Ambulance Equipment Market Opportunities, Forecast, Size, Competitive Analysis till 2031

Health |

2026-04-13 10:00:28

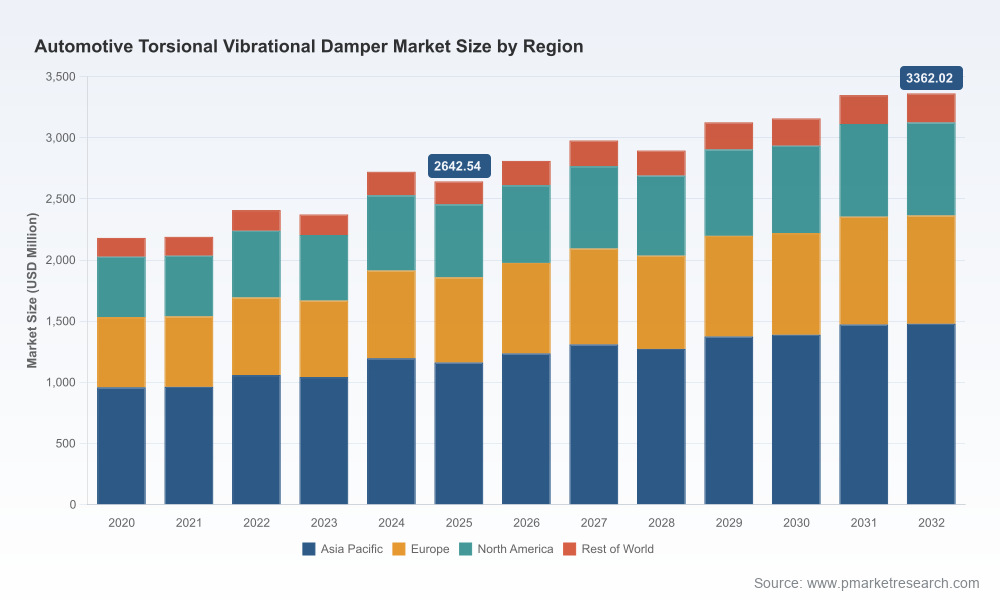

PW Consulting’s new market study on the Worldwide Automotive Torsional Vibrational Damper (TVD) market delivers a decision-grade synthesis for executives planning product, supply-chain, and M&A moves in 2026. Anchored on a 2025 base year and an expanded 2026–2032 forecast horizon, the research maps a market that has shown resilience through recent cyclical fluctuations and structural electrification shifts. Our modelling indicates mid-single-digit compound growth (approx. 3.5% CAGR over the forecast window), underscoring a stable but technology‑intensive landscape where engineering differentiation and systems integration will drive value capture.

Worldwide Automotive Torsional Vibrational Damper Market

Engineering and product roadmaps: As OEMs push smaller, turbocharged engines, mild‑hybrid electrification, and higher accessory/48V loads, torsional excitation profiles are changing. Decision-makers need near-term product strategies to manage NVH and drivetrain durability while avoiding commoditization.

Worldwide Automotive Torsional Vibrational Damper Market

Supply-chain resilience: Material substitution (notably lightweight composites) and sensorized hybrid damper architectures are altering sourcing needs and manufacturing footprints. Procurement strategies must balance specialty polymer supply, viscous fluid specifications, and emerging composite supply partners.

Worldwide Automotive Torsional Vibrational Damper Market

Commercial and aftermarket mix: As vehicle electrification patterns evolve, OEM integration requirements and aftermarket replacement dynamics diverge. Strategic choices made in 2026 about modularity, serviceability, and platform-level integration will determine long-term aftermarket share.

Our topline model shows the TVD market recovering from recent volatility and following a steady growth trajectory through 2032. The market size in the 2025 base year reflects the net effect of powertrain downsizing and early electrification, while the forecast incorporates rising penetration of 48V systems, broader adoption of composite materials, and an incremental shift to hybrid and viscous damper solutions for high-load applications. PW Consulting’s forecast is intentionally conservative on emergence timing for fully sensorized dampers but assumes material and hybridization trends materially reshape product architectures by late‑decade.

Market sizing and scenario modelling: Base case plus two alternative scenarios that stress higher electrification and faster material adoption. Each scenario includes driver-level sensitivity analysis so you can test revenue outcomes for specific strategic moves.

Practical go-to-market playbooks: OEM engagement strategies by vehicle architecture, aftermarket commercialization templates, and channel segmentation matrices that translate engineering attributes into procurement and sales actions.

Technology and product roadmaps: Comparative performance stacks for rubber, viscous, and hybrid dampers; guidance on composite material introduction, thermal management for viscous units, and packaging trade-offs for 48V BSG integration.

Supply-chain diagnostics: Tier mapping, critical raw-material exposure, cost curve benchmarking, and an actionable supplier-selection scorecard for verticalization versus outsourcing decisions.

Competitive benchmarking and M&A screening toolkit: A repeatable framework to evaluate target fit, synergy potential, and integration risk — complete with an M&A valuation dashboard calibrated to TVD-specific margins and capex profiles.

Regulatory and risk matrix: Assessment of emissions, fleet CO2 mandates, and safety/regulatory factors influencing TVD design priorities, plus mitigation playbooks for regional regulatory divergence.

Implementation assets: Executive one-pagers, a 36-month product launch calendar template, and downloadable financial models aligned to the report’s scenarios (interactive spreadsheets included).

The TVD market is populated by engineering-led incumbents and specialist suppliers. Our competitive synthesis focuses on technology differentiation, route-to-OEM access, and modular systems capability — the three axes most predictive of share shifts through 2028.

Vibracoustic SE (Germany) — Strengths: Broad portfolio across pressed, vulcanized, and fluid dampers; deep OEM relationships and systems approach that pairs dampers with decoupled pulleys. Strategic implication: Vibracoustic’s systems capabilities make it a natural partner for OEMs seeking turnkey belt-drive isolation for downsized, start‑stop engines. Competitors should evaluate whether to compete on system integration or specialize on higher‑temperature viscous solutions.

Vibratech TVD (United States) — Strengths: Pioneering viscous designs, focus on durability under high-temperature/high-load conditions, and breadth across crank, cam, and electric drive viscous units. Strategic implication: Viscous dampers offer a clear performance advantage in high-stress and electrified powertrains; expect continued demand in premium and heavy-duty segments. Partnerships or licensing of viscous technologies may accelerate time-to-market for challengers.

ZF Friedrichshafen AG (Germany) — Strengths: Dual mass flywheel and DynaDamp technologies tailored for commercial and hybrid applications, with high torque handling. Strategic implication: ZF’s wheelhouse is commercial vehicles and high-torque niches; acquisition-minded OEMs and tier‑1s looking to enter heavy-duty dampers should price in mechanical robustness and system integration capabilities when benchmarking targets.

Continental AG (Germany) — Strengths: Integrated TVD modules for 48V mild-hybrid engines and broad aftermarket reach. Recent launches indicate a push toward combining damper, pulley, and crank functions into compact modules. Strategic implication: Continental’s integrated modules lower installation complexity for OEMs and become compelling where packaging space and 48V adoption are drivers. Competitors must address modularity and weight trade-offs.

Schaeffler AG (LuK/INA) (Germany) — Strengths: Deep competencies in crankshaft dampers, spoke dampers, and pulley decouplers serving both combustion and hybrid applications. Strategic implication: Schaeffler’s varied portfolio and cross-technology expertise position it well for multi-powertrain platforms. Companies focused on single technologies should anticipate combative OEM spec processes.

Hasse & Wrede GmbH (Germany) — Strengths: Specialist viscous dampers across passenger and commercial portfolios. Strategic implication: Niche specialists retain margins via performance differentiation; they are attractive consolidation targets for tier‑1s seeking viscous capability.

Gates Corporation (United States) — Strengths: System solutions for passenger and light commercial vehicles, with a focus on belt and pulley assemblies. Strategic implication: Gates’ channel and aftermarket expertise make it a formidable player in replacement markets; OEM-focused competitors should assess aftermarket cannibalization risk when designing serviceable modules.

Vibratech’s late‑2024 technical documentation highlights dual viscous damper designs optimized for heat dissipation and durability — a strong signal that viscous technology is being positioned for premium and high‑load segments.

Continental’s mid‑2024 launch of an integrated torsional damper module for 48V mild‑hybrid systems underscores the market imperative for compact, multifunctional modules aligned with electrification packaging constraints.

Composite adoption: Around half of new product developments now integrate lightweight composite materials to improve NVH and reduce mass. That changes cost structures, manufacturing investments, and supplier selection criteria.

Sensorization and hybrid dampers: Over 30% of companies are rolling out hybrid dampers paired with sensors for torque management and predictive maintenance. Early adopters gain service-data monetization and differentiation; late movers risk competing on price alone.

Electrification pressures: The proliferation of 48V mild‑hybrid systems (projected to be a material share of new sales by the late‑2020s) shifts packaging and thermal requirements, favoring modular, integrated damper/pulley solutions.

Define a product portfolio thesis now: Decide whether to compete as a systems integrator, viscous specialist, or lightweight-material pioneer. Each path requires distinct investments and go-to-market motions.

Invest in thermal and materials engineering capabilities: For viscous and hybrid dampers, thermal management and composite manufacturing are primary enablers of performance and cost control.

Pursue selective partnerships for sensor and data capabilities: Sensorized dampers unlock predictive maintenance revenue and OEM differentiation; partnerships lower development risk and accelerate time-to-market.

Calibrate M&A to capability gaps, not revenue size alone: Targets that add viscous technology, composite know-how, or OEM module integration are higher-return than bolt-on volume plays.

Embed scenario planning into procurement: Run supplier strategies against the report’s scenarios (base, high electrification, rapid material substitution) to stress-test contracts and inventory policies.

This study is designed as an execution companion, not a static snapshot. Alongside market forecasts and competitive assessments, you receive modular tools — financial models, scorecards, launch calendars, and supplier evaluation templates — that can be taken directly into negotiation rooms and product-planning workshops. The research balances proprietary field interviews with quantitative modelling to provide probability-weighted outcomes that feed strategic prioritization for 2026.

For teams preparing 2026 budgets and three‑year product roadmaps, the report provides prioritized action items and a clear investment thesis for each strategic path described above. PW Consulting’s clients also gain access to our interactive forecast dashboard and a bespoke briefing workshop where we stress-test your plans against the report’s scenarios.

To access the full dataset, granular segmentation tables, and downloadable implementation assets, please consult the full report on PW Consulting’s distribution page — the complete intelligence and Excel models are available there for practitioners who need the underlying numbers to operationalize the strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Torsional Vibrational Damper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com