Worldwide Medications for Cutaneous Mastocytosis Market — Strategic Brief for 2026 Decision-Makers

Executive snapshot

PW Consulting’s latest market intelligence release examines the global market for medications used to manage cutaneous mastocytosis, integrating primary research, regulatory reviews, and commercial modelling to produce a forward-looking roadmap for 2026–2032. Built on a base year of 2025 and a historical window from 2020–2025, our market model shows the total market expanding from a documented USD 89.24 Million in 2020 to USD 120.0 Million in 2025, and projecting to reach USD 170.57 Million by 2032 at a compound annual growth rate (CAGR) of 5.15% over the forecast period. These headline numbers frame a market that is small and specialised, yet commercially meaningful for targeted portfolios and strategic M&A in rare dermatologic and systemic mast cell disorders.

Worldwide Medications for Cutaneous Mastocytosis Market

Why this market matters in 2026

- Regulatory inflection points: The recent approvals of targeted systemic agents with demonstrable impact on cutaneous manifestations have re-shaped clinical practice and payer conversations. This creates new reference points for value dossiers and reimbursement discussions focused on symptom relief and disease-modifying benefit.

- Commercial consolidation and opportunity: Concentration metrics indicate an industry where a small number of specialised product franchises and generics dominate clinical practice—presenting both barriers and potential for disruptive entrants via novel mechanisms or differentiated access strategies.

- Operational fragility: Supply chain and raw-material constraints for niche active pharmaceutical ingredients (APIs) are a real operational risk that can materially affect launch timing, formulary positioning, and pricing strategies.

What the PW Consulting report delivers (practical contents)

The report is designed as an operational playbook for executives making portfolio, investment, and commercial decisions in 2026. Key deliverables include:

Worldwide Medications for Cutaneous Mastocytosis Market

- Quantitative market model: historical segmentation and bottom-up forecasting (2026–2032) calibrated to clinical uptake scenarios, pricing trajectories, and reimbursement environments.

- Scenario analysis: upside/downside cases reflecting alternative regulator/payer outcomes, new-label approvals, and generics pressure — with sensitivity testing on price erosion and adoption curves.

- Competitive and pipeline intelligence: profiles of incumbent and emerging players, crosswalks of mechanism of action to clinical outcomes, and prioritized targets for in-licensing or co-development.

- Go-to-market and access playbooks: payer evidence generation strategies, HTA positioning maps, pricing levers, and contracting templates tailored for specialist- and hospital-driven channels.

- Supply chain and manufacturing risk matrix: identification of single-source API dependencies, recommended dual-sourcing strategies, and costed remediation options for short- and medium-term resilience.

- Stakeholder dynamics and KOL signals: synthesis of guideline shifts, society positions, and specialist behaviors that will determine uptake curves across dermatology, allergy/immunology, and hematology settings.

- Actionable M&A and partnership framework: target sizing rules, valuation heuristics for asset-level deals, and integration playbooks that preserve clinical momentum while accelerating commercialization.

Competitive landscape: what incumbents are doing and why it matters

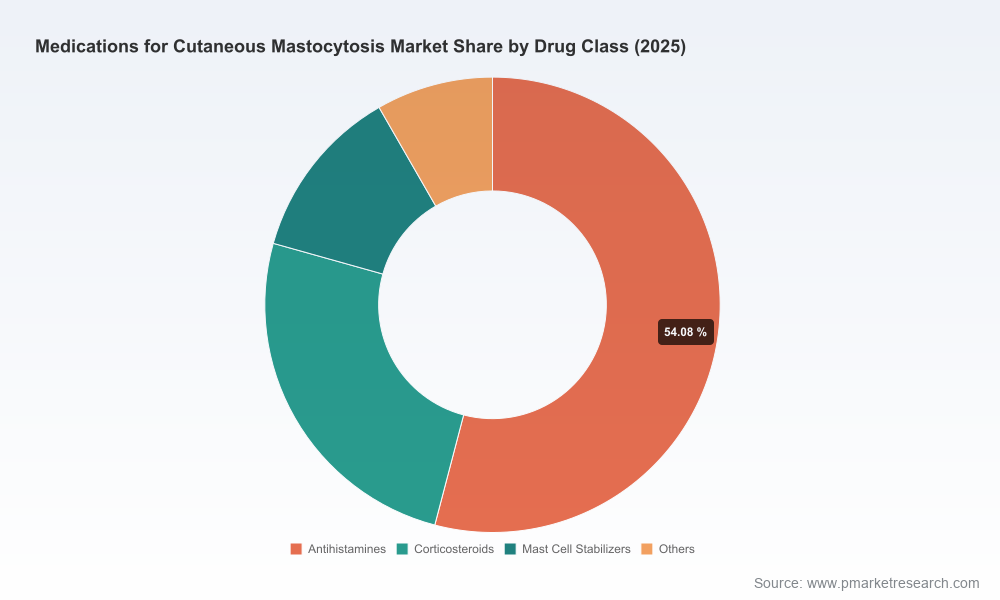

The market has a mix of specialised targeted therapies and a broad set of symptomatic medicines (including antihistamines, mast cell stabilizers and corticosteroids), served by both innovators and generics manufacturers. Our competitive scan focuses on several strategic players whose actions will set benchmarks for 2026 strategy.

Worldwide Medications for Cutaneous Mastocytosis Market

- Blueprint Medicines Corporation (now operating within Sanofi) — Cambridge, MA, USA (https://www.blueprintmedicines.com): The company’s avapritinib (AYVAKIT) development program, now positioned under Sanofi, exemplifies how targeted inhibition of KIT D816V can change the treatment paradigm. Corporate communications in January 2025 emphasised continued investment in mast cell disorders and translational work to address cutaneous involvement. For partners and competitors, this signals both a clinical benchmark and a potential strategic acquirer that is intent on building a mast cell disorder franchise.

- Novartis AG — Basel, Switzerland (https://www.novartis.com): Novartis’ midostaurin (Rydapt) remains a reference multikinase option for advanced disease and continues to underpin symptomatic management pathways. Novartis’ portfolio and payer relationships will be central to determining how new entrants price and differentiate treatments where systemic and cutaneous indications intersect.

- Viatris Inc. — Canonsburg, PA, USA (https://www.viatris.com): As a supplier of generic cromolyn formulations, Viatris represents the structural pricing pressure in the symptomatic segment. Generic players like Viatris are critical to payers’ cost-containment strategies and will be active participants in contracting and formulary negotiations.

- Teva Pharmaceutical Industries Ltd. — Tel Aviv, Israel (https://www.tevapharm.com): With a portfolio focused on generic antihistamines and symptomatic medicines, Teva’s scale in distribution channels and tender markets creates a baseline competitive tier for any entrant seeking volume-driven access in major markets.

Recent regulatory and guideline developments shaping near-term strategy

- Regulatory milestones: The FDA approval of avapritinib for indolent systemic mastocytosis (ISM) and advanced systemic mastocytosis represents the first targeted systemic approval with measurable benefit on cutaneous symptoms. This approval (and corresponding EMA actions) creates precedent for labeling claims, payer value arguments, and trial endpoint selection for next-generation agents.

- Clinical guidance: Recent guideline publications for non-advanced mastocytosis (notably a French guidance release in October 2025) consolidate symptom-directed care in adult practice and provide a clearer framework for clinicians on when to escalate to systemic therapies versus symptomatic regimens.

- Clinical discourse: Ongoing discussions across dermatology and hematology forums (with notable presentations through early 2026) are aligning around practical algorithms that integrate systemic KIT inhibitors for patients with significant cutaneous burden, blurring specialty boundaries and expanding the addressable prescriber base.

- Reimbursement realities: Established reimbursement pathways for symptomatic medicines coexist with heightened scrutiny for novel targeted agents. Payers will demand real-world evidence linking symptom improvement to reduced utilization of acute care and improved patient-reported outcomes.

Market dynamics and operational constraints to factor into 2026 decisions

- Moderate market concentration: The top-three and top-five players collectively account for a meaningful share of market sales, creating both a protective moat for incumbents and a concentrated set of counterparty options for licensing or co-promotion.

- Supply chain fragility: Sourcing specialised APIs is a recurring theme; companies should prioritise procurement audits and contingency sourcing to avoid launch slippages or commercial shortages.

- Channel heterogeneity: Dermatology, allergy/immunology, and hematology/oncology channels display distinct prescribing drivers. Commercial models must be hybrid—balancing specialist field teams with hospital formulary access and digital outreach for rare-disease communities.

How to use this intelligence in 2026 — pragmatic recommendations

- Portfolio prioritisation: Use our forecast scenarios to stress-test which assets merit late-stage investment versus out-licensing. Prioritise assets that can demonstrate measurable cutaneous benefit or clear symptomatic relief in trial designs aligned with payer KPIs.

- Value creation through evidence: Invest in targeted real-world evidence (RWE) programs that quantify reduction in acute care events and improvements in patient-reported symptoms. Payer negotiations in 2026 will favour dossiers with pragmatic endpoints and economic modelling anchored to real-world utilization.

- Access-first launch sequencing: For novel agents, coordinate regulatory submissions with parallel reimbursement dossiers in key markets and pursue managed-entry agreements where appropriate — particularly in jurisdictions that have precedent for rare-disease conditional coverage.

- Supply-chain de-risking: Execute dual-source strategies for critical APIs, and include contractual safeguards for capacity allocation during scale-up phases.

- M&A and partnering: Employ the report’s valuation heuristics to identify targets that offer either novel mechanisms addressing cutaneous pathology or established symptomatic franchises that can be leveraged via distribution scale.

What we intentionally hold back (and why)

In keeping with our “trailer” approach, this public brief communicates strategic conclusions, headline market sizing and directionality, and the competitive and regulatory context you need to assess opportunity. The report itself contains the granular segmentation, country-level forecasts, payer-reimbursement matrices, and product-level revenue splits that underpin the model. Those core data sets are deliberately reserved for subscribers and prospective partners because they represent the tactical intelligence necessary for immediate commercial execution.

Next steps

Executives preparing 2026 strategies should request a walkthrough of the full PW Consulting report to access the detailed market model, playbooks, and raw-data appendices. Our advisory teams are available to run custom scenario modelling, transaction support, and commercial readiness assessments that translate the insights in this brief into executable plans aligned to your risk tolerance and investment horizon.

For confidential inquiries and to arrange a bespoke briefing, contact PW Consulting’s Life Sciences Strategy Practice.

For detailed analysis of this topic, please visit the official page:Worldwide Medications for Cutaneous Mastocytosis Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com