Worldwide Handles of Tilt & Turn Windows Market: Strategic Outlook for 2026 Decision-Making

PW Consulting’s latest market study, Worldwide Handles of Tilt & Turn Windows Market (base year 2025), delivers an actionable strategic compass for executives planning across product development, procurement, and market expansion in 2026. The global market for tilt & turn window handles has demonstrated steady expansion — rising from roughly USD 510 million in 2020 to an estimated USD 648.5 million in 2025 — and our forecast shows continued growth through 2032 (projected to reach approximately USD 927 million), at a compound annual growth rate (CAGR) of 5.23% for the 2026–2032 horizon. These headline metrics frame practical decision windows: identify where to defend margin, where to invest in innovation, and where to pursue partnerships or consolidation.

Worldwide Handles of Tilt & Turn Windows Market

Why this report matters for 2026 strategy

- Data-driven scenario planning: The study couples a short-term 2026 outlook with a 2026–2032 forecast that quantifies upside under multiple regulatory and raw-material scenarios, enabling CFOs and heads of strategy to stress-test capex and working-capital plans.

- Commercial and product roadmaps: OEMs and system integrators receive pragmatic guidance on product mixes (material and feature trade-offs), IP and standards positioning, and incremental design investments that yield the highest probability of commercial payback within a typical 36–48 month product cycle.

- Supply chain resilience playbook: Given recent volatility in metal inputs and logistics, the report prioritizes procurement hedging, dual-sourcing strategies, and near-shore options that materially reduce exposure to single-source shocks.

Market dynamics shaping near-term choices

Three structural forces are creating the principal decision levers for 2026:

Worldwide Handles of Tilt & Turn Windows Market

- Regulatory acceleration toward energy efficiency. Revisions such as the EU’s Energy Performance of Buildings Directive and updated national building regulations (including recent UK standards targeting improved U-values and air tightness) are increasing specification demands for window systems. Tilt & turn platforms — valued for their airtight seals and thermal performance — are therefore being specified more frequently in renovations and new builds, which in turn elevates demand for compatible high-performance handles and multi-point locking interfaces.

- Raw-material cost pressure and component sourcing. Aluminum mill-shapes experienced a significant producer-price rise in 2025, pressuring input costs for metal-based handles. That dynamic is forcing manufacturers to revisit bill-of-materials decisions (material substitution where feasible), renegotiate supplier contracts, and accelerate product designs that optimize material usage without compromising performance or compliance.

- Product evolution toward smart, secure, and aesthetic differentiation. The next product wave is less about the basic rotation mechanism and more about integration: lockable handles, concealed mechanisms, corrosion-resistant finishes for aluminum systems, and smart interfaces that fit into home automation fabrics. Recent product introductions underscore this shift toward connectivity and premium finish options.

Competitive landscape: positioning and implications

The tilt & turn handle market is moderately consolidated, with the top three and top five suppliers holding meaningful—but not dominant—shares. This concentration profile creates room for both incumbents and well-capitalized challengers to capture share through targeted differentiation.

Worldwide Handles of Tilt & Turn Windows Market

- HOPPE (Germany) — A benchmark in variety of design and finish, HOPPE combines broad aesthetic portfolios with security add-ons (e.g., SecuStik). For category managers, HOPPE’s model demonstrates the commercial value of offering tiered aesthetic and security upgrades to capture premium margins in renovation-heavy markets.

- Gretsch-Unitas (G‑U, Germany) — A specialist in lockable, standards-tested handles. Their emphasis on normative compliance and tested performance is a reminder that certification-led differentiation remains a practical route to higher price realization in institutional and commercial tendering.

- MACO (Austria) & Roto Frank (Germany) — Both firms showcase the value of systems thinking: delivering handles as part of multi-point hardware ecosystems, with a clear focus on aluminum and diverse profile compatibility. For manufacturers, partnerships or platform-compatible product launches can unlock OEM channels and long-term service revenues.

- Siegenia — The company is accelerating smart-handle adoption; its second-generation Matter-enabled product underlines the commercialization pathway from connected prototypes to specification-ready components. Product and engineering leaders should evaluate integration roadmaps with smart-home protocols as a near-term product requirement rather than a distant optionality.

- Winkhaus, ASSA ABLOY Fenestration, Trojan, FPL Hardware, Formani — This mix of industrial suppliers and premium design houses illustrates the dual axes of competition: functional/system performance on one axis and architectural design leadership on the other. Buyers should segment sourcing strategies accordingly: technical-volume suppliers for large build programs and design-led partners for premium residential segments.

Recent industry signals to act on in 2026

- Product launches and trade show activity (including the latest smart-handle introduction and international exhibitions) indicate that manufacturers are prioritizing both connectivity and concealed hardware innovations. These are early indicators of specification changes in building products catalogues for 2027–2028 projects.

- Publicization of aluminum input cost surges in 2025 is already filtering through supplier price lists and quotation cycles. Procurement teams should expect further price indexing clauses and a renewed focus on total-cost-of-ownership conversations with customers.

- Regulatory timelines (EPBD and national building standards) create explicit retrofit and new-construction windows of opportunity. Companies that align sales incentives and channel strategies to these calendar windows can materially outperform peers.

What the report delivers — practical, operational content

The study is designed as an operational toolkit rather than a theoretical overview. It includes:

- Validated market-sizing and seven-year forecasts at the total-market level, with scenario variants reflecting regulatory tightening and raw-material shocks.

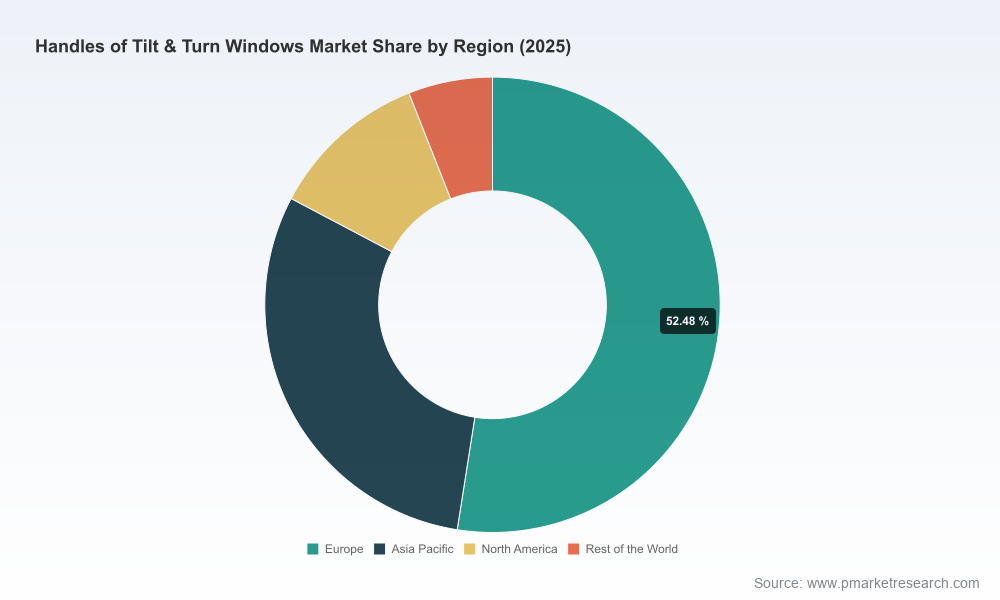

- Segmentation frameworks by region, material type, and end-use that clarify where premiumization and volume opportunities reside (note: granular regional/application splits are available in the full report).

- Supplier benchmarking with profiles, capability maps, and a heat map of strategic strengths (manufacturing scale, system compatibility, standards certification, smart-integration readiness).

- Procurement and supply-chain playbooks: contract design options, hedging strategies for aluminum and zinc inputs, and supplier-risk matrices tuned to 2026 contracting cycles.

- Commercial growth playbooks: channel prioritization, specification-influence tactics for architects and façade engineers, and retrofit-targeting models optimized for regulatory deadlines.

- M&A and partnership screening criteria, including an M&A shortlist methodology and valuation sensitivities tied to rising input costs and potential consolidation scenarios.

Recommended 2026 actions — an executive checklist

- Immediate (0–6 months): Lock short-term metal procurement using a tiered hedging approach; re-run product cost models across worst-, base-, and best-case aluminum-price scenarios; prioritize sales efforts toward renovation pipelines influenced by recent EPBD cycles.

- Near term (6–18 months): Accelerate introduction of lockable and smart-enabled handles (Matter and other stable radio-link standards) for pilot projects; formalize OEM compatibility agreements to enter high-volume aluminum-system programs; refresh warranties and service propositions to capture aftermarket revenues.

- Medium term (18–36 months): Consider strategic M&A or joint ventures that add finish/coat capabilities or near-shore stamping capacity; deploy modular product platforms that reduce SKU proliferation while enabling customization at the point of sale.

- Strategic (3+ years): Invest in IP-backed smart-handle features and integration with building-management ecosystems; build service-led business models (subscription or performance warranties) to monetize installed bases during large-scale renovation waves.

The PW Consulting advantage

Clients use this study not as a static data dump but as a playbook: revenue-impacting procurement decisions, product development priorities, and M&A screening all derive from the study’s blended evidence base of market sizing, standards analysis, supplier profiling, and scenario modeling. Our approach is tailored to executives who must translate market signals into budgeted actions during 2026 planning cycles.

Next steps

This article highlights the strategic signal set and executive implications drawn from the full PW Consulting market study. For procurement managers, product leaders, and corporate development teams seeking the full dataset — including regional and application-level splits, supplier scorecards, and the downloadable scenario models — please refer to the report landing page for the comprehensive datasets and advisory engagement options. The report is intentionally curated to provide both an operational playbook and a diagnostic toolbox to accelerate decision-making in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Handles of Tilt & Turn Windows Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com