PW Consulting: Elbow Stiffness Treatment Market Poised for 5.75% CAGR Expansion Through 2032

Other |

2026-07-06 15:10:32

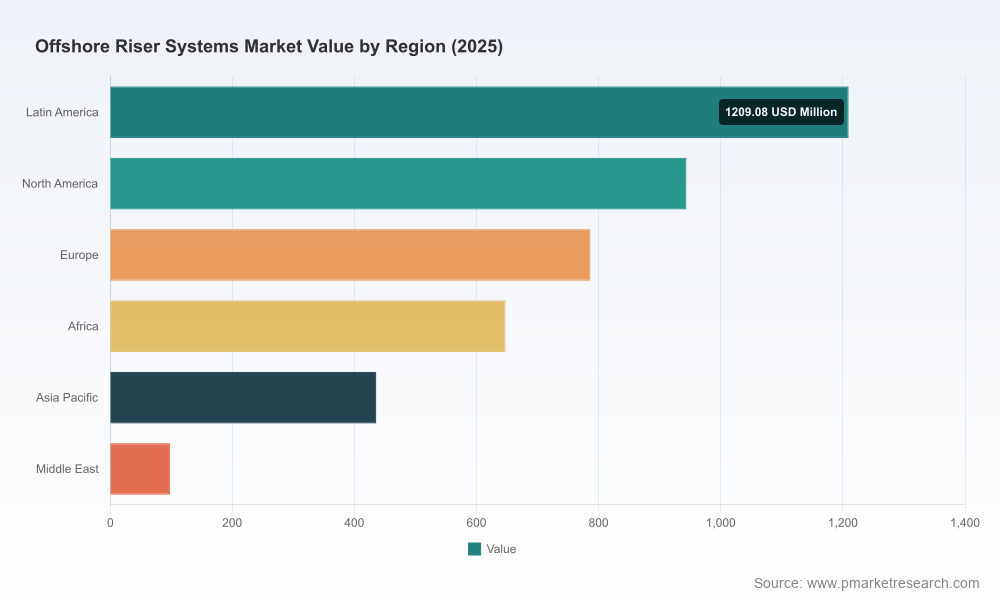

PW Consulting’s new market study on the Worldwide Offshore Riser Systems market (base year 2025, forecast 2026–2032) is crafted as an operational playbook for executive teams making allocation, procurement, and technology decisions in 2026. Our analysis shows the market expanding from roughly USD 3.11 billion in 2020 to USD 4.12 billion in 2025, and continuing to grow to an estimated USD 6.41 billion by 2032, representing a compound annual growth rate of 6.52% across the forecast period. This briefing highlights the strategic implications embedded in those topline dynamics and explains how the full report converts them into actionable steps for operators, EPCIs, OEMs, and investors — while preserving the granular sub‑segment tables and project‑level intelligence exclusively in the paid report.

Worldwide Offshore Riser Systems Market

Offshore riser systems remain a critical bottleneck for deepwater development economics. The market growth trajectory reflects a combination of pipeline replacement, new deepwater and ultra‑deepwater developments, and a growing emphasis on fatigue‑resistant, HP/HT and dynamic riser solutions for floating production systems.

Worldwide Offshore Riser Systems Market

Macro volatility and disciplined upstream capex strategies have reshaped project selection: industry forecasts and recent issuer guidance point to modest upstream capex contraction in 2026, which means only projects with robust economics or strategic importance will proceed — driving a premium on delivery certainty, cost predictability, and modular execution.

Worldwide Offshore Riser Systems Market

Standards and procurement practices are in active flux. The 2025 update to API Standard 2RD and continuing reliance on ISO/API specifications for drilling riser equipment are realigning design and compliance checklists, increasing the emphasis on lifecycle integrity management and documented fatigue analyses as pass/fail criteria in vendor selection.

Raw material and manufacturing cost dynamics: commodity pricing and export flows for carbon steel and tubulars are material to riser economics. Buyers and OEMs are therefore re‑engineering procurement windows, contract indexation, and hedging strategies for the first half of 2026 to insulate project margins from spot volatility.

Project pipeline concentration: a small number of large tenders and field redevelopments announced across 2025–early‑2026 create lumpy demand. Tender timing and installation vessel availability will be decisive constraints; successful bidders will be the ones who can link manufacturing throughput to a flexible installation schedule.

Standards-driven cost of compliance: the latest API and ISO clarifications raise the bar on design verification and integrity management plans. For operators, this increases near‑term development costs but reduces lifecycle uncertainty and insurance friction for complex deepwater systems.

Prioritize contracts that allocate material and schedule risk. For buyers, fixed‑price guarantees without material price adjustment clauses are risky in the current environment. Conversely, suppliers should seek mechanisms (longer lead contracts, gain‑share structures, volume commitments) to secure throughput and smooth factory loading.

Build modularization and pre‑assembly into tender responses. Modular delivery — with factory acceptance testing (FAT) and partial onshore integration — reduces offshore vessel time and is a competitive differentiator in tenders where installation windows are constrained.

Make regulatory and standards‑compliance an early gating criterion in engineering and procurement. Incorporating API 2RD (third edition) and related ISO requirements at FEED and tender stages materially reduces late design changes and claim exposure during hook‑up and commissioning.

Adopt a two‑track supplier engagement model: (1) near‑term qualified vendors for immediate tenders and (2) strategic partners for multi‑year delivery and technology co‑development. This balances speed to market with capability building for fatigue‑resistant and HP/HT riser systems.

Reassess capex phasing and sanction thresholds. With headline upstream capex set to be constrained, operators should sharpen break‑even and IRR thresholds for riser‑intensive developments and consider staged delivery options that align with cash‑flow and commodity price sensitivity.

The riser systems supply chain shows moderate concentration: the top three firms account for roughly 42% of market revenue and the top five for approximately 58%, indicating an oligopolistic dynamic where technical capabilities, fabrication scale, and EPCI track records determine access to large deepwater awards.

TechnipFMC — Integrated SURF and flexible riser capabilities make it a natural front‑runner on large FLNG and deepwater EPCI packages. Recent awards for complex deepwater flexible systems underscore its manufacturing and installation scale.

Subsea 7 — With strong EPCI credentials in URF and SC‑R systems, Subsea 7 competes on engineering and offshore execution for redevelopment and greenfield projects in harsh environments.

OneSubsea (SLB/Aker Solutions/Subsea 7 JV) — Combines deep subsea production systems engineering with riser technology expertise, especially in fatigue‑sensitive and HP/HT applications; attractive to operators facing complex reservoir and environmental conditions.

Baker Hughes and Aker Solutions — Both have differentiated portfolios around fatigue‑resistant risers, buoyancy solutions, and manufacturing integration, competing on reliability and lifecycle service offerings.

OEMs and specialist suppliers (NOV, Oil States, Vallourec, Aquaterra, Balmoral, Weatherford, Saipem) — These players supply critical components (drilling risers, connectors, buoyancy modules, premium tubulars) and niche engineering services. For many projects, their product performance or delivery lead time can determine award outcomes.

Recent market events — large EPCI contracts awarded for deepwater flexible flowlines and risers, multi‑hundred‑km export pipeline installations with S‑type risers, and the issuance of exceptionally large tenders for rigid and flexible risers and umbilicals — are reshaping supplier order books and strategic priorities into 2027–2028. All are discussed in dedicated company‑level case studies in the full report.

Granular market sizing and forward forecast models (global and by type, water‑depth cohort, and region) with sensitivity scenarios reflecting commodity prices and capex paths.

Project‑level pipeline intelligence: timing, award probability scoring, and installation window risk for >300 identified developments and redevelopment projects globally.

Vendor benchmarking and procurement playbooks: technical scorecards, time‑to‑deliver heatmaps, historical bid‑win performance, and contractual clauses optimized for current market risks.

Supply chain and manufacturing diagnostics: lead‑time maps, yard capacity assessments, and sourcing strategies for tubulars, composites and buoyancy modules.

Technology and cost‑of‑ownership assessments: fatigue‑management approaches, HP/HT material choices, connector ecosystems, and life‑cycle OPEX modelling.

Risk matrices and scenario playbooks that translate macro drivers (steel price, standards update, vessel availability, and demand lumpiness) into actionable decision triggers for 90‑day to 24‑month horizons.

90‑day priorities: perform immediate tender stress‑tests, renegotiate material indexation in open contracts, qualify a second‑tier fabrication partner, and embed API 2RD compliance checkpoints into FEED deliverables.

6–12 month priorities: secure long‑lead items, commit to modular manufacturing lines where feasible, execute joint development agreements for specialty riser technologies, and refine sanction thresholds for riser‑heavy developments using our scenario models.

Monitoring and triggers: track a small set of leading indicators we provide — offshore installation yard availability, benchmark tubular export pricing, major tender award calendars, and regulatory guidance changes — to shift strategy from defensive to growth‑capture when windows open.

Our approach couples a quantitative forecast (topline market growth and CAGR) with bottom‑up project and supply‑chain granularity. We do not simply report historical trends; we map where delivery risk concentrates and provide pragmatic, contract‑level mitigations that procurement and project teams can implement immediately. To respect commercial confidentiality and support clients’ competitive positioning, detailed sub‑segment allocations, region/application breakouts, and project‑level intelligence are available only in the full report and the associated client‑briefing packages.

To obtain the complete Worldwide Offshore Riser Systems Market report, the vendor benchmarking appendix, and our executable 90‑day playbook for 2026, contact PW Consulting’s market intelligence team or visit our report page for purchasing and bespoke briefing options.

For detailed analysis of this topic, please visit the official page:Worldwide Offshore Riser Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com