Low Power Embedded Controllers Market Projected to Reach USD 7.89 Billion by 2034

Fitness |

2026-06-09 05:50:39

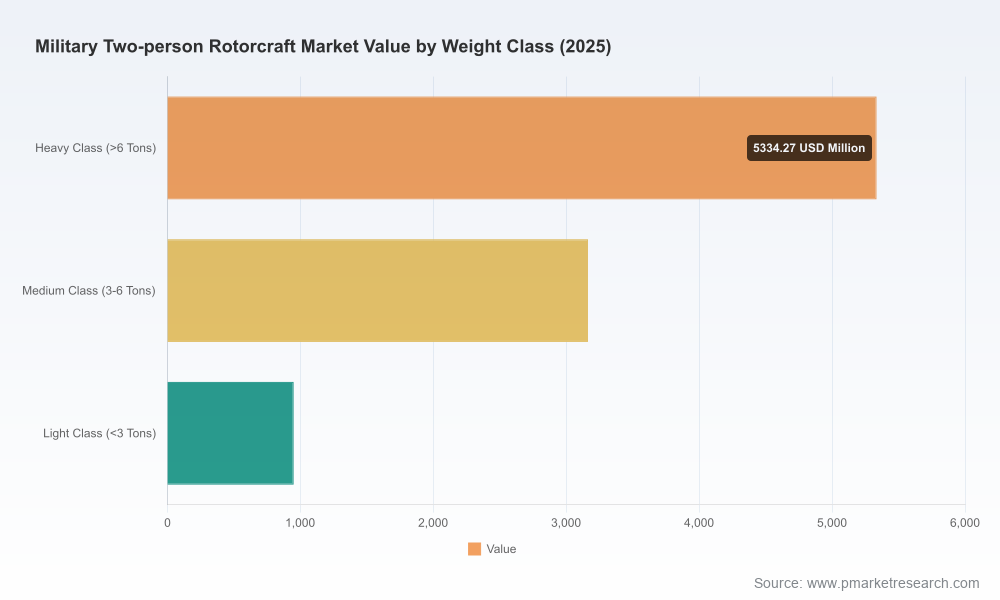

PW Consulting’s new market study on the Worldwide Military Two-person Rotorcraft market equips decision-makers with the strategic foresight needed for 2026 procurement, investment and industrial-base choices. The market has expanded materially in the second half of the last decade, growing from roughly USD 7.7 billion in 2020 to an estimated USD 9.45 billion in 2025. Our baseline forecast shows the market crossing the USD 10.0 billion threshold in 2026, and progressing at a compound annual growth rate of 4.35% through 2032, when modeled demand reaches just over USD 12.7 billion. These topline dynamics set the frame for practical decisions across OEMs, primes, Tier‑1 suppliers and defence customers in the coming 12–24 months.

Worldwide Military Two-person Rotorcraft Market

Three converging forces make 2026 a strategic inflection point for two-person military rotorcraft: (1) accelerating fleet modernization programs among NATO and partner nations, reinforced by early-stage workstreams under Next Generation Rotorcraft programs; (2) post-pandemic industrial recovery that is still constrained by raw-material and composite production bottlenecks; and (3) an increasingly concentrated supplier base. Our market concentration analysis indicates that the top three firms control a substantial majority of value, and the top five extend that dominance further—conditions that amplify the commercial impact of a single large contract or a supply-chain disruption.

Worldwide Military Two-person Rotorcraft Market

Recent program-level activity underscores the shift. OEMs with light- and twin-engine two‑crew solutions have secured follow-on options and national packages, and at least one major OEM has publicly advanced next‑generation concepts in collaboration with defence prime partners. For operators and procurement authorities, 2026 will therefore be a year to decide not only what platforms they acquire, but how they secure long-term sustainment, technology transfer and industrial participation.

Worldwide Military Two-person Rotorcraft Market

Demand drivers are familiar but intensifying: fleet recapitalization, modernization for ISR and light-attack roles, growth in special-operations requirements and an expanded training pipeline. On the supply side, raw-material and composite production constraints are shaping delivery schedules and cost trajectories. Our research highlights the aerospace titanium market as a near-term pressure point for airframe and rotor assemblies, and identifies composite-material constraints as a multi-year bottleneck that will affect throughput unless upstream capacity and skills investments are accelerated.

Regulatory and program-level commitments also matter. Next-generation rotorcraft concept studies and program roadmaps are actively shaping industry investment priorities; several major contractors and OEMs have been selected for concept workstreams that will inform medium‑lift and multi‑mission replacement programs targeting the 2035–2040 timeframe. For 2026, this means a bifurcated market dynamic: continued near-term demand for upgraded legacy platforms and training assets, alongside emergent competition to lead long‑term capability programs.

Our fieldwork and supplier interviews identify three pragmatic mitigation levers for 2026:

Our report is intentionally practical and operational. Beyond the headline market trajectory, PW Consulting provides the executable analytics—tender watchlists, supplier heatmaps, and scenario P&Ls—that procurement teams, business‑development leaders and investors need to convert insight into action during 2026. We also surface the commercial implications of industrial constraints (raw materials, composites, skilled labour) and the competitive consequences of concentration among a handful of dominant OEMs.

In keeping with our “trailer” approach to market disclosure, this press release communicates core market direction, structural risks and strategic imperatives while withholding granular proprietary segmentation tables and contract‑level breakouts. Those detailed datasets—critical for bid pricing, contract negotiations and investment underwriting—are available in the full report and accompanying models.

For defence acquisition authorities, OEM strategy teams, supplier sourcing leads and strategic investors, 2026 will reward preparedness: secure material and supplier pathways now, align bids with sustainment economics, and use modular designs to reduce time‑to‑mission. PW Consulting’s full Worldwide Military Two-person Rotorcraft Market report includes the detailed models and operational playbooks needed to implement these recommendations. To access the comprehensive dataset, scenario tools and vendor scorecards, please consult the official PW Consulting report page or contact our strategic advisory team for a bespoke briefing.

PW Consulting — turning market trajectory into executable strategy for the rotorcraft ecosystem in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Military Two-person Rotorcraft Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com