Enhancing Surfaces with Professional Garage and Patio Walkway Coating Solutions

Home |

2026-04-06 20:24:04

PW Consulting’s latest market research, “Worldwide Complicated Urinary Tract Infections (cUTI) Treatment Market — 2026 Outlook & 2032 Forecast,” delivers an operationally focused, decision-grade intelligence package designed to inform executive strategy and tactical plans in 2026. Built on a 2020–2025 historical foundation and a 2026–2032 forecast horizon, the study quantifies market momentum and crystallizes implications for product teams, commercial leaders, supply-chain managers, and corporate development groups.

Worldwide Complicated Urinary Tract Infections Treatment Market

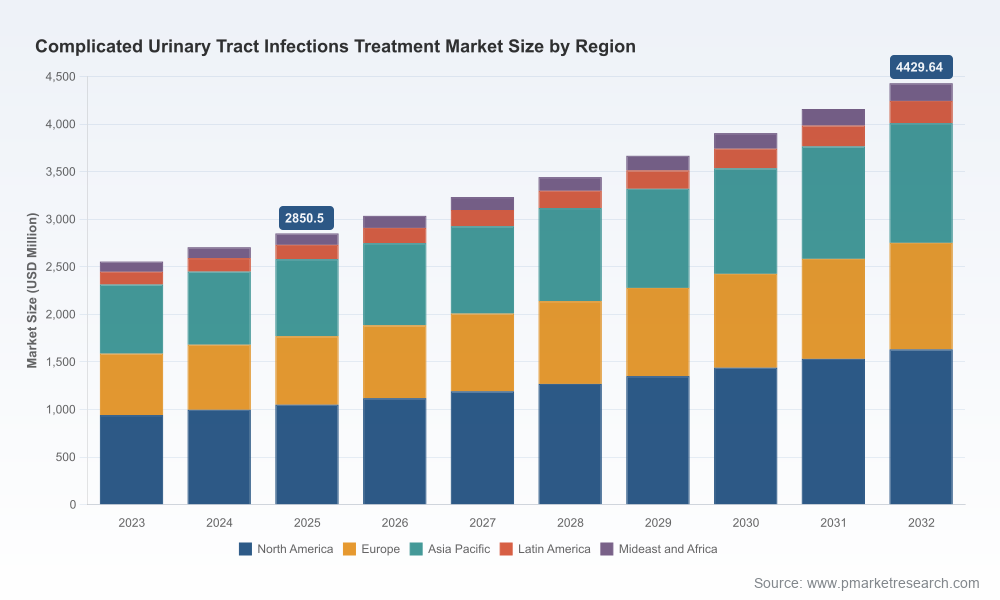

The cUTI market has demonstrated steady expansion from 2023 through 2025, with our base-year modeling pegged at 2025 and a forecast showing sustained growth through 2032. Using conservative baseline assumptions, the market is projected to grow at a compound annual growth rate (CAGR) of 6.5% across the 2026–2032 forecast window. This trajectory reflects a combination of clinical innovation, shifting inpatient/outpatient treatment patterns, regulatory incentives for priority antibacterial therapies, and persistent access and supply challenges that sustain demand for newer agents and combination products.

Worldwide Complicated Urinary Tract Infections Treatment Market

Portfolio prioritization: With market expansion underpinned by targeted regulatory designations and late-stage oral and intravenous entrants, 2026 is a pivotal year to align R&D spend and launch sequencing to maximize time-to-market and reimbursement windows.

Worldwide Complicated Urinary Tract Infections Treatment Market

Access & reimbursement: Payers are actively recalibrating coverage frameworks for high-cost branded cUTI agents. Companies must present robust real-world evidence and value dossiers early to secure favorable formulary positions at launch.

Supply resilience: Raw material constraints observed in 2024–2025 have direct commercial impact. Decisions made in 2026 around supplier diversification, API inventory strategy, and contract manufacturing partner selection will determine launch reliability and margin preservation.

Our report synthesizes epidemiology, treatment pathway analysis, and commercial channel dynamics to identify three primary growth levers:

Clinical innovation: New mechanisms, combination therapies, and the emergence of oral carbapenem-class candidates are reshaping outpatient treatment potential. Regulatory incentives such as QIDP designations accelerate the pathway for differentiated antibacterials and materially affect time-to-revenue calculus.

Shifts in care setting: Hospitals continue to be the primary site for severe cUTI management, but advances enabling safe oral step-down therapy are expanding outpatient treatment mix — affecting unit economics, channel strategy, and patient support program design.

Access friction points: Payer scrutiny, evolving formularies, and potential generic erosion around key molecules necessitate early, data-rich health economic arguments and dynamic pricing playbooks.

The market concentration profile indicates a moderately fragmented yet consolidating space — our analysis places the top-three firms’ combined share in the mid-thirties percent range while the top-five approach the high-forties mark. This structure creates room for both scale advantages and tactical disruption by nimble biotechs and differentiated product strategies.

Large pharma incumbents: Established players with broad infectious-disease portfolios continue to leverage branded assets, hospital relationships, and formulary influence. Their strategic playbooks emphasize lifecycle management, label expansions, and integrated stewardship programs to defend share.

Specialist biotechs and new entrants: Clinical-stage oral carbapenems and novel beta-lactamase inhibitor combinations are examples of assets that can alter prescribing patterns if they achieve regulatory approval and demonstrate equivalence or superiority on key endpoints.

Recent regulatory and clinical milestones: Several manufacturers have advanced important programs or achieved approvals in the last 24 months — events that have real, immediate commercial implications for 2026 planning, including competition for preferred hospital contracts and antimicrobial stewardship protocols.

Global diversified pharmas retain advantages in distribution, payer contracting, and cross-portfolio synergies; their strategic choices in 2026 will focus on defending hospital formularies and expanding outpatient penetration where feasible.

Biotechs with late-stage oral programs have a narrow window to secure commercial partnerships, manufacturing slots, and access pathways. QIDP-type incentives make these assets attractive targets for licensing or M&A, but execution risk remains in scaling production and payer acceptance.

Manufacturers of agents with off-label cUTI use must decide whether to pursue formal label expansion investments or instead optimize lifecycle and real-world evidence strategies to preserve share against formally approved competitors.

For leadership teams preparing 2026 budgets and strategic plans, our report distills actionable guidance across five priority domains:

Go-to-market sequencing: Prioritize regulatory and reimbursement alignment six to nine months ahead of expected approvals. Build launch playbooks that integrate hospital stewardship teams, key opinion leader (KOL) engagement, and payer pharmacoeconomic dossiers.

Supply-chain fortification: Invest in API redundancy and near-shore manufacturing options for critical inputs. Scenario-test your P&L against prolonged shortages and price volatility to understand trade-offs between margin and availability.

Partnership & M&A posture: Use the forecast runway to identify acquisition candidates that provide either differentiated clinical profiles or manufacturing/capacity capabilities. Transaction timing should consider expected patent expiries in the next decade and how that shapes long-term value.

Evidence generation: Accelerate post-marketing studies that demonstrate reduced length-of-stay, successful oral step-down, and lower total cost of care to strengthen reimbursement positioning and uptake in 2026.

Risk & compliance: Anticipate heightened regulatory scrutiny on antimicrobial use and stewardship programs. Align commercial incentives with stewardship outcomes to avoid payor or public health backlash.

PW Consulting’s deliverable is structured as an operational toolset rather than a passive report. Key components include:

Market-sizing model (2020–2032) with scenario toggles for alternative uptake and pricing assumptions, enabling C-suite teams to test “what-if” strategies across conservative, base, and aggressive cases.

Clinical pipeline and product maps by mechanism and development phase, including regulatory milestones and expected launch timelines.

Commercial playbooks tailored to hospitals, retail and online pharmacy channels, and integrated health systems — with recommended salesforce models, contracting levers, and sample value dossiers.

Supply-chain and procurement assessment, including API exposure matrices and supplier concentration risk scoring, to inform manufacturing and inventory decisions.

M&A and licensing target shortlists mapped to strategic objectives (capacity, pipeline, geographic footprint), accompanied by valuation heuristics and integration risk checklists.

Regulatory and reimbursement trackers, incorporating known designations, patent expiry windows, and recent payer actions to help time pricing and access strategies.

Board level: Use our scenario model to stress-test portfolio decisions and capital allocation through 2032 under varying uptake and generic-entry assumptions.

Commercial teams: Build launch timelines anchored to our regulatory and reimbursement trackers; prepare payer dossiers and hospital stewardship engagement plans 9–12 months before anticipated market entry.

Supply-chain & manufacturing: Prioritize supplier diversification and multi-sourcing agreements now; implement the API exposure mitigation recommendations to prevent launch delays and margin erosion.

Corporate development: Align scouting activity with our M&A target matrix; prioritize assets that either accelerate oral outpatient transition or materially enlarge manufacturing capacity for critical antibiotics.

The cUTI treatment market presents a blend of predictable growth and episodic disruption. A steady CAGR over the 2026–2032 period underscores a favorable market environment, but gains will accrue only to organizations that synchronize clinical differentiation with payer-credible value narratives and resilient supply chains. Regulatory incentives and recent approvals have shifted the competitive balance — creating windows for both incumbents and challengers — but practical execution risks around manufacturing and access remain salient.

PW Consulting’s report offers the analytics, tactical modules, and scenario tools needed to convert these market dynamics into executable strategies in 2026. For executives seeking the full segmentation tables, product-level revenue forecasts, and granular regional and channel breakdowns that underpin our recommendations, the detailed datasets and downloadable model are available on our report page.

For detailed analysis of this topic, please visit the official page:Worldwide Complicated Urinary Tract Infections Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com