Worldwide Email Address Verification Service Market — Strategic Outlook for 2026 Decision-Makers

PW Consulting’s latest market research — the Worldwide Email Address Verification Service Market Report (base year 2025) — synthesizes five years of historical trends (2020–2025) and delivers an actionable seven-year forecast (2026–2032). For executives planning technology investments, vendor selection, or M&A activity in 2026, the report translates raw market momentum into pragmatic choices. This executive briefing highlights the strategic value of the study, summarizes the competitive and regulatory dynamics shaping the market, and outlines the exact operational guidance the full report supplies (reserved for subscribers).

Worldwide Email Address Verification Service Market

Why this market matters in 2026

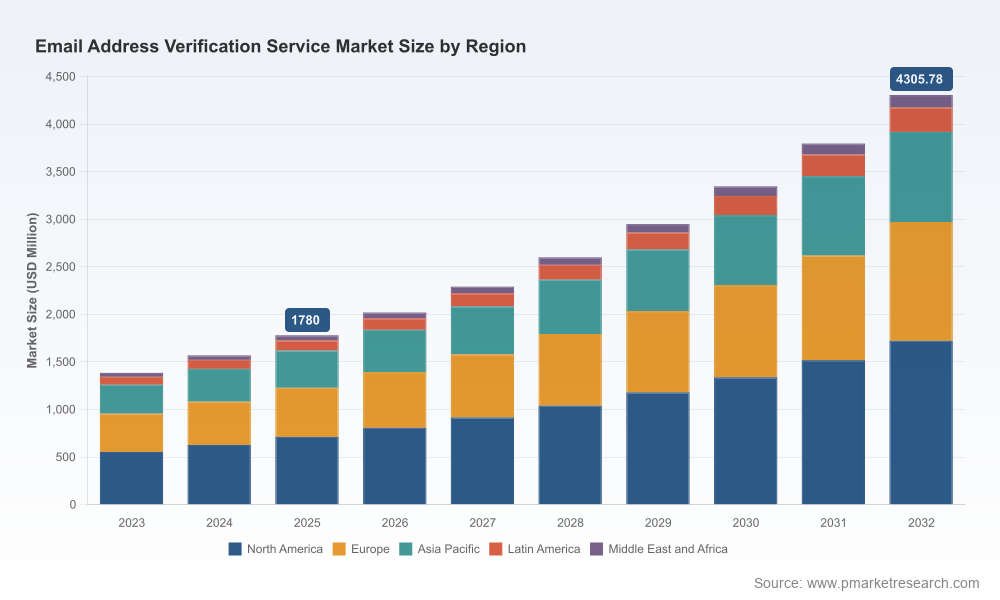

Email remains a primary B2B and B2C channel for customer engagement, identity verification, and account recovery. The economics of list hygiene and address validation are therefore no longer a marginal operational cost — they are integral to revenue efficiency and risk mitigation. PW Consulting’s base-year assessment (2025) places the market at approximately USD 1.78 billion (revenue unit: Million). Our forecast projects continued expansion, with the market expected to surpass USD 2.0 billion in 2026 and rise to roughly USD 4.3 billion by 2032, driven by a compound annual growth rate (CAGR) of 13.45% across the forecast period.

Worldwide Email Address Verification Service Market

Two strategic implications follow:

Worldwide Email Address Verification Service Market

- Short-term (12–18 months): procurement roadmaps should prioritize API-enabled real-time validation and scalable bulk-cleaning capabilities while embedding compliance controls.

- Medium-term (3–5 years): buyers must evaluate vendors for AI-enhanced scoring, privacy-preserving architectures, and platform integration readiness as verification becomes a systemic component of marketing, sales, and identity systems.

Market structure and concentration — what the numbers say

The market shows moderate concentration: the top three providers account for a meaningful but not dominant share, and the top five widen that footprint without reaching monopoly dynamics (CR3 ~34.2%, CR5 ~46.85%). Practically, this means:

- There is sufficient vendor diversity for buyers to negotiate on features and pricing.

- Market leadership is contingent on technology differentiation, regulatory posture, and channel partnerships rather than pure scale alone.

PW Consulting’s sector analysis emphasizes that market share today is a function of accuracy claims, deliverability outcomes, integration ecosystems, and compliance assurances — not just raw pricing.

Competitive landscape — capabilities to watch

Our vendor coverage profiles the commercial leaders and challenger players whose technology stacks and go-to-market strategies are influencing procurement choices in 2026. Representative examples include:

- ZeroBounce (Boca Raton, Florida) — notable for its real-time validation API, deliverability analytics, and scoring capabilities that support marketing and sales teams in inbox placement optimization. (https://www.zerobounce.net/)

- Bouncer (EU-based, Poland) — differentiated by compliance-oriented positioning, including ISO 27001 certification, and strong bulk-verification features favored by security-conscious buyers. (https://www.usebouncer.com/)

- Hunter.io (Belgium) — combines email discovery with verification for B2B lead generation, increasingly used by outbound teams requiring integrated finder + verifier workflows. (https://hunter.io/)

- NeverBounce (by ZoomInfo, Vancouver) — integrates data hygiene with CRM ecosystems and is pitched for scalable agency and enterprise use-cases. (https://www.neverbounce.com/)

- Kickbox, Emailable, Clearout, Verifalia, MillionVerifier, EmailListVerify — each occupying specific positions across affordability, integration breadth, AI feature-sets, and developer-friendliness. (See company sites for details.)

Recent vendor developments validate the trajectory we identify in the report:

- Clearout’s rollout of advanced AI-driven risk detection and predictive deliverability scoring sharpens the competitive emphasis on machine learning to reduce false positives and identify latent risk vectors (March 2026).

- Hunter.io’s independent benchmark release highlights buyer demand for third-party accuracy validation and underscores the value of transparent comparative testing (late 2025/2026 releases).

- Bouncer’s emphasis on ISO 27001 and catch-all detection demonstrates how security certifications and specialist features are becoming table stakes for enterprise procurement (2026 analyses).

Regulatory and compliance headwinds — build for resilience

Regulation is a material driver of vendor evaluation and total cost of ownership. Key developments that 2026 procurement teams must incorporate:

- GDPR enforcement remains active, with significant fines for inadequate security measures. Enforcement trends and high-profile penalties underscore the need for documented lawful bases for processing and robust technical safeguards.

- California’s privacy regime (CCPA/CPPA) has introduced higher statutory damages, expanded audit and cybersecurity obligations, and tighter rules for automated decision-making — increasing obligations for processors and verification vendors working with Californian data subjects.

- For small and medium businesses, first-year privacy compliance costs (policy drafting, data mapping, basic tooling) are non-trivial. Buyers should budget not only for vendor fees but for integration, audit, and data governance expenditures.

Our practical guidance: require vendors to provide data processing addenda (DPAs), security attestations (ISO, SOC reports where available), and a clear provenance model for checking and storing verification results. Failure to bake these requirements into contracts creates downstream legal and reputational risk.

What the PW Consulting report contains — operational tools and playbooks

The full report is structured to move directly from insight to execution. Highlights include:

- Methodology and data appendix — transparent sources, sampling approaches, and verification of vendor-claimed accuracy metrics.

- Vendor scorecards — multi-dimensional assessments across accuracy, latency, integration, compliance, pricing models, and product roadmap indicators.

- Buyer’s decision framework — a phased, risk-weighted template to prioritize features (real-time API vs. bulk processing, security certifications, predictive scoring, CRM/ESP connectors) based on organizational needs and maturity.

- Procurement artifacts — RFP templates, conditional SOW language, and contract negotiation playbooks focused on SLAs, uptime, data retention, and breach notification clauses.

- Implementation blueprints — integration architectures for real-time validation in authentication flows, marketing platforms, and data lakes; pilot design for A/B testing vendor impact on deliverability metrics; and metrics for monitoring (bounce rates, spam complaint reductions, conversion uplift attributable to improved list quality).

- Compliance checklists and TCO modeling tools — to quantify first- and recurring-year costs of ownership including compliance overhead and integration effort.

- Scenario analyses — vendor consolidation, technology substitution risks (e.g., rise of identity graph replacements), and M&A implications for platform buyers and sellers.

To honor the “trailer” principle and preserve the strategic advantage contained in the report, we deliberately withhold detailed segment-level tables and region/application percentage splits from this briefing. The full report contains granular segmentation, use-case matrices, and downloadable financial models available on our website.

Actionable recommendations for 2026 procurement and strategy teams

From our analysis, the following prioritized actions will materially improve outcomes for organizations deploying email verification in 2026:

- Adopt a compliance-first procurement checklist: insist on DPAs, security attestations, and a clear data deletion policy before engaging in pilots.

- Run parallel pilot trials: measure deliverability and conversion impact across at least two vendors (one accuracy-focused leader and one low-cost/high-volume challenger) to quantify trade-offs.

- Demand transparency: require vendors to publish validation method overviews and sample accuracy benchmarks under NDAs if necessary; third-party benchmark reports should be weighted heavily.

- Design for layered validation: combine real-time API checks in user-facing flows with periodic bulk cleaning of legacy lists to optimize cost and friction.

- Embed verification outcomes into core KPIs: integrate verification signals into CRM scoring, campaign segmentation, and fraud-detection pipelines to capture full value beyond bounce reduction.

- Plan for vendor portability: require exportable validation reports and non-expiring credit models where appropriate, to avoid lock-in and to support post-contract audits.

M&A, partnership and investment signals

Given the market’s growth trajectory and fragmented share distribution, strategic acquirers and investors should watch for:

- Target profiles that combine high-quality data assets, strong API ecosystems, and enterprise-grade compliance posture.

- Opportunities to bolt-on AI scoring capabilities or ESP/CRM integrations to accelerate cross-sell into existing martech and data stacks.

- Partnerships with identity graph providers and fraud platforms, which are increasingly common as verification moves from hygiene to identity assurance.

Concluding perspective

For 2026, email address verification is no longer a back-office hygiene task — it is a strategic capability with measurable impacts on delivery economics, customer experience, and regulatory risk. PW Consulting’s report equips leaders with the evidence, procurement templates, and implementation roadmaps needed to convert market growth into defensible advantage. Our modeling shows a robust expansion from the 2025 base, with significant upside for organizations that systematically integrate verification into data governance and customer-engagement systems.

To access the complete dataset, vendor scorecards, downloadable TCO models, and the full segmentation breakdown that underpin these findings, please consult the PW Consulting report page. The public brief above is intentionally high-level; the full publication contains the granular insights your procurement, legal, and technical teams will require to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Email Address Verification Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com