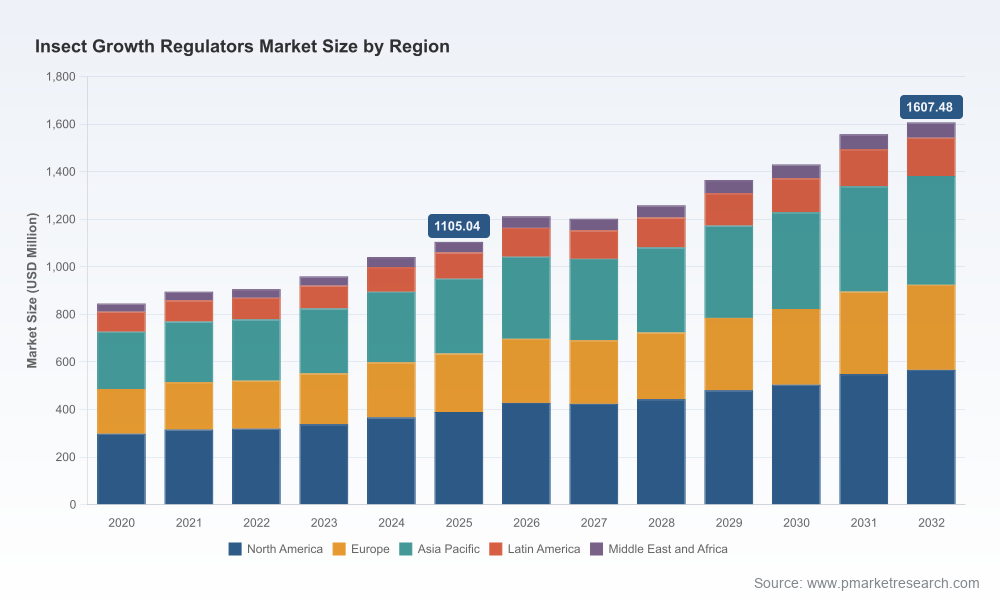

As regulatory pressure, evolving pest resistance profiles, and shifting agricultural practices reshape crop protection priorities, insect growth regulators (IGRs) are emerging as a strategic lever for agribusinesses, pest management firms, and animal-health players alike. PW Consulting’s latest market study, anchored on a 2025 base year and projecting through 2032, maps a clear, investible trajectory for the sector: the IGR market grew from approximately USD 845.5 Million in 2020 to USD 1,105.04 Million in 2025 and is forecast to reach an estimated USD 1,607.48 Million by 2032, expanding at a compound annual growth rate of 5.5% over the 2026–2032 period.

Worldwide Insect Growth Regulators Market

The near-term acceleration reflected in the 2024–2026 corridor signals a market transitioning from niche replacement products to core elements of integrated pest management (IPM). While this release intentionally withholds detailed segment-by-segment revenues to drive readers to the full report, the headline points are clear: steady mid-single-digit CAGR, a meaningful uptick in overall addressable market size since 2020, and a competitive landscape that is neither monopolistic nor highly atomized — the top three firms account for under half the market and the top five approach just over half, indicating significant room for consolidation and differentiated positioning.

Worldwide Insect Growth Regulators Market

Portfolio prioritization: With regulators favoring low-residue, targeted chemistries and growers demanding lower environmental impact, firms must rationalize pipelines to emphasize IGR chemistries that balance regulatory resilience with agronomic efficacy. Our forecast provides scenario-tested demand curves that allow R&D and portfolio teams to size near-term ROI on development programs.

Worldwide Insect Growth Regulators Market

Regulatory planning as strategic defense: IGRs often require product-specific labeling and may face use restrictions in certain cropping systems. Anticipating these constraints is now a strategic imperative for registration teams — missteps can materially erode market access. The PW report synthesizes label-driven limitations and EPA group classifications to guide registration prioritization.

M&A and partnership playbooks: Given a market where the three largest firms capture roughly 42.5% and the five largest roughly 58.3%, mid-sized targets with differentiated formulations or niche channel access are attractive acquisition candidates. Our study models valuation sensitivities against revenue trajectories and regulatory uncertainty, helping strategy teams frame bid ranges and integration plans.

Commercial channel optimization: Pest control professionals, greenhouse horticulture, livestock feed-through programs, and broadacre agriculture each demand distinct go-to-market approaches. The full report maps channel economics and adoption barriers, enabling sales leaders to reallocate resources to highest-yield segments without exposing those granular splits in this preview.

Product innovation and next-gen chemistries — Recent launches demonstrate intensified investment in molecules that deliver systemic activity, longer residuality, or lower residues. Systemic ketoenol-class products and enhanced juvenile-hormone analog formulations are examples of how innovation is targeting both efficacy and regulatory acceptance.

Regulatory nuance — IGRs are frequently regulated under specific EPA classifications and labeling regimes that reflect their mode-of-action and delayed developmental effects on target pests. Compliance with label restrictions (for instance, prohibited use patterns for some granular formulations) and proactive stewardship programs will be non-negotiable for market entrants.

Supply-chain specialization — The active ingredients behind many IGRs rely on specialized chemical intermediates (e.g., phenoxyphenyl derivatives and juvenile hormone analog synthesis pathways). Securing reliable sources, dual-sourcing plans, and transparent traceability will reduce production risk and protect margins.

Urban & specialty demand — Resistance management in urban pests and demand for low-residue solutions in greenhouse and livestock environments are driving commercial innovation beyond broadacre agriculture, creating profitable niches for nimble suppliers.

Proprietary market sizing and scenario forecasts (2026–2032) with policy and price sensitivity overlays to help financial planning and capital allocation.

Go-to-market playbooks across four commercial channels: broadacre agriculture, greenhouse/horticulture, urban professional pest control, and livestock/feed-through systems — including margin models, distribution archetypes, and adoption levers.

Regulatory risk matrix and registration prioritization tool that maps likely approval timelines and label constraints against potential revenue impact.

Supplier and raw-material risk model, with mitigation options such as backward integration, contract manufacturing screening criteria, and inventory strategies tailored by chemical class.

Full competitive intelligence dossiers on 12 market participants, plus M&A scouting lists and synergy valuation templates to expedite deal screening.

Actionable product development scorecards for evaluating new IGRs across efficacy, regulatory durability, cost-to-produce, and channel fit.

The competitive field blends global agrochemical heavyweights with regional specialists and heritage pest-control firms. Key players included in our analysis are BASF SE, Bayer AG, Syngenta AG, Sumitomo Chemical, Corteva Agriscience, FMC Corporation, ADAMA Ltd., Nufarm Limited, Valent U.S.A., Central Life Sciences, MGK, and Russell IPM. Several strategic patterns emerge:

BASF SE (Ludwigshafen): Deep R&D and formulation capabilities focused on chitin synthesis inhibitors and juvenile hormone analogs. Strengths: global registration expertise and integrated distribution in crop protection. Strategic implication: BASF is positioned to leverage formulation science to extend product life-cycles where regulatory pathways allow.

Bayer AG (Leverkusen): Recent introduction of a ketoenol-class systemic product underscores a push into systemic IGR chemistries that address sap-feeding pests. Strengths: advanced R&D and strong grower relationships. Strategic implication: competitors must anticipate Bayer's push where systemic activity confers agronomic advantages.

Syngenta AG (Basel): Expanding urban pest portfolios and reformulated products to counter resistance highlights a dual agricultural/urban strategy. Strengths: product breadth and channel penetration in professional pest control. Strategic implication: urban pest control remains a battleground for differential formulations and resistance-management claims.

Sumitomo Chemical (Tokyo): Portfolio focus on low-residue chitin synthesis inhibitors for rice and horticulture targets high-value specialty segments. Strengths: regional crop expertise and regulatory alignment for low-residue systems. Strategic implication: entrants must match local regulatory and residue expectations to compete effectively in specialty crops.

Corteva Agriscience, FMC, Nufarm: These players compete on scale and distribution, bundling IGRs into broader IPM and seed-treatment offerings. Strengths: channel reach and integrated product suites. Strategic implication: strategic partnerships or bundling strategies are essential for smaller IGR specialists to gain traction.

ADAMA, Valent, Central Life Sciences, MGK, Russell IPM: Regional or niche specialists focusing on greenhouse, feed-through, or professional pest control segments. Recent ADAMA launch of a greenhouse thrips/whitefly IGR in late 2025 exemplifies how niche product introductions create immediate local advantage. Strategic implication: targeted, compliant formulations can yield rapid local uptake without the need for global scale.

ADAMA’s late-2025 horticultural IGR launch in Japan highlights the commercial opportunity in compliant greenhouse solutions under tight residue regimes.

Bayer’s March 2025 Plenexos launch signals intensified investment in systemic ketoenol-class IGRs that appeal to growers managing sap-feeding pests and seeking translocation within the plant.

Syngenta’s early-2025 portfolio enhancements aim to confront urban cockroach resistance with combined IGR formulations — a pattern we expect to continue as urban resistance profiles evolve.

Sumitomo’s 2025 rice-paddy product underscores the premium that low-residue, targeted chitin synthesis inhibitors command in region-specific cereal systems.

Run a rapid portfolio stress test using our regulatory risk matrix: flag products with label-driven use restrictions and quantify near-term addressable markets under conservative labeling scenarios.

Initiate supplier resilience assessments for active-ingredient intermediates and secure second-source agreements for high-risk chemistries.

Prioritize pilot programs for differentiated formulations in greenhouse and urban professional segments where speed-to-market can outpace mass-market shifts.

Use our M&A scouting templates to identify sub-scale innovators with unique formulations or channel access as acquisition or distribution partners.

This briefing is a strategic “trailer”: it demonstrates the analytical depth of our Worldwide Insect Growth Regulators Market report and outlines the decision-useful takeaways for 2026. To preserve the value of our granular, validated intelligence we have intentionally withheld revenue-by-region, detailed product-type and application splits, and specific company-level revenue contributions from this public summary. The full report contains those datasets, downloadable models, and end-user adoption curves that enable precise scenario planning and valuation.

For boards, corporate development teams, product managers, and regulatory leads preparing for 2026, PW Consulting’s full report delivers the operational playbooks and financial models necessary to convert IGR market growth into measurable advantage. Contact PW Consulting to obtain the complete study, customized briefings, and the Excel-based forecast model designed for immediate integration into your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Worldwide Insect Growth Regulators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com